VN

VN

EN

EN

21/07/2026, 02:38

Business economics

USD/VND in 2026 may increase less than in 2025

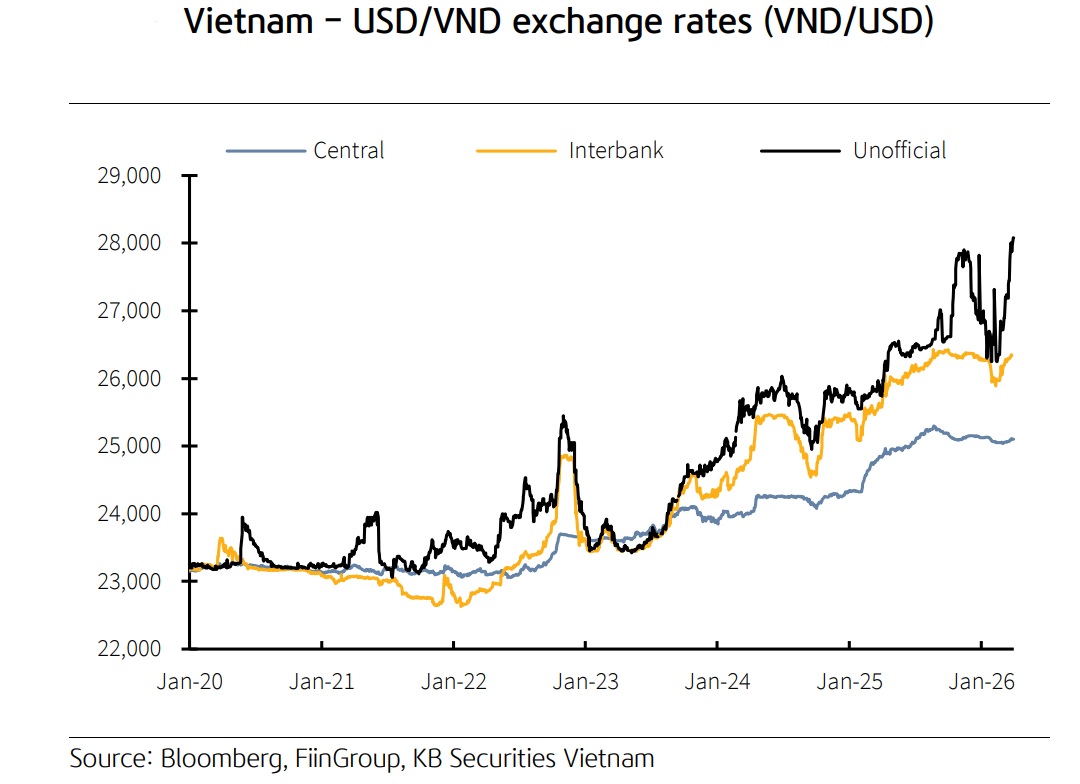

In 2026, KBSV forecasts the USD/VND exchange rate to increase by 2.5-3%, lower than the 2025 increase (+3.5% YTD) due to some factors.

USD/VND in 2026 may increase less than in 2025

Pressure from the US-Iran conflict

The cooling of the USD/VND exchange rate from the end of last year continued in the first half of 1Q26 (interbank exchange rate dropped 1.6% YTD) thanks to (1) increased demand for VND before the Lunar New Year holiday, (2) remittances flowing into the country, and (3) the DXY falling to around 96-97 points. The possibility of foreign exchange intervention from the Fed to support the JPY and statements by President Donald Trump regarding tax policy triggered USD sell-offs.

However, the situation quickly reversed when geopolitical tensions in the Middle East occurred at the end of February, triggering risk-averse sentiment and causing capital to flee into safe assets such as the USD and US Treasury bonds, thereby sending the DXY higher to 99-100 points. At the same time, the sharp rise in oil prices weighed on US inflation, reducing the Fed's room for monetary policy easing, thereby putting pressure on the USD/VND exchange rate. From the time the conflict broke out until the end of the first quarter, the interbank and central USD/VND exchange rates recorded increases of VND282 and VND58, respectively.

However, compared to the high comparative base from the end of 2025, 1Q interbank exchange rate grew by a mere 0.1% YTD, recorded at VND26,340/USD, while the central exchange rate came in at VND25,102/USD (-0.1% YTD). The State Bank of Vietnam (SBV) intervened and kept interbank interest rates at a high level (through continuous net withdrawals via the OMO channel in March) and cancelled 180-day foreign exchange sales with a total foreign exchange reserve of over USD2 billion.

The unofficial exchange rate showed a similar trend, with stronger fluctuations due to its sensitivity to macroeconomic variables. The unofficial exchange rate reached a historical peak during the last two trading sessions of 1Q, reaching VND28,080/USD (4.7% YTD). Furthermore, the widening gap between domestic and international gold prices to VND20-30 million/ounce stimulated speculation and gold smuggling, directly pushing up the unofficial rate.

This situation is expected to gradually improve as the SBV’s policies aimed at strengthening control over the gold market gradually permeate gold trading and business activities. Besides Decree 232/2025/ND-CP (effective from October 10, 2025) aiming to eliminate the state monopoly on gold bar production and expand gold imports, Decree 340/2025/ND-CP (effective from February 9, 2026) has added penalty frameworks to tighten control over related violations. In addition, the establishment of a gold exchange is still being expedited to finalise the proposal and is expected to be piloted in 2026.

According to our calculation model, NEER is the multilateral nominal exchange rate measuring the value of the VND against a basket of eight reference currencies under the central exchange rate mechanism, and REER is the multilateral real exchange rate, an inflation-adjusted index relative to NEER. In 2Q26, the NEER recorded a slight uptrend (1% YTD) after a sharp decline in 2025, reflecting less depreciation of the VND against its trading partners. The weakening of major counter currencies such as the EUR, JPY, and KRW stemmed from global economic concerns arising from US-Iran tensions. For the REER, the higher increase (2.5% YTD) indicates that domestic inflationary pressure is exceeding the average of countries in the benchmark basket, thereby reducing the competitiveness of Vietnamese export goods.

Outlook for 2026 USD/VND exchange rate

KBSV believes the DXY index will remain in the high range of 97-102 points in the first half of 2Q26 as the Fed's policy easing space has narrowed considerably after escalating tensions in the Middle East. March 2026 data showed the US CPI reached 3.3%, growing 90bps from the previous month, clearly reflecting the strong impact of the current macroeconomic situation. At the same time, the position of the USD is strengthened by capital flows seeking safe-haven assets amidst complex war developments.

However, in the second half of 2Q26, although there may be some intermittent recovery periods, the DXY index is likely to be in a downward trend due to (1) the scenario of de-escalation of the war and the downtrend of oil prices and (2) expectations over another Fed rate cut while major central banks like the ECB and BOJ may move to an interest rate hike phase for the remainder of 2026.

In 2026, KBSV forecasts the USD/VND exchange rate to increase by 2.5-3%, lower than the 2025 increase (3.5% YTD) as the exchange rate is supported by positive factors such as (1) the DXY index will tend to decline in the second half of 2026 as the Middle East conflict cools down (mentioned above). (2) The VND-USD interest rate differential continues to remain positive, creating a natural barrier to speculation. (3) The prospect of upgrading to a secondary emerging market in FTSE Russell's September 2026 stock market review will lure capital flows from international ETFs and active funds into the Vietnamese market, with the expected capital size ranging from USD3–9 billion. (4) The recovery of FDI flows thanks to the wave of restructuring of global supply chains before the US-China trade tensions, especially in the high-tech industry, which is currently in the priority group for exemption from US tariffs. (5) Timely intervention by the SBV through liquidity regulation, forward foreign exchange sales, foreign exchange swaps and other tools to stabilise the exchange rate.

However, KBSV believes that there are still risks that could put pressure on the USD/VND exchange rate, including (1) the forecast that gold prices may soon return to the peak of the beginning of the year (around USD 5,200 - 5,400/ounce) along with increased domestic gold import demand and (2) the easing of the money supply by the SBV to lower interest rates and stimulate economic growth.

Author: NGOC ANH

RECOMMENDED TOPICS