VN

VN

EN

EN

16/07/2026, 02:00

Business economics

USD/VND exchange rate continues cooling trend

Since the beginning of 2026, the VND has remained stable despite a strengthening DXY and an increasing trade deficit.

In the opening trading session of this week, May 11, the central exchange rate announced by the State Bank of Vietnam stood at 25,118 VND, an increase of 6 VND. Meanwhile, the free market USD rate decreased by 30 VND, falling to 26,420 – 26,470 VND/USD. The USD-Index was at 97.87, amid signs of cooling tensions in the Middle East.

The official USD/VND exchange rate recorded stability while the rate on the informal market decreased. (Illustration photo)

USD/VND Exchange Rate Remains Stable and Moves Sideways

Previously, statistical data recorded that during the week of May 4–8, the USD index decreased slightly by 0.08% WoW to 98.23 points, despite significant volatility during the week. According to Yuanta Securities Vietnam, the USD faced pressure as the market continued to hope for a de-escalation of U.S.-Iran tensions, while gold and several risky currencies recovered. The DXY at one point dropped to its lowest level since late February but was still somewhat supported by better-than-expected U.S. employment data for April and the possibility that the Fed might maintain high interest rates for longer.

Also last week, the JPY continued to be the focus of the global FX market as the USD/JPY exchange rate fluctuated sharply around the 156–160 range. After intervening in late April, the Japanese Ministry of Finance is believed to have continued purchasing Yen last week, helping the currency see sudden strong gains in some sessions. Additionally, expectations that the BoJ might raise interest rates further in June supported the JPY, although the market still believes the BoJ's policy normalization process will be slow. Meanwhile, the EUR and GBP were relatively stable and tended to strengthen against the USD due to expectations that the ECB and BoE will maintain relatively cautious policy stances due to energy inflation risks.

Note that global JPY fluctuations are always a concern for investors, as capital flows frequently rotate between the JPY and USD based on the interest rate differential between the U.S. Federal Reserve (Fed) and the BoJ, amplifying volatility for both the DXY and USD/JPY.

Interest rate differentials are the basis for the strategy known as the "Yen carry trade." Accordingly, when BoJ rates are low while the Fed maintains a high range (the current gap is up to 300 basis points), investors borrow Yen at a cheap cost and then invest that capital into higher-yielding assets in USD or other strong currencies to profit from the spread. When the JPY appreciates or the BoJ changes policy (raises rates), this strategy is abruptly reversed as many investors close their positions to repay loans before the JPY price or interest rates rise too high. The Yen carry trade is so prevalent that if a wave of exits from this activity occurs, widespread impact on global markets—including assets and the greenback—is inevitable. This also has cross-impacts on efforts to stabilize the USD/VND exchange rate.

According to data from May 4–8, domestic official exchange rates generally remained stable. The central rate ended the week at 25,112 VND/USD, flat compared to the previous week; buying/selling rates at commercial banks were 26,087/26,367 VND/USD, respectively, decreasing slightly on the buying side and remaining unchanged on the selling side. Notably, the free market rate dropped sharply by 1.08% WoW to 26,450 VND/USD, extending the cooling trend after a period of strong volatility in late March. Exchange rate pressure on the free market has eased significantly as the DXY adjusted and the domestic-global gold price gap narrowed to approximately 4.3 million VND/tael.

Mr. Truong Quang Binh, Director of Retail Research and Analysis at Yuanta Securities Vietnam, observed that in the short term, the USD/VND exchange rate is likely to continue moving sideways within a narrow range, despite the possibility of a USD recovery this week.

