VN

VN

EN

EN

09/07/2026, 02:38

Investment

Could interest rates have approached their peak?

The overnight interbank lending rate has temporarily dropped back to around 6%/year — a comfort zone compared to the previous peak of nearly 13%.

Interbank Interest Rates Cool Down

On the open market, during the trading session on July 7, the State Bank of Vietnam (SBV) offered 1,000 billion VND for a 7-day term, 2,000 billion VND for a 35-day term, and 2,000 billion VND for a 63-day term through the mortgage channel (OMO). The total bidding value of 5,000 billion VND was fully won, all at an interest rate of 4.5%/year. Nearly 20,964 billion VND matured in this session. The SBV continued to refrain from issuing central bank bills. Consequently, the SBV net-withdrew 15,964 billion VND from the market. The outstanding volume on the mortgage channel after this session stood at around 219,055 billion VND.

(Source: SBV)

Previously, in the July 6 session, continuing open market operations, the SBV offered 3,000 billion VND each for 7-day and 63-day terms, and 1,000 billion VND for a 35-day term, all at a 4.5% interest rate. There were 2,636.67 billion VND won for the 7-day term, 780.34 billion VND for the 35-day term, and 3,000 billion VND for the 63-day term. Meanwhile, 10,597.08 billion VND matured. The SBV did not offer any central bank bills. Accordingly, in the preceding session, the SBV net-withdrew 4,180.07 billion VND from the market through open market operations. The outstanding volume circulating on the mortgage channel was 235,019.31 billion VND.

Thus, for two consecutive sessions at the beginning of the week, the SBV maintained a net withdrawal — a reversal from the trend seen during the turn of the month from June 29 to July 3. Specifically, during that week, the SBV continued to inject liquidity slightly via the OMO channel after a modest injection the week before. The SBV issued 69.1 trillion VND while the maturing volume reached 59.5 trillion VND, thereby net-injecting about 9.5 trillion VND into the system. Although the injection amount was small, it showed that the SBV actively supported liquidity during the sensitive end-of-quarter period.

In addition, the swap tool (spot USD buy - forward USD sell) was also utilized by the SBV on June 29 to inject VND into the system without putting pressure on the exchange rate.

Accordingly, in the week of June 29 – July 3, the interbank interest rate spiked to approximately 13% in one session before being adjusted downward as previously reported by Dien Dan Doanh Nghiep. This indicates that very short-term capital pressure could still appear locally, but the need to balance capital across the end of the quarter has eased compared to previous weeks.

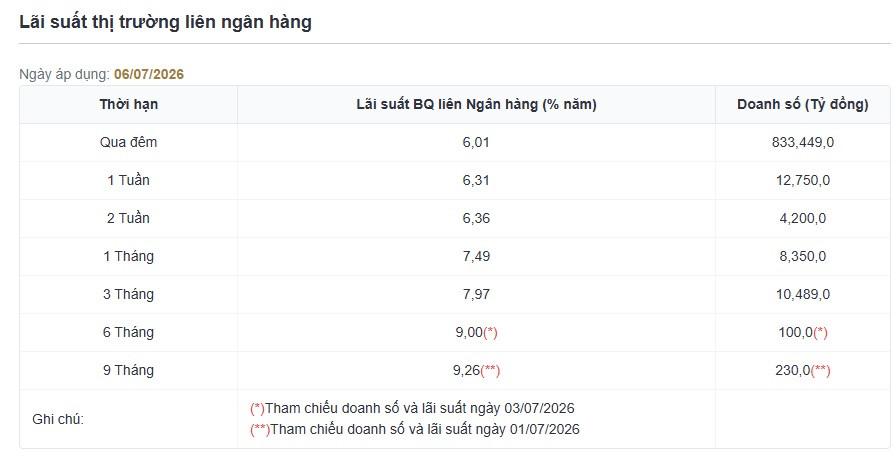

By the July 6 session, data from the SBV recorded that the average VND interbank interest rate increased by 0.2–0.3 percentage points for overnight and 1-week terms, while decreasing by 0.05–0.15 percentage points for 2-week and 1-month terms compared to the final session of the previous week. Transactions stood at: overnight 6%; 1 week 6.4%; 2 weeks 6.6%; and 1 month 7.45%. The average USD interbank interest rate remained unchanged for short terms while increasing by 0.02 percentage points for the 1-month term; trading at: overnight 3.66%; 1 week 3.7%; 2 weeks 3.75%, and 1 month 3.81%.

