VN

VN

EN

EN

09/07/2026, 11:15

Investment

Cost pressures compress DBC’s profit margins

Dabaco Group JSC (HOSE: DBC)’s 1Q26 earnings declined despite solid revenue growth due to cost pressures and weaker hog price dynamics.

DBC’s 1Q26 net profit after tax came in at VND 374 bn (-26.4% yoy), fulfilling 33.5% of the company’s full-year plan and coming in 22.9% below MBS's forecast.

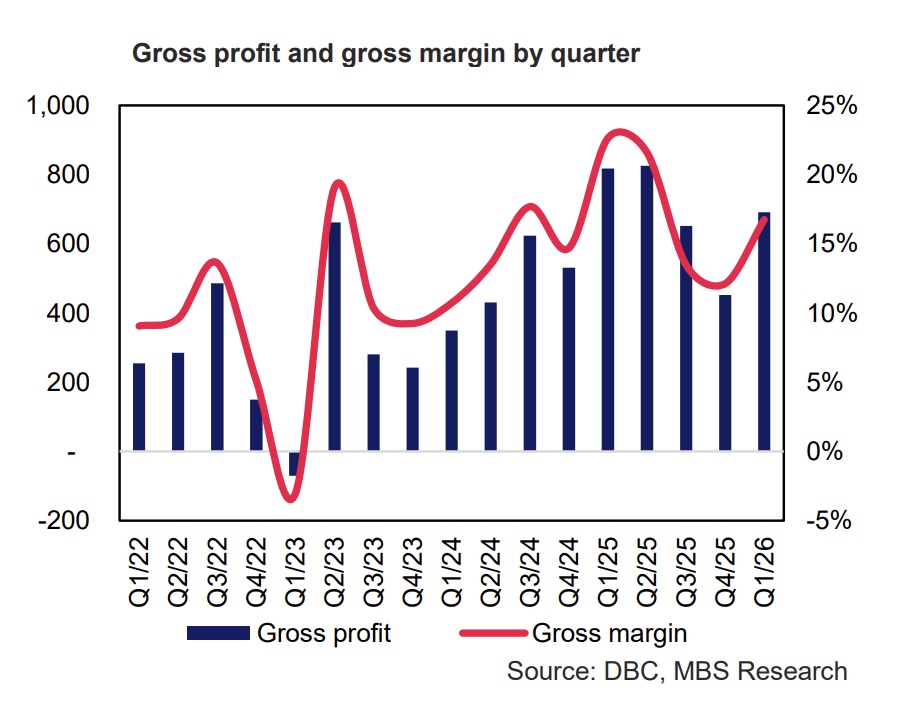

In 1Q26, DBC reported net revenue of VND 4,124 bn (14.3% yoy), supported by a 28% yoy increase in feed volumes and solid contributions from the poultry segment. Live hog prices recovered QoQ to an average of VND 69,790/kg (-2.7% yoy, 26.3% QoQ) but remained below the high base of the same period last year, leading to weaker profitability in the hog farming segment.

Meanwhile, higher input costs and FX pressures continued to weigh on feed margins. On the positive side, the poultry segment reported a profit of VND 40.2 bn (compared to a loss of VND 37.7 bn in 1Q25).

Overall, DBC’s 1Q26 net profit after tax came in at VND 374 bn (-26.4% yoy), fulfilling 33.5% of the company’s full-year plan and coming in 22.9% below MBS's forecast. Additionally, DBC commissioned Phase 2 of its vegetable oil crushing plant (capacity: 1,000 tons/day, doubling Phase 1), which is expected to support future revenue and earnings growth.

MBS forecasts DBC’s revenue to grow by 13.5% and 13.2% yoy in 2026 and 2027, respectively, driven by higher hog volumes as the company enters a new expansion phase, alongside feed selling prices adjusting upward in line with input costs. However, gross margins are expected to come under pressure over 2026-2027, as rising raw material costs coincide with an expected decline followed by a modest recovery in live hog prices. Corn and soybean prices have increased by 4% and 11.3% YTD, respectively, while average live hog prices in Q1 2026 declined 2.7% YoY.. Accordingly, MBS projects a consolidated gross margin to contract by 4.4 pp in 2026 and a further 0.2 pp in 2027. As a result, net profit is expected to decline sharply by 35.2% yoy in 2026, before rebounding by 14.7% yoy in 2027 as cost pressures gradually ease.

MBS expects DBC’s revenue to grow by 13.5%/13.2% over 2026-2027, primarily driven by (1) higher hog output as the company re-enters an expansion phase and (2) feed selling prices increasing in line with input costs. However, the outlook for live hog prices is less favorable compared to 2025, as supply recovers rapidly following ASF outbreaks and weather conditions improve (El Niño), while demand remains largely stable. This stock company forecasts average live hog prices to decline slightly to around VND 62,700/kg in 2026 (-2% yoy).

Rising input cost pressures represent the key near-term risk. Higher raw feed material prices, driven by geopolitical tensions and global supply chain disruptions, are expected to directly impact margins—particularly given DBC’s heavy reliance on imported inputs and limited ability to pass through costs. As a result, gross margin is expected to contract significantly in 2026 and remain broadly flat in 2027.

MBS applied a blended valuation approach using FCFF (WACC: 10.8%) and EV/EBITDA to derive a fair value of VND 25,500/share for DBC. For the EV/EBITDA method, it applied a target multiple of 7.x, in line with the average over 3Q21-2Q22, which is selected as a reference period given similar hog price dynamics to its 2026-2027 forecast scenario. On this basis, it recommended investors hold DBC shares with a target price of VND 25,500/share.

Author: NGOC ANH

RECOMMENDED TOPICS