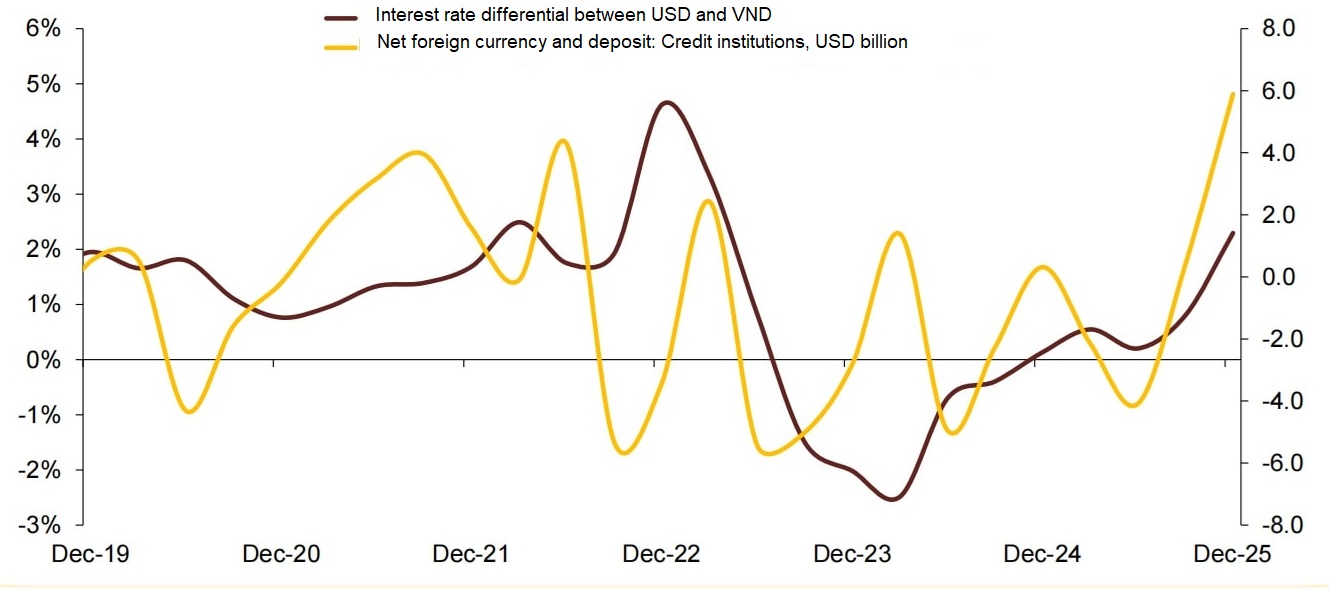

VND-USD Interest Rate Differential and Trade Balance

From a macro perspective, Mr. Vu Viet Linh, Deputy Director of Institutional Client Analysis at Maybank Securities, analyzed that Vietnam's balance of payments changed significantly in the second half of 2025, recording a surplus of 2.4 billion USD in Q4/2025. Besides support from the trade balance and FDI, the main driver came from the reversal of the "other investment" category, shifting from a deficit of 9.4 billion USD mid-year to a surplus of 1.1 billion USD by the end of 2025.

This reversal was driven by the widening VND-USD interest rate differential, which reached 2.3% in Q4/2025. This gap boosted foreign currency deposit flows into credit institutions, increasing to nearly 6.0 billion USD in Q4/2025 (compared to -4.1 billion USD in Q2/2025), Mr. Linh noted.

However, according to the Maybank expert, structural weaknesses still exist. The errors and omissions category continued to show a heavy negative at -12.4 billion USD in Q4/2025, reflecting continued foreign currency outflows from the individual and non-banking sectors (-4.1 billion USD in Q4/2025).

"This shows that domestic confidence in the VND remains weak, even though credit institutions have responded with higher VND interest rates," according to Mr. Linh.

From the beginning of 2026 to date, the VND has remained stable despite the strengthening DXY and increasing trade deficit, likely thanks to capital flows into the balance of payments continuing to be supported by the other investment category. Current stability depends less on the trade balance and more on the State Bank of Vietnam's (SBV) determination to maintain a high VND-USD interest rate differential—thereby anchoring institutional liquidity while private sector confidence gradually recovers.

Author: LE MY - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS