VN

VN

EN

EN

22/07/2026, 02:38

Investment

Solutions to close the Vietnam’s infrastructure financing gap

To close the infrastructure gap, Vietnam must scale market innovation and build investor confidence in bonds as a viable, long-term funding tool.

Vietnam’s infrastructure ambitions—estimated at USD 245 billion through 2030—depend on unlocking long-term private capital. With public funding falling short and bank lending constrained, the corporate bond market is emerging as a critical financing channel. Recent regulatory reforms, along with stronger disclosure, credit ratings, and guarantees, are laying the groundwork for deeper investor participation.

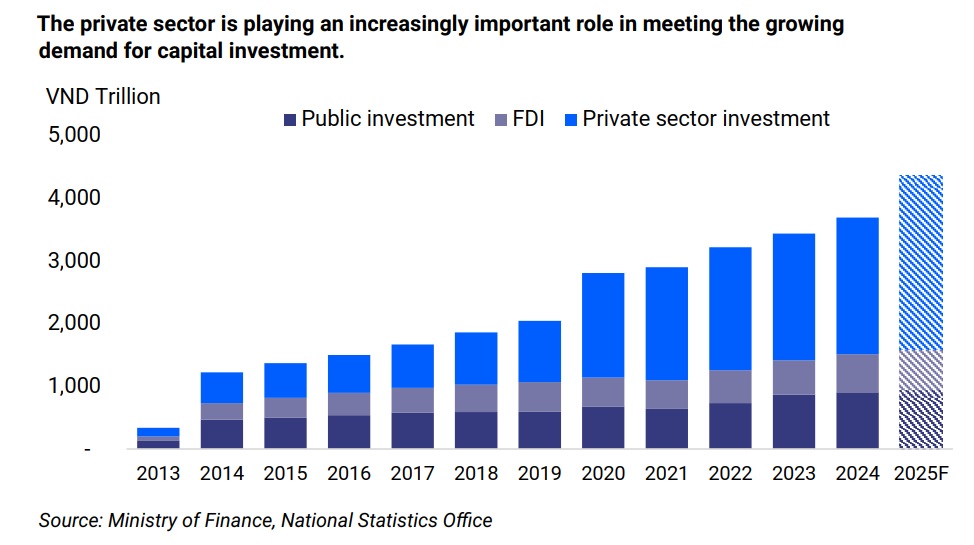

Vietnam’s infrastructure ambitions hinge on mobilising private capital through the corporate bond market. Between 2025 and 2030, the country will need an estimated USD 245 billion for expressways, high-speed rail, and power projects—yet public funding can only cover 70%. Private investment has already become a key driver, accounting for over half of registered fixed asset investment.

As bank lending tightens, due to regulatory limits on using short-term deposits for long-term loans—the role of the bond market becomes even more critical. Bank credit to toll road projects, for instance, has declined by 6% annually since 2020. To close the infrastructure financing gap, in VisRating’s view, Vietnam must deepen its corporate bond market and attract long-term private capital.

Vietnam’s bond market is gaining traction as a key channel for infrastructure financing. Recent regulatory reforms are paving the way for project companies to issue bonds more flexibly—such as through private placements without historical financials under the amended PPP Law. The state is also stepping in with higher equity contributions to ease debt burdens and improve credit quality.

“A forthcoming decree is expected to further unlock the market by allowing public offerings and immediate listings of infrastructure bonds. While issuance conditions will be eased, post-issuance controls—such as trustee oversight, escrow accounts, and regulated disbursements—will tighten, creating a more robust legal framework”, said VIS Rating.

Meanwhile, new requirements on disclosure, issuance standards, and mandatory credit ratings are boosting transparency and investor confidence. Together, these reforms position corporate bonds as a more viable, long-term funding tool for Vietnam’s infrastructure ambitions.

Accoring to the VIS Rating, credit guarantees and credit ratings are crucial tools for unlocking private capital for infrastructure development. Infrastructure projects often carry weaker credit profiles due to high leverage, single revenue streams, and exposure to construction risks. Limited track records and restricted access to project agreements further complicate investor assessments. Long tenors—often 15 to 20 years—also heighten liquidity risk.

Credit guarantees provide support to project bond issuers, thereby enhancing credit quality and reducing bondholders’ exposure to project-related risks. CGIF’s regional portfolio, including several infrastructure projects in Vietnam, demonstrates how credit guarantees can support project owners in broadening their investor base and facilitating access to capital markets.

“Credit ratings help bridge information gaps on complex projects and project bonds by providing independent assessments of creditworthiness and tracking project progress. They also evaluate guarantees, collateral, and tranche structures—setting clearer benchmarks for risk pricing and improving bond market liquidity”, emphasized VIS Rating.

Together, guarantees and ratings are essential tools for scaling infrastructure bond issuance and attracting long-term private capital.

Author: NGOC ANH

RECOMMENDED TOPICS