Government bond yields on the secondary market remained unchanged across most maturities, except for a slight increase in the 10-year term, closing the session at: 3-year 3.57%; 5-year 4.20%; 7-year 4.26%; 10-year 4.40%; and 15-year 4.57%.

Prior to that, in the July 5 session, the average overnight interbank interest rate was anchored at 5.7%.

It can be said that, apart from the temporary surge in liquidity pressure caused by short-term end-of-quarter demands, the banking system is absorbing the SBV's recent liquidity support measures, which has helped alleviate some of the stress in the money market.

Data recently released by the SBV shows that credit growth and capital mobilization in the first 6 months of 2026 reached 7.41% and 5.05% respectively. Notably, deposit mobilization improved significantly compared to the 2.98% recorded at the end of the first 5 months, according to an assessment by Yuanta Securities Vietnam, contributing to narrowing the gap with credit growth. However, the gap between credit growth and capital mobilization remains high, indicating that the pressure on medium-to-long-term capital sources has not been fully resolved.

Banks Mobilizing Capital on Market 1

On Market 1 (the retail market between banks and customers), although listed deposit rates saw little volatility, many banks are raising interest rates through promotional programs and tailored agreements—pushing rates up to 9.2% - 9.3%—and issuing bonds with yields up to 9.7%/year. This demonstrates that the need to replenish medium-to-long-term capital is still present, especially amid the current push to expand credit.

Interest rates are believed to have approached their peak and are gradually cooling down. (Illustrative photo: Quoc Tuan)

Market observations show that many banks have designed highly diverse interest rate incentives. For instance, PVcomBank is leading with an interest rate of 10%/year for 12-to-13-month terms with interest paid at maturity, applicable exclusively to deposits of 2,000 billion VND or more. At MSB, a 9%/year interest rate applies to savings books opened new or automatically renewed from January 1, 2018, with a minimum balance of 500 billion VND for 12 or 13-month terms.

Vikki Bank has a policy of adding an extra 1.8%/year for customers depositing 999 billion VND or more. This rate is calculated by adding a 1.8 percentage point margin to the listed interest rate and cannot be applied simultaneously with other promotional programs. This lender is paying interest rates up to 7.9%/year for VIP customers, alongside various incentives to win SJC gold for customers who download the app and open a VikkiME account.

Meanwhile, at HDBank, customers depositing 500 billion VND or more are eligible for two special interest rates for 12 and 13-month terms, at 7.2%/year and 7.6%/year respectively (compared to the regular listed rates of 5.2%/year and 5.4%/year).

In general, the group of banks designing special interest rate programs—such as PVComBank, Nam A Bank, ACB, MSB, Vikki Bank, ABBank, LPBank, VietBank, HDBank, OCB, etc.—are all targeting large deposits from major institutional or high-net-worth clients. However, added gifts or entry into lucky draw programs also offer strong appeal to retail customers looking to deposit smaller, short-term amounts.

Aside from these special interest rate programs for substantial deposits, standard deposit interest rates on Market 1 are showing relative stability.

The group of banks applying online deposit rates of over 7.5%/year depending on the term includes ACB, SaigonBank, VIB, MB, VCBNeo, and PGBank.

BVBank, Bac A Bank, OCB, and LPBank are applying an interest rate of 6.9%/year for 12-month deposits.

BIDV, Vietcombank, VietinBank, and Agribank maintain uniform interest rates across terms at the lowest levels in the market: 4.75%/year; 6.6%/year for 6-month and 9-month terms; while 12-month and 18-month terms are both listed at 6.8%/year.

TPBank, ABBank, Techcombank, BaoVietBank, NamABank, MB, SHB, and NCB list online deposit rates ranging from 6.25% to 6.75%/year for a 12-month term.

Finally, VietA Bank, VietBank, and Vikki Bank all apply a rate of 6.1%/year, while PVcomBank, GPBank, KienlongBank, Eximbank, HDBank, and SeABank are in the group applying interest rates from 6.2%/year. SCB remains the bank with the lowest listed deposit rates in the system, starting from 3.7%/year for a 12-month term. Note that these are online savings rates listed on the respective banks' websites/apps.

Yuanta Securities Vietnam believes that in the short term, seasonal pressures from the end of the quarter have passed, and interbank interest rates are highly likely to remain stable around the newly established range (around 5.7%-6% for the overnight term, as mentioned).

Accordingly, analysts from the Retail Research & Analysis Division at YSVN also suggest that overall interest rates may have neared their peak thanks to the regulatory orientation of the central bank. However, close monitoring of liquidity developments and capital mobilization growth remains essential moving forward.

Author: LE MY - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS