VN

VN

EN

EN

26/07/2026, 02:38

Business economics

What challenges is the UK facing?

The UK is not alone in suffering supply-chain difficulties, but it is in the worst position than many, and part of this is down to Brexit.

The pound gained a modestly bullish bias. Given that it has risen by around 5% in trade-weighted terms over the past year, this appears a reasonable view. However, it has started to wobble a bit recently.

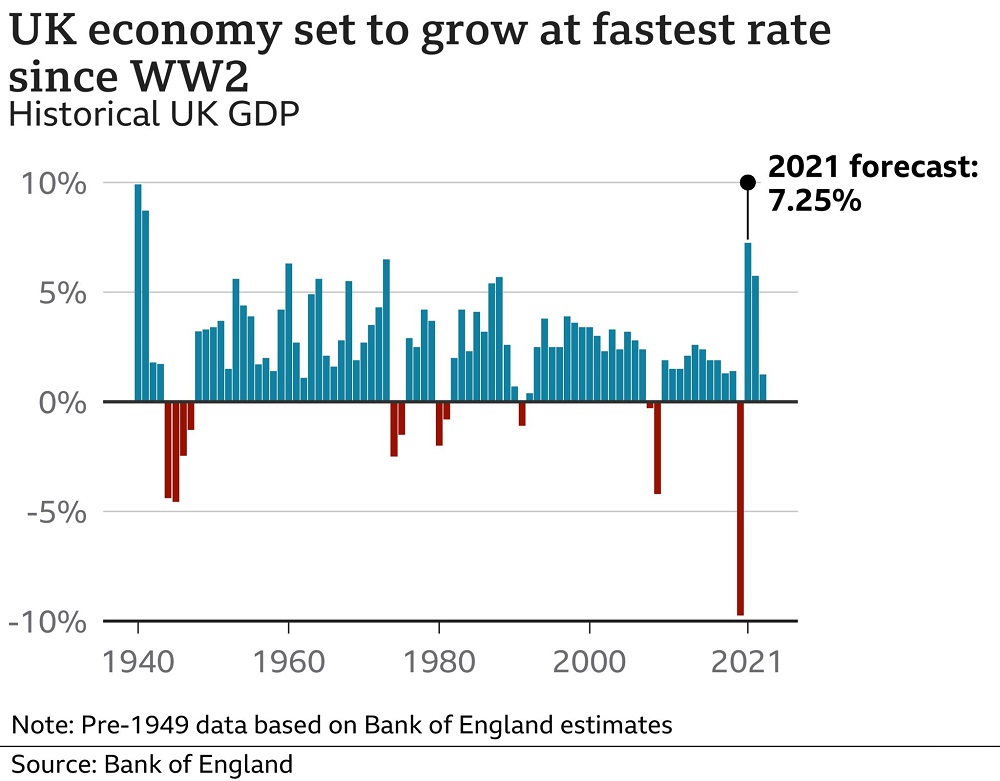

Last week, Bank of England Governor Bailey talked about all the bad things that have befallen the UK economy recently. It certainly seems like this given the images of petrol queues, empty supermarket shelves and fears that Christmas could be canceled because of supply-side problems. The UK is not alone in suffering supply-chain difficulties, but it is in the worst position than many, and part of this is down to Brexit. Perhaps fortunately for the government, Covid-induced supply chain problems are so massive that they cover up the tensions created by Brexit. And don’t forget, Brexit only started in earnest this year, at least when it comes to trade, not in 2016 when the referendum to leave the EU saw UK residents vote for the exit. What’s more, the full extent of Brexit is yet to arrive, not just with respect to trade but also other sectors of the economy as well. If things are this bad under this smoothed-in Brexit, just imagine how hard things could get when full Brexit arrives.

One problem is that the Brexit process appears to have increased distrust in the government and that can create havoc when shortages are muted because government denials are ignored, as we have seen with the petrol crisis. It is not inconceivable that more such shortages could develop, particularly as the government’s argument to things like the shortage of skilled UK workers is not to allow EU citizens back but, instead, train up more of the UK workforce.

Of course, the government denies that Brexit is playing a part in the difficulties and even the Bank of England hides behind the argument that it is just too hard to distinguish the impact of Brexit from that of Covid. But even a cursory glance at trade data between the UK and EU shows concerning signs, while non-EU trade looks solid. For instance, before Brexit – and before Covid – imports of goods from non-EU countries were running around 20% below those from the EU. But since Brexit, the UK now imports more goods from outside the EU than inside. What’s more, the main difficulty, which involves trade between Great Britain and Northern Ireland, is still the cause of a huge row between the UK and EU and could still end up with the UK unilaterally reneging on the NI protocol and being taken to court by the EU.

Mr. Steve Barrow, Head of Standard Bank G10 Strategy thinks it is pretty clear that Brexit has been a huge spanner in the works for the UK economy, even if it is not easy to see its effects because the – even bigger – spanner of Covid has been thrown in as well. For the markets, and the pound specifically, the question is whether this constitutes a sufficient problem to unwind the strength that we have seen in the pound. Before the 2016 EU referendum, the euro/sterling was in a rough 0.75-0.80 trading range. Since the referendum, the 0.83-0.93 level has captured most of the activity. In other words, there has been a step down in sterling which likely captures the perceived cost of Brexit to the UK.

“Sterling has been clawing its way back over the past year, or so, but we now reach a point where we might need to ask if the market has sufficiently discounted all the bad news that Brexit brings. For the moment, we still stick with the view that sufficient bad news has been priced into the pound and that, as we go forward, and especially as some of the current acute problems ease, the pound will more likely move towards 0.80 than 0.90 against the euro. But we do feel as if we are clinging onto this view with an increasingly tenuous grip”, Mr. Steve Barrow said.

Author: NGOC ANH

RECOMMENDED TOPICS