VN

VN

EN

EN

09/07/2026, 02:00

Business economics

High interest rates to continue weighing on banks' asset quality risks

Experts forecast that persistently high interest rates, coupled with rising household leverage, will increase the risk of deterioration in banks’ asset quality.

Vietnamese banks entered 2026 amid a more challenging and volatile operating environment, as interest rates remain elevated due to system-wide liquidity pressures and external headwinds that are weakening both asset quality and profitability.

United Overseas Bank (UOB) expects the State Bank of Vietnam (SBV) to keep the refinancing rate unchanged at 4.50% per year and the rediscount rate at 3.00% per year. In the coming period, prolonged high interest rates and rising household leverage are expected to increase the risk of weakening asset quality.

Interest rates remain elevated due to system-wide liquidity pressures and external headwinds that are weakening both asset quality and profitability.

Asset Quality Weakens at Smaller Banks

Assessing banks’ credit profiles during the first quarter of 2026 amid macroeconomic uncertainty and market volatility, experts from VIS Rating said mid-sized banks recorded the sharpest deterioration in credit profiles. This was driven by rising overdue loans in the retail customer segment, while return on average assets (ROAA) declined as net interest margins (NIM) narrowed and credit costs increased.

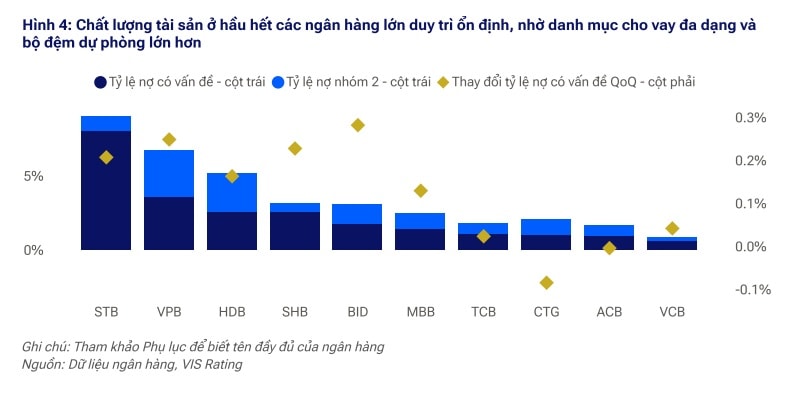

By contrast, large banks and state-owned banks (SOBs) generally maintained stable asset quality and profitability thanks to diversified loan portfolios, stronger customer bases, and stable fee income streams.

Specifically, non-performing loans in the retail segment increased at smaller banks as high interest rates and elevated leverage persisted. The sector’s problem loan ratio rose by 11 basis points quarter-on-quarter to 2.2% in the first quarter of 2026, reflecting higher new bad debt formation.

The deterioration in asset quality was concentrated among small and mid-sized banks such as LPB, OCB, TPB, PGB, BAB, SGB, and VBB, mainly due to rising overdue loans related to home purchases, household businesses, and unsecured consumer lending, alongside an approximately 10 percentage-point decline in bad debt coverage ratios.

Meanwhile, larger banks, including both state-owned and private lenders such as VCB, CTG, ACB, and TCB, maintained relatively stable asset quality due to diversified lending portfolios, stronger customer foundations, and larger provisioning buffers.

Interest Rates Pressure Debt Repayment Capacity

VIS Rating forecasts that persistently high interest rates and rising household leverage will continue to increase the risk of asset quality deterioration, especially for banks with high exposure to retail lending and limited risk buffers.

Nguyễn Hà My, CFA, Head of Analysis at VIS Rating, said the bad debt formation ratio is expected to rise further in 2026, particularly among smaller banks with significant retail lending exposure, as elevated interest rates and growing household leverage continue to weigh on borrowers’ repayment capacity.

Shrinking profit margins due to heightened competition for deposits have also reduced profitability, with the impact most severe on small and mid-sized banks. Sector-wide ROAA fell by 10 basis points quarter-on-quarter to 1.4% in the first quarter of 2026, while NIM contracted by an average of 11 basis points because of rising funding costs, especially among smaller banks with more limited deposit mobilization networks.

Mid-sized banks also faced pressure from rising credit costs, declining non-interest income, and the absence of extraordinary income sources.

Large banks, however, maintained broadly stable profitability, supported by improving NIMs, recovering bancassurance income, lower credit costs, and tighter expense control.

“We expect narrowing NIMs and rising credit costs to reduce core profitability for small and mid-sized banks in 2026, amid continued funding competition and sustained pressure from asset quality risks,” analysts said.

Deposit Competition Pressures Profitability

One notable bright spot identified by experts is the upcoming wave of capital increases, which is expected to strengthen capital buffers, although trends will diverge across banking groups. The sector’s tangible common equity to total assets (TCE/TA) ratio rose by 20 basis points quarter-on-quarter to 8.4% in the first quarter of 2026, driven by large-scale capital raisings at banks such as BID, PGB, and BAB.

New capital raising plans in 2026 are expected to further strengthen capital buffers at smaller banks such as ABB, NVB, VAB, and BVB, while supporting stronger growth at larger banks including HDB and VPB.

However, capital adequacy ratios at mid-sized banks could weaken due to lower internal capital generation capacity and cash dividend payments, as seen at LPB and VIB.

Tighter system liquidity and funding constraints are expected to keep deposit costs elevated in the short term. The sector’s CASA-to-loan ratio declined by 2 percentage points quarter-on-quarter to 18% in the first quarter of 2026, reflecting deposit outflows from both retail customers and corporate clients.

According to VIS Rating, funding conditions remain tight, with total system deposit growth reaching only 0.6%, while nearly half of all banks surveyed (12 out of 27) recorded deposit declines. This included both large banks such as BID, MBB, TCB, and ACB and smaller lenders such as TPB, SGB, and VBB, highlighting system-wide competition for deposits and increasing reliance on short-term interbank funding.

Although tighter liquidity regulations, including CDR, LCR, NSFR, and leverage ratio requirements, are expected to have positive long-term effects, in the short term they will intensify competition for deposits, keep funding costs elevated, and pressure profitability, especially for banks that rely heavily on market-based funding sources.

Author: LE MY - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS