VN

VN

EN

EN

21/07/2026, 02:38

Business economics

What drives container throughput growth?

Vietnam's positive import-export outlook is driving container throughput growth, supported by the successful capacity expansion at its major ports.

Nam Dinh Vu port complex

Amidst a volatile global trade environment in Q1/2026, marked by US tariffs and Middle Eastern tensions, Vietnam’s import-export activities have maintained robust growth. Specifically, total trade turnover reached USD 249.5 billion, a 23% increase YoY. According to VPA data, container throughput across the seaport system in Q1/2026 is estimated at approximately 6,8 million TEUs, up roughly 12.1% YoY. The primary catalyst was the US adjustment of global tariffs to a temporary 15% for a 150-day period, which allowed Vietnam’s strategic exports, such as textiles and furniture, to preserve their competitive edge over rivals. This supported exporters in securing a stable order book through the end of Q3/2026.

MBS expects Vietnam's trade activity to sustain this strong momentum as US importers accelerate inventory stockpiling within this 150-day window. This is further bolstered by the ongoing "China 1" trend, driven by core macro fundamentals such as competitive labor costs, high economic openness through an extensive FTA network, and synchronized improvements in national logistics infrastructure.

This stock company has upwardly revised the total throughput across GMD's entire port system (including Gemalink) by 9.3% and 6.4% compared to its previous forecasts. After such a revision, throughput is projected to reach approximately 5.8 million and 6.4 million TEUs, representing growth of 17% and 10,1% YoY, respectively:

Regarding the Nam Dinh Vu port complex, MBS has upwardly revised the utilization rates by 7.3 percentage points and 7.9 percentage points compared to our previous forecasts, reaching approximately 107.3% and 121.4%. It expects Nam Dinh Vu Phase 3 to rapidly ramp up its utilization to 70% driven by (a) absorbing overflow cargo from Phases 1 and 2; and (b) expanding new service routes to offset volumes shifting to the Lach Huyen area.

Furthermore, GMD will continue upgrading the Ha Nam canal, deepening the berth depth to -9.5m. This will make Nam Dinh Vu the only terminal in the Cam River region capable of receiving vessels of approximately 55,000 DWT (equivalent to vessel sizes of 4,500 – 5,000 TEUs). Post-adjustment, total container throughput for the entire Nam Dinh Vu port is projected at approximately 2.04 million and 2.31 million TEUs, representing growth of 35.7% and 13.1% YoY for the 2026/2027 period, respectively. Additionally, backed by its superior competitive advantages, MBS maintained its expectation that Nam Dinh Vu will sustain higher service fees than regional competitors, with a projected increase of approximately 7% per annum during 2026-2027.

Regarding the Southern port cluster, MBS has upwardly revised throughput by 5.5% and 4.3% compared to its previous forecasts; after such an adjustment, volume is projected to reach 1.7 million and 1.8 million TEUs, representing growth of 9.6% and 2.9% YoY, respectively. It is believed the Southern port cluster will continue to serve as an extended arm, collecting and transshipping the abundant cargo from the Gemalink deep-sea port, which is currently operating at over 130% of its design capacity.

Furthermore, GMD’s proactive efforts to directly link satellite ports with the Cai Mep – Thi Vai cluster via a dedicated feeder barge system will enhance operational efficiency for the Southern cluster. This strategy supports the cluster in effectively absorbing the strong influx of FDI cargo flowing into industrial parks in Binh Duong and Dong Nai.

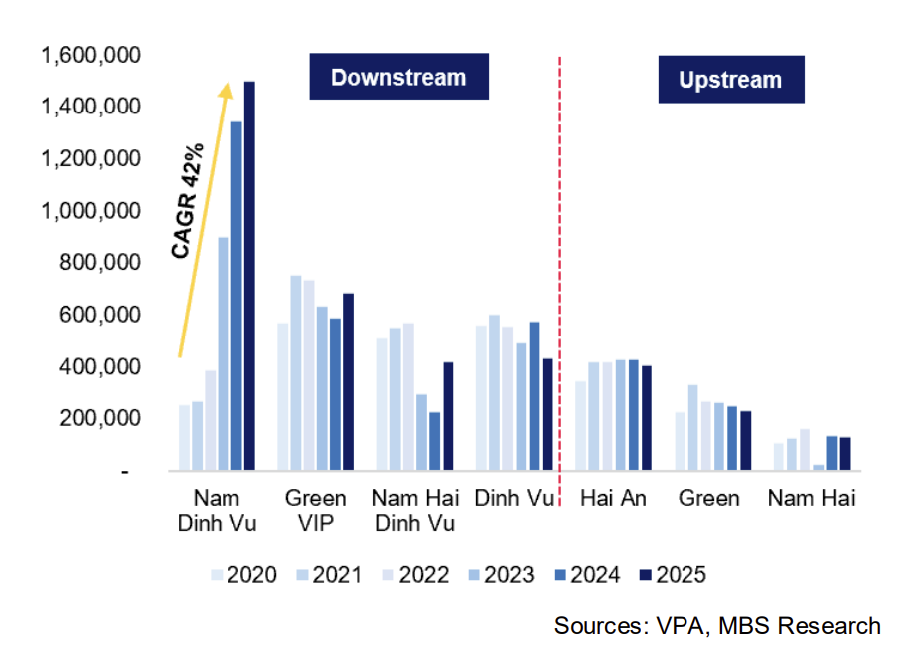

Over the past five years, Nam Dinh Vu has been the port with the most robust throughput growth, driven by its superior competitive advantages.

Regarding Gemalink, MBS has upwardly revised its throughput by 14.8% and 7.4%; after adjustment, volume is projected to reach approximately 2.1 million and 2.4 million TEUs, representing growth of 8.3% and 13.1% YoY for the 2026/2027 period, respectively. According to management, GMD intends to accelerate the expansion of Gemalink Phases 2 and 3 to accommodate partners' expanding service routes, with Phase 3 now expected to commence operations as early as Q4/2028.

Furthermore, MBS anticipates that during 2026-2027, GMD will successfully complete a divestment at Gemalink to a new partner who is a shipping line, thereby ensuring stable cargo volumes for Phases 2 and 3. Gemalink is also in the process of seeking approval for a berth extension to connect with the adjacent SSIT terminal. This would increase the number of vessels handled simultaneously to 3-4 ships (up from 2), supporting an increase in the total capacity of all three phases to approximately 4 million TEUs. As there are no new updates on the licensing progress, MBS has not yet factored this into its forecasts.

However, if successful, this would positively impact Gemalink's net profit in 2028—estimated to rise by 14.9% above our current forecast—which would, in turn, increase GMD's 2028 net profit by 2.1%. Additionally, the container handling fee framework at deep-sea ports has been adjusted upward by 10%. Given that port service fees in Vietnam remain relatively low compared to regional peers, MBS believes GMD has significant room to raise prices in Southern Vietnam, as most terminals in the Cai Mep–Thi Vai area are already operating at or near design capacity.

Author: NGOC ANH

RECOMMENDED TOPICS