VN

VN

EN

EN

09/07/2026, 11:15

Investment

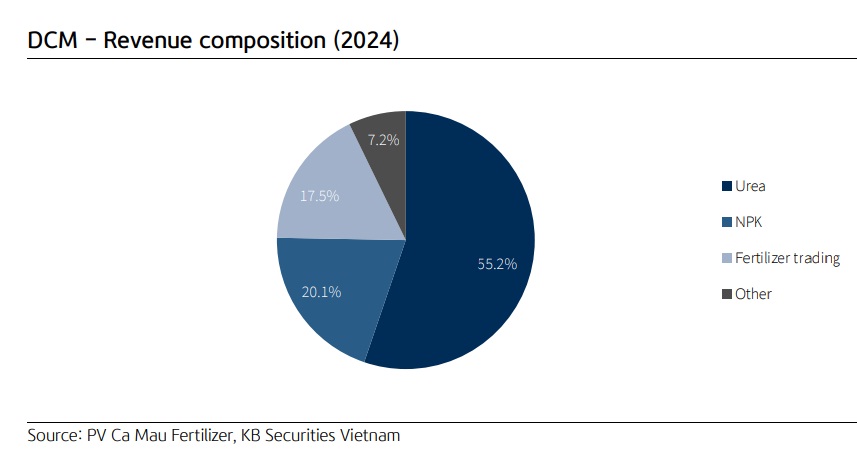

Strong urea prices to propel DCM's earnings outlook

Petro Viet Nam Ca Mau Fertilizer JSC (HoSE: DCM)’s medium-term growth outlook is fueled by: (1) a 25% capacity expansion in the urea segment, (2) an increase in NPK market share to 17% following the acquisition of Korea-Vietnam Fertilizer Co., Ltd (KVF), up from the current 7%, and (3) strategic investment in an industrial gases and chemicals project, according to KBSV.

Main catalyst for profit

As of end-July 2025, urea prices in the Middle East and China had risen by 36% and 74% YTD, respectively. The rally was driven by: (1) production disruptions amid tight gas supply and elevated gas prices caused by geopolitical tensions involving the EU–Russia and Israel–Iran, and (2) strong domestic demand in India since the start of the year, and (3) the enforcement of EU import tariffs on urea from Russia and Belarus effective July 1, 2025 (Table 03). Benefiting from these favorable international market dynamics, DCM’s domestic wholesale urea prices have climbed 30% YTD (Agromonitor), boosting 1H2025 performance with adjusted NPAT-MI up 32% YoY to VND1,168 billion.

Looking ahead, we expect urea prices to remain elevated, backed by: (1) continued gas supply constraints in the EU and Middle East amid geopolitical tensions, (2) robust demand growth in India projected for 2H2025 on the back of tight supply, and (3) stronger EU import demand ahead of potential price hikes following additional tariffs. KBSV forecasts DCM’s average urea selling price at VND11,400/kg in 2025 (20% YoY and VND11,300/kg in 2026 (flat YoY).

Brent crude oil and fuel oil (FO) prices have declined by 9% and 7% YTD, respectively, resulting in a 6% YTD reduction in DCM’s natural gas costs. Favorable input prices lifted DCM’s gross margin to 22% in 1H2025 compared with 20% in the same period last year. Over the long term, DCM plans to secure new gas purchase agreements with a revised pricing mechanism, adding USD1/mmBTU for volumes sourced from VIEG and Petronas. Management believes the new contract terms to remain more competitive than other domestic gas sources, thereby strengthening DCM’s sustainable cost advantage.

In the near term, KBSV expects Brent crude prices to average USD68/65 per barrel in 2025/2026, in line with market consensus. Accordingly, KBSV forecasts DCM’s gross margin to reach 22.1%/22.7% in 2025/2026, supported in part by VAT refunds of VND102 billion in 2H2025 and VND205 billion in 2026, following the implementation of the amended VAT Law on fertilizers effective July 1, 2025.

Stable demand, urea expansion, and NPK optimization

DCM’s domestic urea market share is estimated at 32%, with its share in the Southeast region climbing to 72% by end-2Q2025 (vs. 61% in the same period last year). In 1H2025, DCM’s urea export volume rose 29% YoY to 225 thousand tons, with Cambodia contributing 34% of total exports, where DCM captured a 40% market share as of 2Q2025. KBSV projects DCM’s urea sales volume at 851/890 thousand tons in 2025/2026, representing 6%/5% YoY growth.

For the 2025–2030 period, DCM targets to raise its urea production capacity to 1 million tons per year (a 25% increase from the current level) to reinforce long-term competitiveness. Following the KVF merger, which lifts total capacity to 660 thousand tons per year, DCM also aims to expand its domestic NPK market share to 17% (vs. 7% currently). In addition, the company intends to invest in an industrial gases and chemicals project, which will process N₂, O₂, Ar, H₂, and CO₂.

Attractive dividend yield

In 2025, management plans to distribute a cash dividend of VND2,000 per share, implying a relatively attractive dividend yield of 4.8%. KBSV estimates DCM’s adjusted NPAT-MI at VND2,081/1,981 billion in 2025/2026 (64%/-3% YoY). Backed by robust earnings growth, DCM’s cash dividend is expected to rise to VND2,500 per share in 2025, equivalent to a 6% yield based on the current market capitalization.

However, in KBSV's view, DCM has faced some risks. First, China is expected to resume urea exports during May–September 2025, with an export quota capped at 4 million tons. Although the export volume remains relatively modest, the policy reversal signals a potential risk, which could exert downward pressure on urea prices in 2026 should the quota be further relaxed.

Second, escalating geopolitical tensions between Russia–Ukraine or Israel– Iran could drive oil prices higher. This, in turn, would push natural gas prices up again, squeezing DCM’s profit margins.

Author: Ngoc Anh

RECOMMENDED TOPICS