VN

VN

EN

EN

21/07/2026, 10:30

Investment

Vietnam Real Estate Investment Strategy 2026: Navigating A Repricing Cycle

Vietnam’s real estate market is entering a repricing cycle in 2026, shaped by interest rates, selective credit conditions and regulatory changes. This article explores how investors can reassess risk, liquidity and long-term value creation to build a more disciplined real estate investment strategy in a selective market.

SwanBay project in Dong Nai

Real Estate Remains Relevant in a Volatile Investment Landscape

According to the Savills Impacts report, the global economy has entered a period of heightened volatility over the past five years, characterized by the return of inflation, a higher interest rate environment, and increased uncertainty. At the same time, rapid technological advancement, economic fragmentation, and geopolitical tensions are reshaping how markets operate.

This marks a clear departure from the relatively stable "Great Moderation" era, when macroeconomic conditions remained predictable for an extended period. Today, many traditional market assumptions and investment behaviors are shifting, rendering previous frameworks less applicable.

Martin Towns, Global Head of Real Estate at M&G Investments, observed, "Real estate has tested the patience of investors in recent years, but it is now firmly back on the agenda for asset allocators."

Following a period of underperformance relative to public markets – and, in some cases, significant value destruction that has been driven by structural change—the asset class has reset.

As capital returns to the sector, we are seeing the fundamental strengths of real estate reassert themselves. Income, diversification, and inflation linkage are once again differentiating property—and this is happening at a time when equities and bonds are increasingly moving in tandem, and geopolitical risk continues to inject volatility into the public markets.

Valuations have adjusted meaningfully, prompting an improvement in the relative appeal of real estate. However, the performance of assets will not be uniform. Returns will be driven by selectivity: investing in places that endure and buildings that are capable of meeting the complex needs of a changing economy.

“The opportunity is clear, but investors who want to make the most of it will need to take an active, disciplined approach. There is no room at all for complacency: this will not be a market that rewards passive capital,” said Martin Towns.

Three Key Shifts Shaping Vietnam's Property Market

In Vietnam, according to Nguyen Le Dung, Head of Investment Advisory at Savills Hanoi, the market is experiencing three key shifts: rising interest rate pressure, a mismatch between credit and capital flows, and significant changes in the legal framework.

From an interest rate perspective, elevated VND borrowing costs are encouraging both buyers and investors to adopt a more cautious and long-term approach. At the same time, credit has become more selective as banks rebalance liquidity, requiring developers to strengthen capital structures and improve transparency.

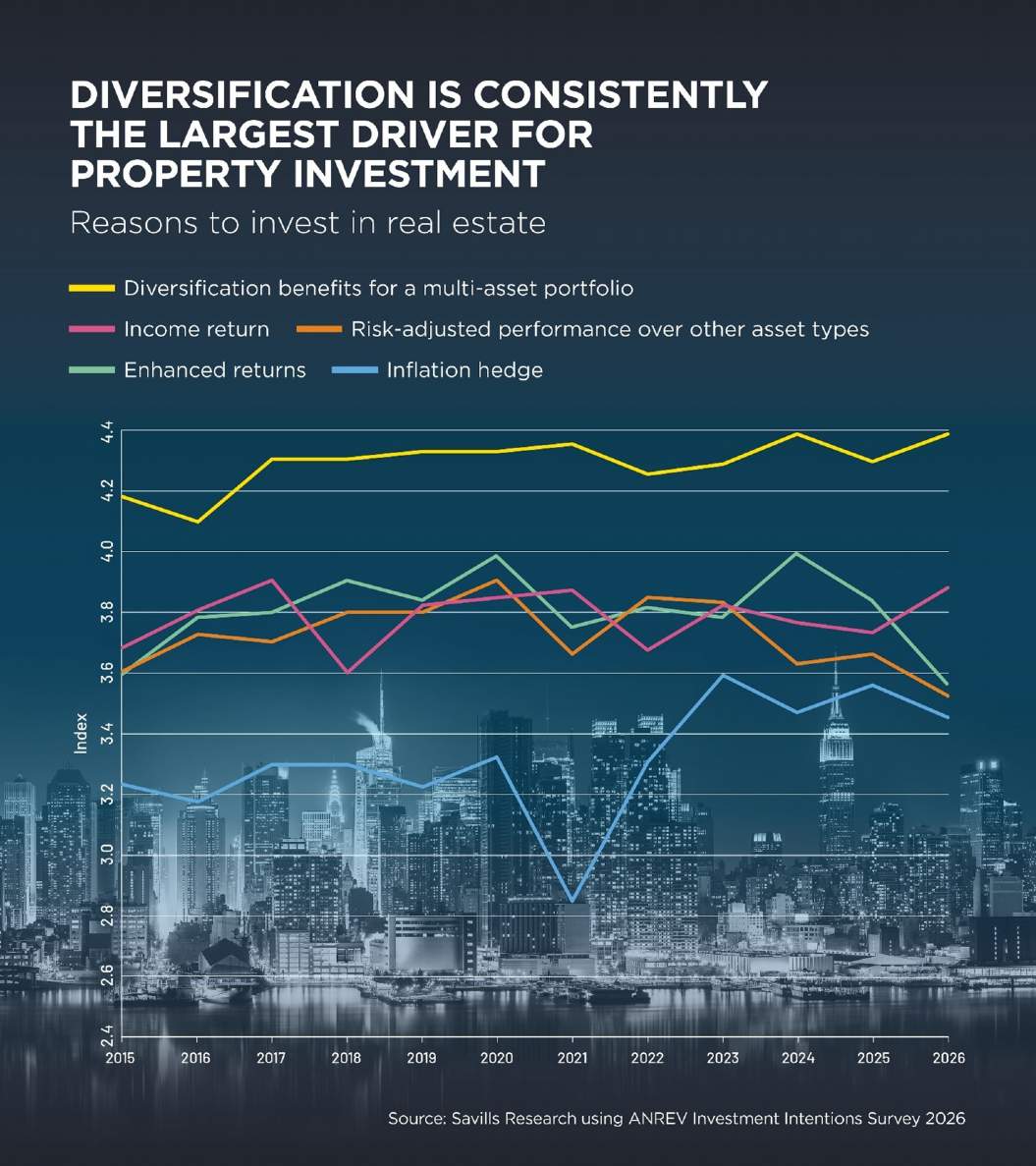

Savills Diversification Is Consistently The Largest Driver For Property Investment (Source: Savills Research)

On the regulatory side, the new land pricing framework may increase development costs. However, alongside procedural reforms and a long-term planning orientation, it also lays the foundation for larger, more structured developments.

Meanwhile, supply continues to shift towards suburban areas and satellite cities, contributing to greater price segmentation and improving the market's ability to meet genuine housing demand.

Investment Strategies for Vietnam’s Selective Real Estate Market

Against this backdrop of market rebalancing, Savills Vietnam experts suggest that developers should adjust their strategies to better align with genuine housing demand, particularly in the affordable segment, to sustain liquidity and absorption.

At the same time, portfolio restructuring towards income-generating assets, such as offices, hotels, and serviced apartments, is expected to help mitigate cyclical risks and enhance long-term operational resilience.

This adjustment phase also opens M&A opportunities for long-term investors, particularly in gaining access to land banks and projects with strong fundamentals that are currently capital-constrained.

For homebuyers and individual investors, the focus is gradually shifting away from short-term capital gains towards long-term asset accumulation and income generation.

As Vietnam’s real estate market moves through a repricing cycle, projects with clear legal status, transparent development timelines, and strong developer track records are likely to stand out. For investors, a disciplined and well-informed real estate investment strategy will be essential to identifying resilient opportunities in an increasingly selective market.

Author: Savills Vietnam

RECOMMENDED TOPICS