VN

VN

EN

EN

26/07/2026, 02:38

Business economics

The global air cargo outlook could be better from 2023

Although global goods trade has rebounded since May 2022, global air cargo transportation volume (tonne-kilometers, or CTKs) has not seen a recovery, causing 8M22 global CTKs to decrease 5.4% year over year.

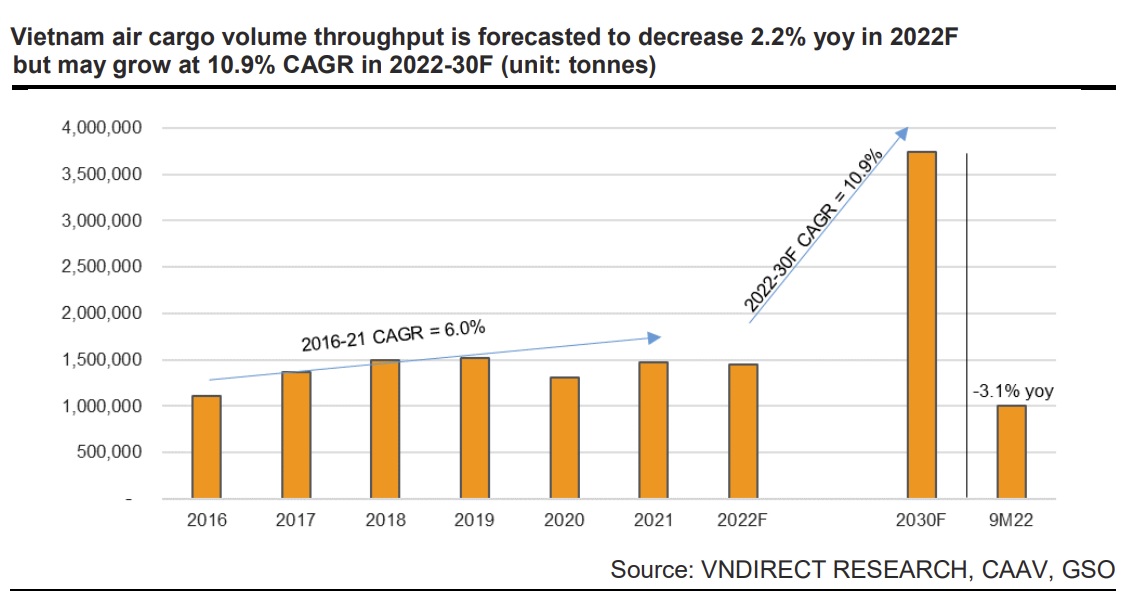

Vietnam's air cargo volume throughput in 9M22 decreased 3.1% year over year to 1 million metric tons.

>> Which challenges face airlines?

There are several reasons for the decrease in air cargo transportation.Air freight rates have now become less attractive. The global goods trade rebound is mainly attributed to strong activity in Latin America, where most of the uptake has benefited sea freight.

Besides, the new export orders from major markets—historically a leading indicator for air cargo shipments—maintained the downward trend as sanctions against Russia disrupted manufacturing in these markets. Chinese export orders also fell further below the 50-mark due to the zero-covid policy.

However, the most recent CTKs by route area data showed a rebound in some routes, including (1) within Asia and North America (Asia due to the relaxation of international travel restrictions in Asia) and (2) North America and Europe due to US support for Ukraine.

Following the difficulties of the global air cargo market, Vietnam's air cargo volume throughput in 9M22 decreased 3.1% year over year to 1 million metric tons.

Mr. Nguyen Dzung, senior analyst at VNDirect, expects the global air cargo market to improve beginning in 2023F. Because of this, further easing of COVID-19 restrictions in China, including factory reopenings, will also support the global air cargo market's recovery in the coming months. Meanwhile, international travel restrictions in Asia will continue to relax, allowing air freight capacity to expand and air freight rates to become more appealing.

"We expect Vietnam air cargo volume to remain flat in 4Q22F as (1) global geopolitical uncertainties and (2) rising inflation and interest rates may reduce global manufacturing, resulting in a 2.2% year-over-year decrease in 2022F air cargo volume."However, for the longer term, the Vietnam air cargo market still has a lot of growth potential with the government’s goal of becoming a "big factory" for the world. "CAAV estimates a 2022–30F air cargo volume CAGR of 10.9%," said Mr. Nguyen Dzung.

For the most promising business in the segment, SCSC Cargo Service Corporation (HoSE: SCS), Mr. Nguyen Dzung has the following assessments:

>> Risk of overloaded aviation infrastructure

In 9M22, SCS’ air cargo volume increased at a higher pace of 6.9% yoy, with a main contribution from international cargo volume (15.9% yoy), as the production of mobile phones and electronic devices remains strong. 9M22 revenue increased 13.7% year on year, with gross margin increasing 1.76% points due to increased international cargo with a higher service fee.With the contribution of financial income (68.5% yoy) thanks to a higher deposit, 9M22's net profit increased by 20.5% yoy. "For 2022F, we expect SCS’s NP to increase by 25.8% yoy as the 4th quarter is the peak season. "NP growth may slow down in 2023F (5.3% yoy) as the company is subjected to the normal tax rate of 20% from 2023F," said Mr. Nguyen Dzung.

Mr. Nguyen Dzung believes that in the long run, SCS will be able to capture Tan Son Nhat International Airport's (TIA) air cargo volume growth by increasing its current terminal capacity from 200.000 tpa to 350.000 tpa, whereas its sole competitor Tan Son Nhat Cargo Service Company JSC (TCS) has no room to expand (without taking into account the expansion plan, SCS's 2022F utilisation rate is estimated at 120%)."We believe air cargo terminal companies that are capable of expanding capacity like SCS will benefit from this steady growth," emphasized Mr. Nguyen Dzung.

Besides, SCS is providing the Airport Corporation of Vietnam (ACV) with insights on the air cargo terminal layout based on SCS’s experiences with the LTIA construction. Mr. Nguyen Dzung believes SCS has many advantages in bidding for the air cargo terminal at LTIA, and this is a strong upside risk for SCS.

Author: NGOC ANH

RECOMMENDED TOPICS