VN

VN

EN

EN

26/07/2026, 11:20

Investment

What will drive PHR’s outlook?

Higher valuation for the rubber segment and land compensation are the primary catalysts for Phuoc Hoa Rubber JSC (HSX: PHR)’s surging net profit.

In 2026, PHR targets rubber production of 13,700 tons, rubber consumption of 28,200 tons, and a maximum cost of VND 43.92 million/ton.

In 2026, PHR targets rubber production of 13,700 tons, rubber consumption of 28,200 tons, and a maximum cost of VND 43.92 million/ton. This company plans to achieve total revenue of VND 2,280 billion and net profit of VND 779 billion. PHR plans to pay a minimum cash dividend of 25% and a stock dividend at an 80% ratio from its development investment fund. Supported by land compensation, BOD expects net profit to exceed VND 2 trillion in 2026 and remain in the range of VND 1.5–2.0 trillion annually during 2027–28.

Positive outlook for the rubber segment

As of end-May 2026, rubber prices across major Southeast Asian producing markets had risen by more than 25% YTD. Thailand's STR20 reached USD 2.53/kg (29%); Indonesia's SIR20 rose to USD 2.30/kg (28%); Malaysia's SMR20 increased to USD 2.37/kg (27%); Singapore's TSR20 climbed to USD 2.28/kg (25%); while Vietnam's SVR10 reached USD 2.37/kg (26%). The rally has been driven by three key factors: supply shortages, higher oil prices, and extreme weather conditions.

First, the rubber supply is in shortage. According to the Association of Natural Rubber Producing Countries (ANRPC), global production is forecast to reach 15.32 million tons in 2026, up 2.2% yoy, while global consumption is expected to increase 1.3% yoy to 15.55 million tons. As a result, the market is projected to face a supply deficit of more than 200,000 tons. Major rubber-producing regions in Southeast Asia continue to face challenges from aging rubber trees and shrinking cultivation areas. In Thailand—the world's largest producer—the average age of rubber trees exceeds 25 years, with aging trees constituting more than half of the total stock, leading to a year-on-year decline in production capacity.

Meanwhile, rubber farmers are shifting to the cultivation of cash crops such as oil palm and fruit trees, while land conversion for IP development has further reduced cultivation areas. Given that it takes seven years for a rubber tree to mature from planting to tapping, the supply side suffers from a severe lack of elasticity.

Second, oil prices are higher. Brent oil prices increased sharply, averaging USD 88/bbl during the first five months of 2026, up 45% compared with the beginning of the year. The surge was primarily driven by geopolitical tensions in the Middle East and temporary disruptions to shipping activities through the Strait of Hormuz. Higher oil prices have provided additional support for natural rubber prices, particularly for latex products, by increasing the cost of synthetic rubber and improving the relative competitiveness of natural rubber.

Third, extreme weather conditions pose risks to rubber production. According to the latest update from the International Research Institute for Climate and Society (IRI), the probability of El Niño is expected to peak at 98% during May–July 2026 and remain exceptionally high at 97–98% through January–March 2027. By contrast, the probability of neutral conditions is estimated at only 2–3%, while the likelihood of La Niña is close to zero. El Niño typically causes prolonged heatwaves and widespread drought conditions across Southeast Asia. Such adverse weather conditions could delay tapping activities and reduce productivity.

In 2026, MBS expects Vietnam's SVR10 price to rise to USD 2.5/kg, with a full-year average of USD 2.2/kg. Accordingly, it expects PHR's average price to reach VND 57 million/ton in 2026 (14% yoy) before moderating to VND 50 million/ton in 2027 (-12% yoy), up 45% and 25% vs. the previous report. Rubber production may decline due to adverse weather conditions affecting productivity, as well as intensified competition for procurement from rubber farmers. As a result, it increased FY26-27F revenue by 27% and 17% vs. the previous report to VND 1,678 billion and VND 1,539 billion, respectively.

