VN

VN

EN

EN

26/07/2026, 11:20

Investment

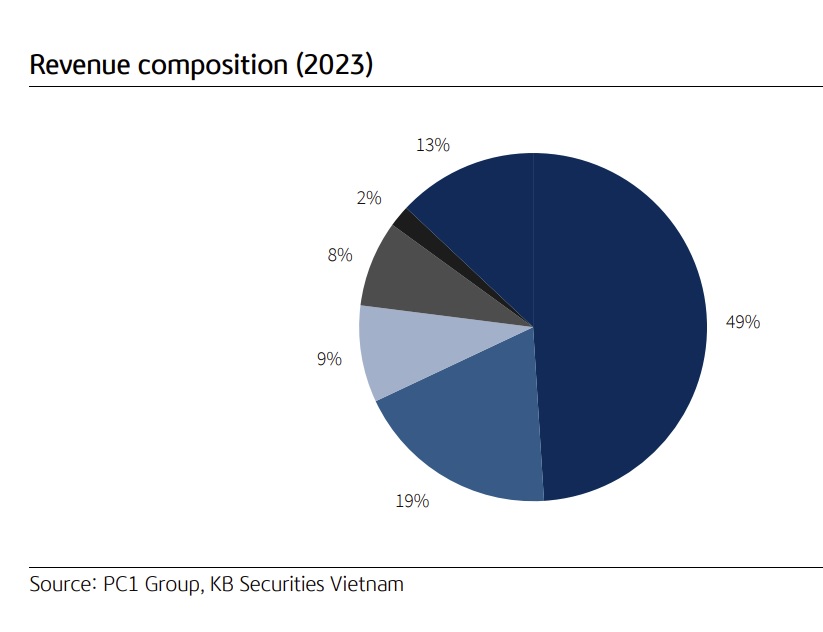

Industrial parks as PC1’s long-term growth driver

Industrial real estate is expected to ensure the longterm growth for PC1 Group Joint Stock Company (HoSE: PC1).

The value of new contracts signed in the first nine months of 2024 was VND4,838 billion, while the backlog in construction and industrial production at the end of September 2024 was VND3,970 billion. An EPC general contract for a 58.5 MW wind power facility was signed by PC1 and its Philippine partner last October. The project is anticipated to generate VND1,200 billion in revenue for PC1 overall in 2025 and 2026.

Due to (1) the group's promotion of non-EVN projects in overseas markets and (2) the revised Electricity Law passed at the end of November, which will speed up the approval of new projects, KBSV anticipated that PC1's industrial construction and production revenue would continue to recover, growing 28%/20% in 2024/2025. Additionally, the group anticipated that the demand for power plant and transmission line construction would increase steadily over the long term.

PC1's hydropower output in 2H24 has benefited from the El Nino to La Nina phase change, and it should continue to be high in 1H25. Business outcomes for the power sector will continue to be favorable: (1) wind power should remain steady, and the sector may record 1.1 billion kWh in 2024/2025F output; and (2) electricity prices are anticipated to rise by 2% annually on average.

PC1 is now completing site clearance for the implementation of two hydropower projects, Thuong Ha (13 MW) and Bao Lac A (30 MW), after completing legal procedures. With the completion of these two projects in 2H26, PC1's hydropower capacity should climb to 212 MW, a 25% increase over its current capacity. This would ensure medium- and long-term growth potential for the company's energy division.

After a sharp decline since the beginning of 4Q, nickel prices started to move sideways over concerns about Indonesia tightening its mining policy, the world’s largest nickel supplier. However, KBSV believed that nickel prices would not recover in the short term as nickel supply from major exporting countries remains abundant while demand from China remains weak, with an average price of USD16,600/ton in 2025 compared to an average of USD17,000/ton in 2024. PC1’s nickel output is expected to grow by 9% YoY as PC1 has secured a partner to ensure output while nickel demand continues to grow steadily.

In addition to Nomura 1 Hai Phong Industrial Park, whose occupancy rate reached nearly 100%, and Yen Phong 2A Industrial Park, which has started leasing since the beginning of this year, PC1 is developing nearly 400ha of industrial park land in Ha Nam, Hai Phong, and Bac Giang. It is expected that these projects will complete legal procedures and start leasing from 2026- 2027, contributing an average of about VND400-500 billion/year to PC1's profit.

The Golden Tower - Gia Lam residential real estate project with a scale of 1.5ha of commercial land including 183 villas and townhouses has completed land use fees and should start construction from late 2024-early 2025 and record more than VND1,600 billion in 2026-2027F.

“We believe that the short-term growth driver for PC1's business results will continue to come from the EPC and power segments, while the strong profit growth potential will be realized in the long term as the residential and industrial real estate are expected to increase their contribution to PC1's profits from 2026”, said KBSV.

Using SOTP for PC1 including (1) construction and installation activities, industrial production and energy, (2) mining segment, (3) residential real estate projects and (4) ongoing industrial park projects, KBSV recommended BUY for PC1 with a target price of VND30,300/share, equivalent to a potential return of 31% compared to the closing price on December 9, 2024.

Author: NGOC ANH

RECOMMENDED TOPICS