VN

VN

EN

EN

26/07/2026, 02:00

Investment

Does BCM stock have room to rise further?

The BCM stock of Becamex Investment and Industrial Development Group is currently trading at a trailing P/B of 2.5x and a forward P/B of 2.1x, both below the 5-year historical average P/B of 3.9x.

MBS believes BCM’s profits are entering an acceleration phase, generating cash flows to support large-scale investments, particularly as its planned capital raising has yet to be implemented.

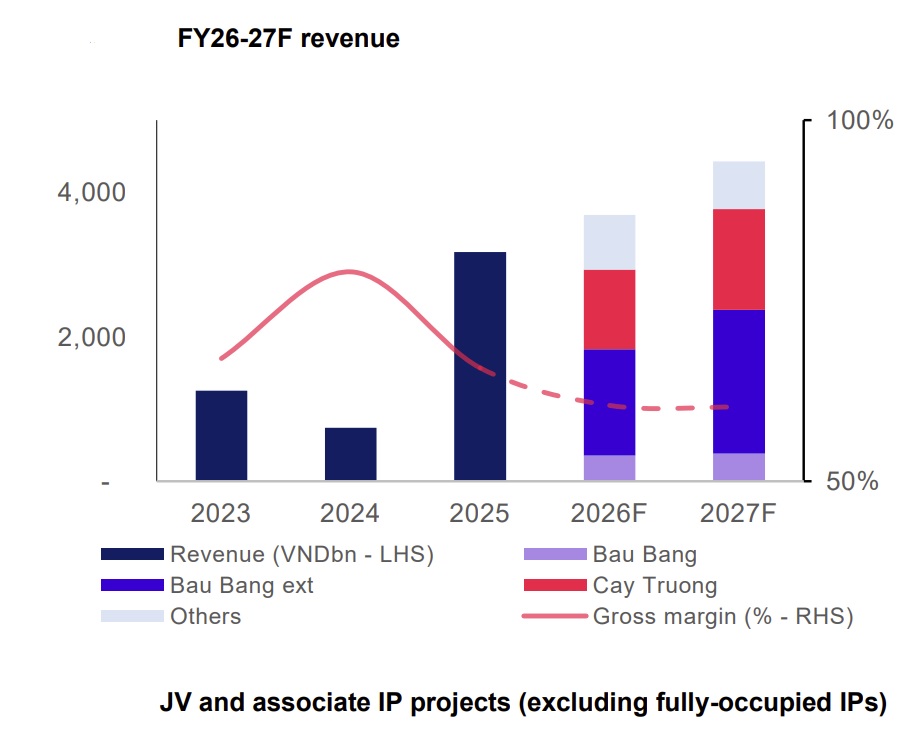

Policy reforms in attracting both domestic and foreign investment into the high-tech sector are laying the foundation for a structural transformation of the IP industry, shifting from traditional IPs toward eco-industrial and high-tech IPs. BCM is developing smart eco-IPs, beginning with Bau Bang IP (phase 2–380 ha) and Cay Truong IP (700 ha), while gradually transforming old IPs toward automation and sustainability. In parallel, BCM and VSIP are jointly investing in new-generation IPs, with new IPs in HCMC, Khanh Hoa, Tay Ninh, Lam Dong, and Binh Phuoc, providing meaningful growth in the coming years.

Following the administrative merger, the former Binh Duong is expected to become a key destination for real estate investment flows, supported by a series of transport infrastructure projects, including the expansion of National Highway 13, the HCMC–Thu Dau Mot–Chon Thanh expressway, and Ring Road 4 of HCMC (the section passing through the former Binh Duong). The development of Science Technology City is expected to attract a high-quality workforce with genuine housing demand around IPs, while investment capital is likely to shift from the city core of HCMC as the city undergoes urban restructuring and spatial re-planning.

MBS believes BCM’s profits are entering an acceleration phase, generating cash flows to support large-scale investments, particularly as its planned capital raising has yet to be implemented. With a large land bank, land prices in the former Binh Duong continue to appreciate, while BCM’s stock price remains deeply discounted relative to its asset valuation. The BCM stock is currently trading at a trailing P/B of 2.5x and a forward P/B of 2.1x, both below the 5-year historical average P/B of 3.9x. MBS believes this presents an attractive opportunity to accumulate BCM shares. However, BCM has faced some downside risks.

First, risks from the U.S. initiating investigations under Section 301 of the U.S. Trade Act of 1974, which may lead to broad-based tariff increases, while such investigations could be used as a bargaining tool in trade negotiations.

Second, there are risks of weaker leasing demand as rising costs may adversely affect tenants’ investment plans.

Third, liquidity risk stems from an increasing debt burden, with significant debt repayment due in 2026 and 2028, particularly in the context of rising interest rates.

Fourth, risk of higher land clearance costs has emerged following the implementation of the amended Land Law in 2025, as compensation costs are based on market prices.

That being said, MBS raised its target price for BCM to VND 89,600/share, driven by (1) a 20% increase in the valuation of the residential property segment, supported by rising land prices after the merger and new land bank; and (2) a 25% increase in VSIP’s valuation, attributable to the approval of new IPs, including VSIP Nam Dinh, VSIP Nghe An III, VSIP Ninh Xuan, and VSIP Hue, with a total land area of over 1,300 ha.

Author: NGOC ANH

RECOMMENDED TOPICS