VN

VN

EN

EN

11/07/2026, 07:27

Business economics

Exchange rate pressures remain in 2026

The US dollar is supported by expectations that the Fed will continue delaying rate cuts for several more months. This will press on the USD/VND rate in 2026.

DXY has surged sharply since the Middle East conflict escalated

DXY has surged sharply since the Middle East conflict escalated; markets have significantly lowered expectations for Fed rate cuts. At the start of the month, the DXY stood at 97, with the US dollar mainly trading in a narrow range around 96-97 during February. By month-end, the DXY rose 0.6% from the end of January to 97.6, marking its first monthly gain since October 2025.

This uptrend was driven by expectations that the Fed would continue to hold rates amid persistent inflation, with February CPI rising 2.4%—above the 2% target. According to the FOMC meeting minutes in March, the Fed kept the federal funds rate unchanged at a target range of 3.50%–3.75% at the March 17–18 Federal Open Market Committee (FOMC) meeting. Only Governor Stephen Miran dissented in favor of additional easing, while Governor Christopher Waller—who had been seen as another likely dissenter given weak labor market conditions—aligned with the consensus. This signals increased concern among policymakers about the inflation implications of the Middle East conflict.

Fed Chair Jerome Powell said little and appeared non-committal during the press conference. He reiterated that, with policy close to neutral—or even slightly restrictive—the Fed is in a good position to “wait and see” how yet another supply shock will influence economic activity. He emphasized that the first shock to monitor is tariffs and noted that, while the implications of the Middle East conflict remain “uncertain,” inflation is likely to move higher.

Additionally, the US dollar's rise was fueled by renewed safe-haven demand following the outbreak of the US-Iran conflict. By mid-March, the DXY had climbed to a 10-month high of 100.36 (2.8% from end-February, 2.1% ytd). Besides safe-haven sentiment, the US dollar's strength was reinforced by expectations that the Fed would continue delaying rate cuts amid heightened inflation risks from sharply rising oil prices.

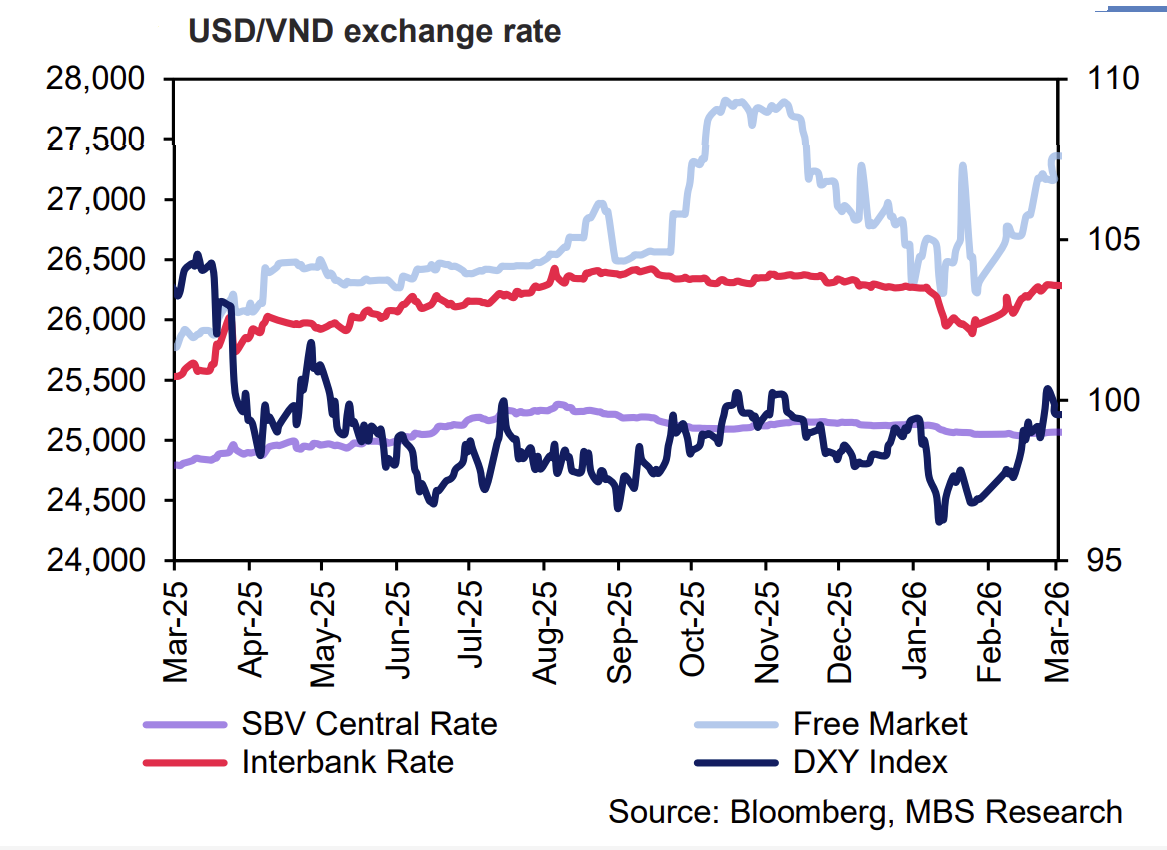

The USD's recovery exerted some pressure on the USD/VND exchange rate in February. Specifically, by the end of Feb, the interbank exchange rate rose 0.4% mom to 26,058 VND/USD (-0.8% ytd). The free-market rate surged 0.85% during the month to 26,700 VND/USD (-0.8% ytd). Meanwhile, the central rate eased slightly by 0.1% mom, reaching 25,044 VND/USD by the month-end (-0.3% ytd). Exchange rate pressure became even more pronounced in the first half of March amid the strong surge in the USD. By mid-March, the interbank rate had risen 0.9% from the end of February to 26,287 VND/USD (0.06% ytd). Meanwhile, the freemarket rate surged 2.5% to 27,365 VND/USD (1.6% ytd).

MBS believed exchange-rate pressures would remain in 2026. First, imports are expected to grow in tandem with exports in 2026, primarily driven by rising imports from the US as Vietnam continues to narrow its bilateral trade deficit. As of February, the merchandise trade balance has recorded three consecutive months of deficits, with a cumulative deficit of nearly USD 3 billion in the first two months of 2026.

Second, global gold prices are forecast to continue rising to the range of 6,000 - 6,300 USD/ounce this year amid escalating Middle East tensions and heightened safe-haven demand.

Third, the DXY reversing to resume its uptrend as its safe-haven role is restored will create significant pressure on the USD/VND rate in the near term. In addition, the US dollar is supported by expectations that the Fed will continue delaying rate cuts for several more months; some Fed officials have even expressed support for rate hikes if inflation does not cool as anticipated. Against this backdrop, MBS projected the USD/VND exchange rate to fluctuate around 26,200 - 26,400 (0.5% ytd) in Q1 and Q2/2026. It also expected the exchange rate to rise by 2.5% - 3% in 2026.

Author: NGOC ANH

RECOMMENDED TOPICS