VN

VN

EN

EN

26/07/2026, 02:38

Business economics

Vietnam is on track for recovery

Despite a rosy picture, risks to trade and inflation warrant a closer look; HSBC expects growth to accelerate to 6.0% in 2024.

HSBC expects Vietnam's GDP growth to accelerate to 6.0% in 2024.

>> Efforts needed to achieve economic growth target of 6-6.5%

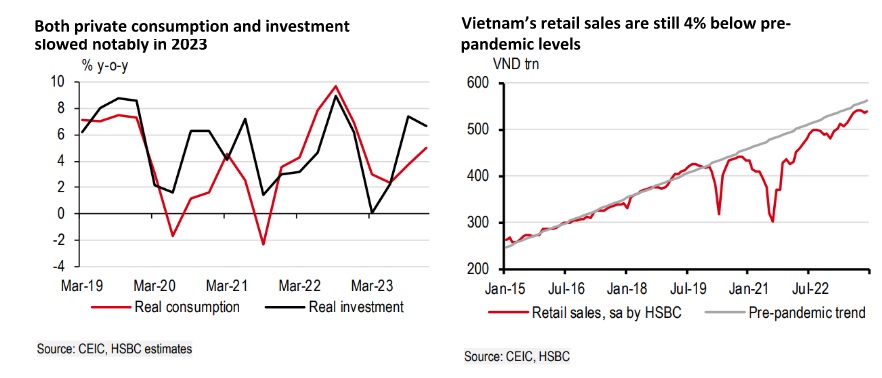

As Vietnam bids farewell to the challenges posed by the Year of the Cat, it is ushering in a more hopeful Year of the Dragon. The most important factor is the added capacity in trade from sustained FDI inflows, which provides hope for its external sector when the trade cycle turns. While the trade cycle is mostly a near-term consideration, FDI reflects the medium- to long-term confidence of investors.

Vietnam has been widely regarded as the main beneficiary of US-China trade tensions, a trend that continues to hold. Both total and new FDI reached close to their respective historical highs in 2023, particularly with greenfield FDI jumping to a four-year-high of c5% of GDP. Notably, new manufacturing FDI soared to a new high of more than US15bn, 80% of which is concentrated in the manufacturing space. This continues to put Vietnam in a leading position in ASEAN, just behind Malaysia.

Looking at the source of FDI, one interesting trend is worth noting. Japan and Korea are both traditionally big investors in Vietnam, but China has been expanding its FDI footprint quickly in Vietnam. In fact, 2023 marks the first time that mainland China has the largest share among investors, beating its two neighbours. Combined, Greater China accounted for almost half of Vietnam’s new FDI inflows in 2023. Not surprisingly, the lion’s share went to electronics, a sector that Vietnam is fast becoming a rising star in. This is also an area where FDI inflows are more diversified, a reflection of Vietnam’s increasing significance in the global tech supply chain. Outside of electronics, investors are increasingly being drawn to Vietnam’s promising consumer market, a trend heralded by Japanese corporates.

In terms of FDI, a key development to watch closely for in 2024 is the implementation of a minimum 15% corporate tax rate for multinational corporations (MNCs), effective 1 January. Recall, back in October 2021, more than 135 jurisdictions agreed to a two-pillar solution (Base Erosion Profit Shifting: BEPS) to reform the international tax framework to address the challenges from the taxation of the digital economy. Under BEPS Pillar II, MNCs with revenue of more than EUR750m (USD825m) are set for a global minimum tax at 15%. The EU and some other countries plan to introduce Pillar II from 2024 while others have signalled their willingness from 2025. In Vietnam, 122 foreign companies will face a steep rise in their tax costs, which is estimated to generate revenue worth USD600m per year.

>> Vietnam prioritises driving growth momentum this year: Cabinet

Long before the National Assembly’s approval of the minimum corporate tax rate, concerns have been raised by MNCs operating in Vietnam. The most notable example is Samsung, who is of crucial importance to Vietnam’s economy. It is not only the single largest foreign investor in Vietnam, with its exports alone expected to account for 13% of GDP in 2023, but also three of its affiliates are in Vietnam’s top 10 foreign taxpayers. Evidently, the tax hike is on Samsung’s agenda, with high-level representatives having been sent to meet with policymakers in early 2023.

“While it may still be too early to evaluate the implications, the impact should be manageable, in our view. How the additional tax revenue will be managed as well as whether subsequent measures or other incentives will be introduced to offset the tax hike will be closely monitored. At the same time as the greenlighting of the tax hike, the authorities are also planning to work on specific incentives in 2024”, said HSBC.

In HSBC’s view, when it comes to investment decisions, tax is a key factor, but it is not the only factor in determining FDI inflows. It is thus important to improve on other metrics, such as infrastructure connectivity, the availability of a skilled workforce, the ease of doing business, and free trade agreements, to name a few. In addition, Vietnam is not the only country that is set to introduce a similar minimum tax rate. Its ASEAN peers are also working towards similar goals.

Elsewhere, inflation is also worth watching. Fortunately, Vietnam’s inflation was under control in 2023, averaging 3.3%, which in line with our expectations. This leaves plenty of space below its inflation ceiling of 4.5%. HSBC expects inflation to remain benign in 2024, with a forecast of 3.4%, well below the new inflation target of 4-4.5%. Despite the broad disinflation trend in Vietnam, price pressures have not faded completely. Upside risks to inflation from energy and food remain, particularly given Vietnam’s sensitivity to these items as indicated by their sizeable weights in the inflation basket. In addition, the rise of healthcare costs warrants close attention, as Vietnam has resumed the changes in national medical service pricing after a period of four years. While maintaining an eye on upside risks to prices, HSBC expects the SBV to keep its policy rate steady at 4.50% thorough 2024.

All in all, HSBC believes Vietnam is on track for recovery, likely returning to its trend growth of 6.0% in 2024. As FDI inflows continue to add production capacity, Vietnam’s manufacturing sector is experiencing the green shoots of a rebound, bringing opportunities for its exports. While it is key to watch how the minimum 15% corporate tax rate evolves, the impact should be manageable.

Author: NGOC ANH

RECOMMENDED TOPICS