VN

VN

EN

EN

15/07/2026, 10:39

Investment

Consumption rebound will drive VNM’s growth in 2025

Milk consumption is expected to show a clearer recovery in 2025. This will be considered a leverage for Viet Nam Dairy Products JSC (Vinamilk, HoSE: VNM).

In the domestic market, VNM has outperformed the entire industry thanks to its brand repositioning strategy and pioneering the development of new products. This company is leading in the plant-based milk segment, which is a potential field, while traditional segments such as fresh milk and powdered milk are slowing down. According to Data Bridge, the global plant-based milk market is expected to grow at a CAGR of 11.7% in 2023-2030 as consumers have increasingly favored low-calorie milk, which does not increase cholesterol, does not contain lactose, and is suitable for middle-aged people. Meanwhile, cow's milk is suitable for the children's segment because it is higher in calories, rich in good fats, good for bones, and easier to absorb than nut milk.

In Vietnam, plant-based milk is the fastest-growing milk line, reaching 18%/year and accounting for 12% of the dairy market share (General Statistics Office of Vietnam, GSO, 2020). Thanks to a diverse product portfolio including 12 outstanding nut milks, VNM is leading the plant-based milk market, especially with the first high-protein nut milk in Vietnam (more than 5g protein/100ml), meeting the needs of customers who play sports. KBSV expects the company to maintain a growth rate of over 10%/year in the plant-based milk segment with the aging trend in Vietnam.

According to VNM, drinking yogurt, Green Farm fresh milk, and condensed milk products maintained growth of over 10% in 9M24. KBSV believes that condensed milk, yogurt, and organic fresh milk can still maintain an average growth rate of 5-7%, offsetting the negative growth from the traditional liquid milk and powdered milk segments.

In the base scenario, KBSV forecasts a 2.5% CAGR for VNM’s domestic revenue in the period 2024-2029. GSO data showed retail sales of consumer goods and services in 9M24 might grow by a mere 8.8 YoY (lower than the level of over 10 before the pandemic) since the demand for tourism recovered by 16.7 YoY, which is not high. According to KBSV, consumer demand in 2024 is still weak due to: (1) Global economic and geopolitical instability causes people to proactively save and invest in safe assets instead of spending. (2) Rising housing prices (including rents) and essential foods affect the affordability of some people. KBSV believes that consumer sentiment is expected to be more positive in 2025 and will lag behind economic growth thanks to the 2% reduction in VAT, which should be maintained until mid-2025. Furthermore, the 2021-2025 public investment plan is in its final stages, helping economic growth.

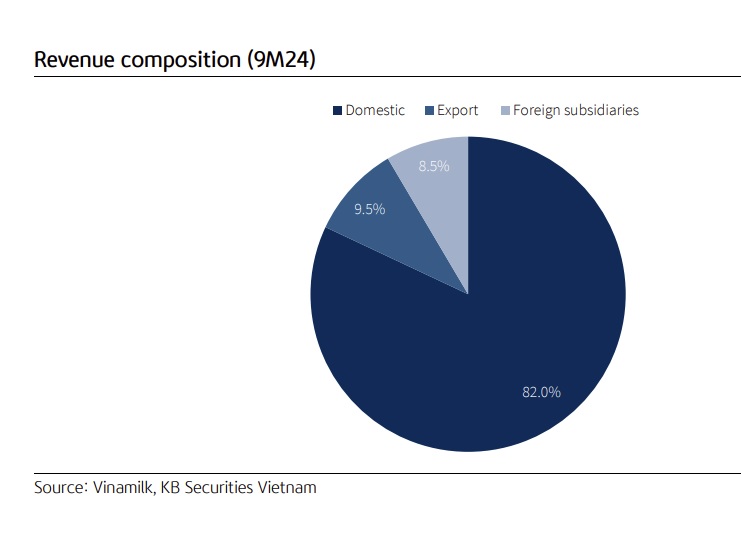

For the export markets, VNM exports to 60 countries, with Iraq being the main market (accounting for 70-80%). KBSV believes that this is a niche market with few competitors due to geopolitical instability. However, VNM has established business relationships with partners in this country since 1998 and maintained good growth momentum, showing that the risk is not too high.

According to Worldometer, Iraq has a high population growth rate, reaching 2.28%/2.15% in 2023/2024, higher than the world average and Vietnam (about 0.8%/year). Therefore, the Iraqi market has great potential for infant formula products, in addition to other traditional products. Statista said milk consumption in Iraq in the period 2018-2023 reached 5.3% and could reach 6.3% in the period 2024-2029. Based on a prudent view, KBSV forecasts export market growth at a CAGR of 5% in the base case.

According to Global Dairy Trade, skim and whole milk powder prices may be pushed up in 2025 due to (1) the strengthening of the US dollar, which is likely to increase the cost of raising cows in the EU, Australia, and New Zealand, and (2) manufacturers shifting to producing cream, reducing the supply of milk powder.

In the base case scenario, KBSV forecasts that the cost of milk powder (accounting for about 30-40% of raw material costs) will increase by 4%, but VNM’s GPM will not be affected too much because it still has a lot of room to raise product prices.

KBSV values VNM shares with an FCFF model, reflecting VNM's relatively stable and slow-growing business model. VNM is currently trading at an attractive valuation (below -1 standard deviation of its five-year average) with a projected dividend yield of 2025/current price of 6%. Therefore, it recommends BUY for VNM shares with a target price of VND75,300/share.

Author: NGOC ANH

RECOMMENDED TOPICS