VN

VN

EN

EN

26/07/2026, 02:38

Business economics

Credit conditions in 2026 will remain broadly stable

Vietnam’s credit outlook in 2026 could remain stable, as strong domestic demand and liquidity offset rate and tariff risks, according to the VISRating.

Credit conditions in 2026 will remain broadly stable, underpinned by continued policy support and resilient domestic demand.

Credit conditions in 2026 will remain broadly stable, underpinned by continued policy support and resilient domestic demand. While higher interest rates are lifting borrowing costs, corporates are increasing leverage to fund capital expenditure, but these pressures are tempered by a steady operating environment and limited refinancing risk. As a result, in VISRating’s view, credit profiles across most corporate and financial institutions should remain stable, with default rates broadly unchanged from 2025.

Vietnam enters 2026 with strong macroeconomic momentum, following GDP growth above 8% in 2025 and a clear policy ambition to sustain double-digit expansion. Domestic activity is being propelled by an aggressive infrastructure build-out, with state‑budget public investment set to rise by up to 53% in 2026 from VND 732 trillion in 2025.

A robust pipeline of expressways, urban rail, power, and port projects—led by state-owned enterprises and supported by growing private sector participation—should lift employment and cash flows across construction, building materials, logistics, and transportation, with positive spillovers to real estate.

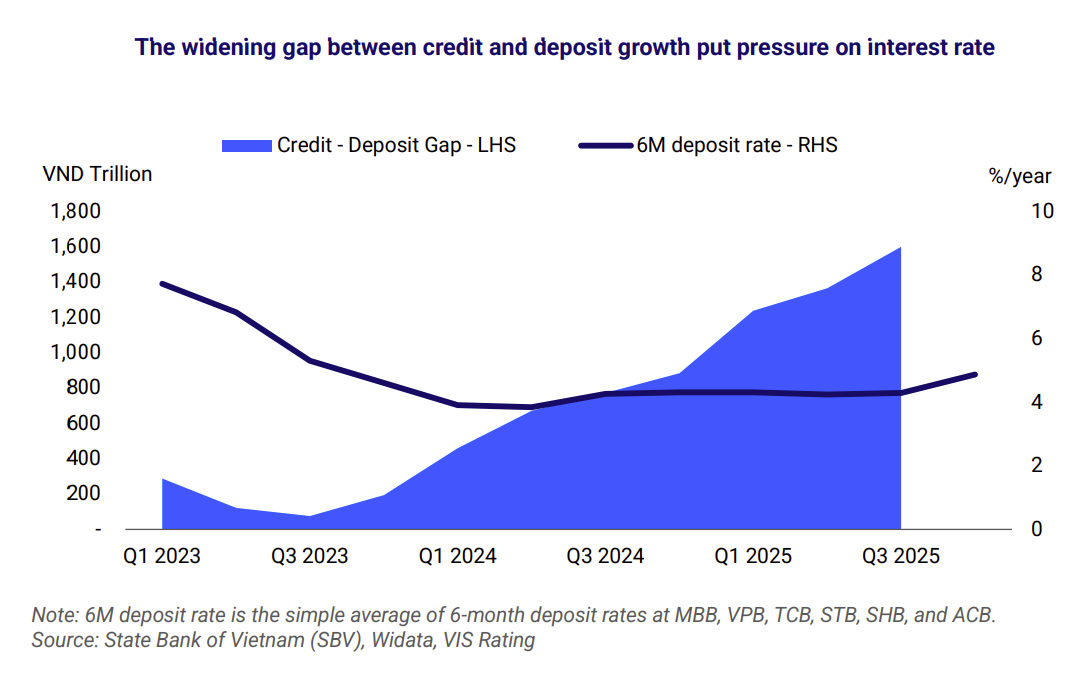

Consumption is expected to recover moderately, with retail sales growth accelerating to around 10% in 2026 from an 8% average in 2022–25, supported by a rebound in international tourism and prospective stimulus measures such as tax relief and expanded social support. Risks are rising, however. “Credit growth continues to outpace deposit mobilization, keeping interest rates elevated and increasing corporate funding costs”, said VISRating.

Externally, higher U.S. tariff levels and intensifying regional competition are likely to weigh on export-oriented sectors, slowing export growth from 2025 levels amid weaker demand in key markets. Changes to the geopolitical landscape and increasingly unpredictable climate events, resulting in severe losses for businesses and households, are also key risks to our stable view. The corporate credit outlook will remain broadly stable, as strong profitability growth is largely offset by rising leverage and interest expenses.

VISRating forecasts average EBITDA growth of 22% for rated issuers in 2026, broadly in line with a projected 21% increase in total debt. Construction and building materials will benefit most from the infrastructure and real estate acceleration, with revenue growth of 15–20% and the strongest credit profile improvement from relatively weak starting points. In the residential real estate sector, leverage is expected to stabilize, and refinancing risks remain manageable, supported by EBITDA growth of 20–25%, improved access to the corporate bond market, and stronger operating cash flows from sales.

According to VISRating, a rebound in tourism and government support measures should lift profitability in retail and consumer goods. In contrast, export-oriented sectors face higher earnings volatility from tariff risks and intensifying competition from Chinese producers, particularly in non-U.S. markets.

Within the financial sector, asset quality and profitability are expected to diverge. Slower system credit growth—targeted at 15% in 2026 from 19% in 2025—along with tighter lending to high-risk real estate, should ease liquidity pressures and curb near-term overheating risks, contributing to a 10 bp decline in the banking sector’s problem loan ratio to around 2.1%. Large banks and securities firms are expected to remain resilient, supported by a stable domestic environment and ongoing policy support.

In contrast, risks remain elevated for smaller banks with exposure to speculative retail mortgages and for cash-loan-focused consumer finance companies, where higher interest rates, rising household leverage, and tariff-related income pressures strain borrowers' debt-servicing capacity. Their profitability will remain constrained by elevated credit and funding costs following deposit rate hikes in 4Q2025. As credit growth and leverage continue to build, banks will become increasingly vulnerable to renewed asset-quality deterioration beyond 2026.

“Credit stress in the bond market is expected to remain contained. Annual default rates are forecast to stay around 1.3% in 2026, unchanged from 2025 and well below the 2023 peak of 12.2%, supported by a resilient operating environment and limited refinancing needs. Bond maturities remain manageable at VND 209 trillion, or 14% of outstanding corporate bonds, following widespread maturity extensions in 2025”, emphasized VISRating.

Cumulative recovery rates on defaulted bonds are expected to improve further, led by stronger performance and effective restructuring among residential real estate issuers. As bank lending becomes more selective, corporate bonds will play a larger role in corporate funding. Improving investor confidence and market liquidity should support a 15–20% increase in new bond issuance in 2026, with private placements to institutional investors continuing to dominate. Banks and real estate issuers will remain central to the market, but issuance is expected to broaden to utilities, logistics, and infrastructure developers as the government’s aggressive infrastructure drive fuels demand for long-term capital

Author: NGOC ANH

RECOMMENDED TOPICS