VN

VN

EN

EN

26/07/2026, 02:38

Business economics

Vietnam Economy Sustains Upward Momentum

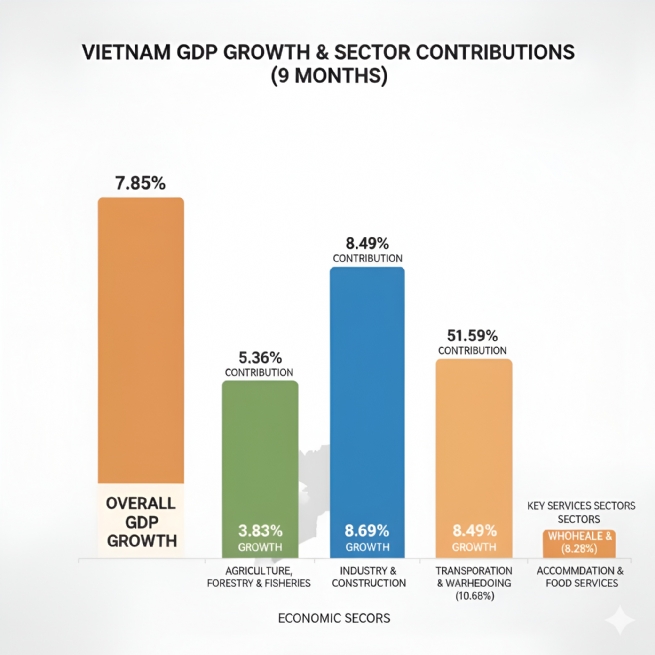

So far in 2025, Vietnam’s economy has demonstrated strong resilience, maintaining stable macroeconomic fundamentals, keeping inflation under control, sustaining a sizable trade surplus, and continuing to attract steady foreign direct investment (FDI) inflows.

However, challenges remain as domestic consumption grows slowly, private investment stays cautious, and public investment disbursement falls short of expectations, all adding pressure in the fourth quarter. A strong and timely policy push will be crucial to achieve the full-year GDP growth target of 8-8.5%.

As of the end of September, Vietnam's total import-export turnover reached US$680.66 billion, up 17.66% year-on-year

Bright spots amid challenges

Amid global headwinds of slower growth, rising trade protectionism, and heightened geopolitical risks disrupting supply chains, Vietnam has demonstrated strong economic resilience with positive macroeconomic indicators. According to the National Statistics Office (Ministry of Finance), average inflation in the first nine months stayed well below the target set by the National Assembly. As of August 2025, the Consumer Price Index (CPI) had risen 3.25% year-on-year, while core inflation increased 3.19%.

Foreign trade remains a major growth driver. As of the end of September, total import-export turnover reached US$680.66 billion, up 17.66% year-on-year. Exports totaled US$348.74 billion, a 16% increase from the same period in 2024, while imports reached US$331.92 billion, up 18.8%. The trade balance posted a surplus of US$16.82 billion in the first nine months. This outcome reflects the effectiveness of adopting higher quality standards and fully leveraging next-generation free trade agreements (FTAs), such as the EU-Vietnam Free Trade Agreement (EVFTA), which have helped lessen dependence on traditional markets.

The Index of Industrial Production (IIP) rose 7.7% year-on-year in the first nine months, driven mainly by the manufacturing and processing sector, which expanded 8.8%, and electricity production and distribution, which grew 9.4%. State budget revenue reached VND1.8879 quadrillion, up 27.9% year-on-year and equivalent to 96% of the full-year target.

Tourism and services maintained a strong recovery, attracting more than 13.9 million international visitors, up 21.7% year-on-year, supported by more flexible visa policies and a wider range of tourism products. The business sector also showed encouraging progress, with over 209,000 newly established and reactivated enterprises, a 24.5% increase from the same period last year. Following the implementation of Resolution 68-NQ/TW, an average of more than 19,100 new businesses were registered each month, nearly 48% higher than in previous months. By the end of August, over 209,240 enterprises had entered or returned to the market, surpassing the number of those exiting by 30%.

FDI inflows also increased in project numbers, with total registered capital reaching US$26.1 billion, up 27.3% year-on-year. However, the average registered capital per project has continued to decline, from US$5.09 million in the first quarter to US$4.35 million by August, indicating a significant structural shift.

According to economist Nguyen Bich Lam, the decline in average registered capital indicates a shift toward smaller and more dispersed projects instead of large-scale, high-impact investments. This trend may constrain technology and management spillovers while reflecting greater investor caution amid intensifying competition to attract high-tech and large-scale projects.

Public investment continues to serve as an important growth driver, with a record VND1 quadrillion scheduled for disbursement this year. To date, about VND410 trillion has been allocated, VND135 trillion higher than in the same period last year. However, this progress still falls short of the target of fully disbursing the planned public investment capital. Many key projects remain delayed due to administrative hurdles, site clearance difficulties, and limited management capacity following recent institutional restructuring.

Vietnam’s IIP rose 7.7% year-on-year in the first nine months, driven mainly by the manufacturing and processing sector

Q4 breakthrough expected

With encouraging results so far, the fourth quarter (Q4) of 2025 is expected to be a decisive period for achieving the full-year GDP growth target of 8-8.5% and setting the stage for 2026. According to the Ministry of Finance, Q4 GDP growth must reach 8-8.5% to meet the annual target. The Government has issued several directives to stimulate consumption, promote exports, and accelerate public investment disbursement.

Prime Minister Pham Minh Chinh emphasized the role of public investment, exports, and domestic consumption as the main drivers of economic growth. In particular, fully disbursing the planned public investment capital, equivalent to VND1 quadrillion, is considered crucial for stimulating demand and mobilizing broader social resources.

To achieve the growth target, the Government has set out several key priorities: maintaining macroeconomic stability and keeping inflation under control through flexible coordination of fiscal and monetary policies; accelerating public investment disbursement by removing administrative and site clearance obstacles; supporting enterprises by lowering capital costs and improving the business environment; enhancing the quality of FDI with a focus on high technology and clean energy; and speeding up digital transformation while promoting the development of a green economy.

Author: VBF

RECOMMENDED TOPICS