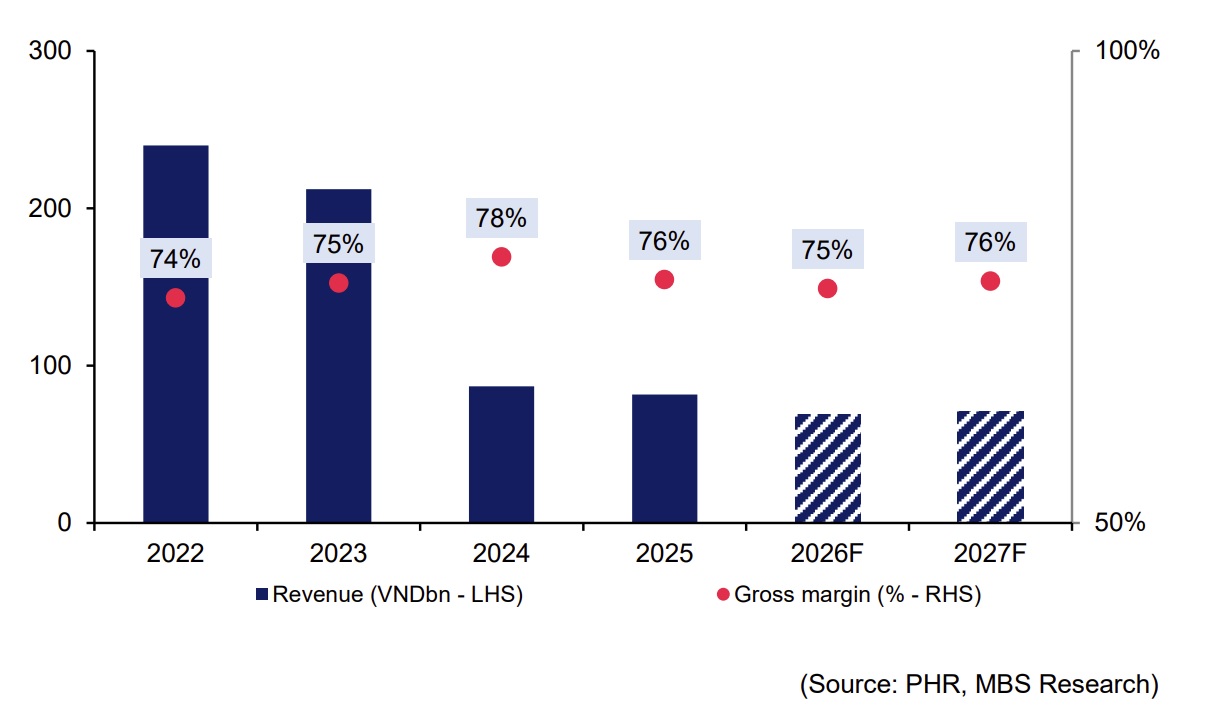

PHR's revenue

New IPs undergoing legal procedures

MBS maintained FY26-27F IP revenue, as Tan Binh IP has reached full occupancy while new IPs are undergoing legal procedures. For Tan Lap 1 IP (200 ha), the company is preparing the 1/2000 master plan and expects to complete the legal procedures by 4Q26, with construction scheduled to commence in 2027. The project is expected to target tenants in the wood processing industry.

“We expect it to generate cash flows from 2028 onward. Regarding Lai Hung IP and Bac Tan Uyen 2 IP, the company has submitted proposals to act as the developer. However, the projects have not yet received approval, so we do not incorporate them into our model," said MBS.

Leverage from land compensation

MBS increased FY26-27F other income to VND 2,089 billion and VND 1,484 billion, representing increases of 735% and 1,021% vs. the previous report, respectively, thanks to:

First, VSIP III Binh Duong IP: Instead of paying land compensation following leasing progress, VSIP will make a one-off payment to PHR. The compensation rate is VND 4.7 billion/ha for a total area of 691 ha. Total compensation amounts to VND 3,260 billion, of which approximately VND 2,103 billion remains to be received during 2026–27. The company received VND 1,050 billion in May 2026 and is expected to collect the remaining balance no later than January 31, 2027.

Second, Bac Tan Uyen 1 IP: PHR and Thaco have finalized the compensation agreement and are expected to sign it in June 2026. The compensation rate is VND 2.05 billion/ha, implying total compensation of approximately VND 1,440 billion. An advance payment of VND 500 billion is expected to be received this year.

Third, MBS forecasted that PHR would dispose rubber trees to facilitate the handover of 706 ha of land to Thaco, with a rate of VND 0.1 billion/ha. Accordingly, income from the disposal of rubber trees is estimated at VND 25 billion in 2026 and VND 46 billion in 2027.

Based on the said analysis, MBS recommended ADD for PHR and raised its target price by 41% to VND 78,200/share, thanks to higher valuation for the rubber segment and land compensation.

Author: NGOC ANH

RECOMMENDED TOPICS