VN

VN

EN

EN

25/06/2026, 02:38

Investment

HAH leverages its core business

Hai An Transport and Stevedoring JSC (HoSE: HAH) has raised its investment in its core business in order to generate growth leverage.

At the end of 1Q26, HAH reported net revenue of VND 1,264 billion, up 8% from the same time in 2025, and after-tax profit of VND 350 billion, up more than 28%

However, this move raises various obstacles for HAH, such as the need to repay principal and interest...

What to boost net profit

At the end of 1Q26, HAH reported net revenue of VND 1,264 billion, up 8% from the same time in 2025, and after-tax profit of VND 350 billion, up more than 28% from the same period the previous year. Despite the volatility of the global transportation sector, HAH's profit growth rate is rather strong. Shipping operations are the primary sources of HAH's significant revenue and profit.

Furthermore, the management and reduction of operational expenses directly contributed to HAH's development in the first quarter of this year.

With its strong economic momentum and considerable financial resources, HAH may seek to increase capacity and extend its fleet of transport boats on intra-Asian shipping routes.

HAH's shareholding structure has shifted to support its expansion plans. As of March 31, 2026, HAH had two significant owners: Vietnam Container Corporation (VSC), which held 16.07% of the charter capital, and Hai Ha Investment and Transport Corporation, which held 14.29% of the charter capital. The remaining 69.64% of the charter capital was held by shareholders who owned less than 5%.

Fleet expansion

The HAH leadership approved investment and fleet growth plans of roughly VND 13,500 billion, as evidenced by Board of Directors resolutions. Most recently, HAH collaborated with Viconship to build and manage a fleet of container ships with capacities ranging from 3,000 to 7,000 TEU. This deal represents a new phase in HAH's fleet growth plan to increase marine transport capacity and create more international shipping routes.

The joint venture plans to build five additional container ships, comprising two 7,000 TEU boats and three 3,000 TEU vessels. This action comes after the Hai An Green Shipping Lines joint venture inked a contract for the building of two 7,100 TEU container ships by the end of 2025. Overall, the joint venture's fleet expansion strategy is for a fleet of nine ships in the following years, with seven new and two secondhand container ships.

Furthermore, purchasing used vessels is a rapid option to boost operating capacity while waiting for the completion and delivery of new ones. Intra-Asian and international transshipment routes often utilise new medium- and big container ships, with capacities ranging from 3,000 to 7,000 TEU. A big and diversified fleet will allow HAH and its partner ventures to reduce operating costs and increase transportation efficiency. For many years, HAH has strived to develop its core business.

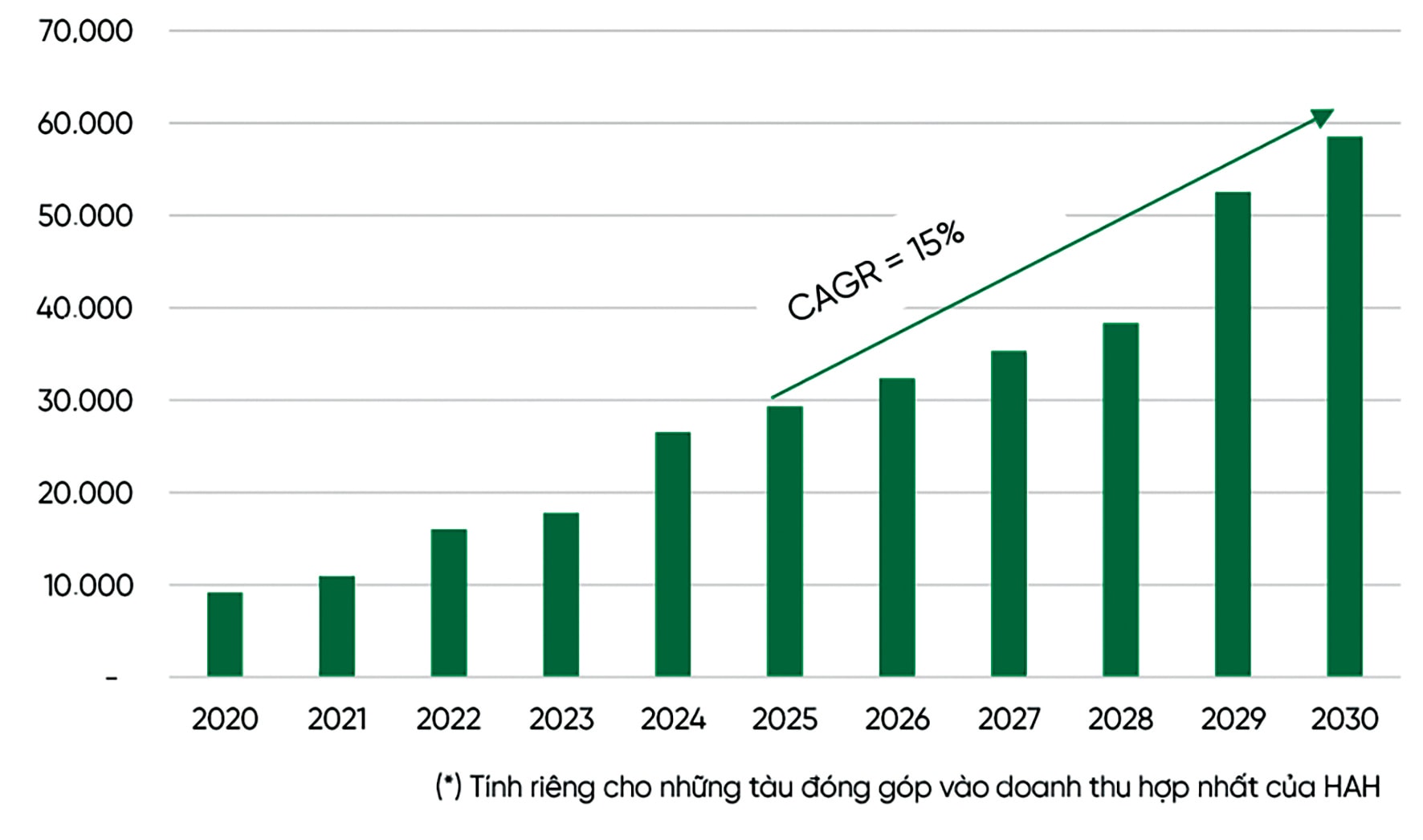

HAH's projected fleet capacity in the period 2026 - 2030. Source: HAH, VPBankS Research.

According to Phu Hung Securities Company projections, the majority of the boats in HAH's plan will be delivered between 2027 and 2030, bringing the total number of HAH vessels to around 22 by the end of 2028, or nearly 1.2 times the fleet size at the end of 2025. The bulk of vessels supplied during this time are projected to be small container ships with a capacity of less than 4,000 TEU, which is a key sector in HAH's intra-Asia container shipping network.

Challenges in expanding its operations

Regarding HAH's business prospects, Yuanta Vietnam anticipates that these newly built vessels will be used at full capacity due to the ongoing rise of intra-Asian commerce. Currently, HAH's intra-Asia container traffic ranks second among important global commerce routes, trailing only the Asia-North America route.

As a result, the new vessels delivered this year and in 2027-2028 will be available for lease at premium prices. Thus, HAH's growth momentum in 2026-2028 will be primarily driven by the contribution of the new fleet, allowing HAH's revenue and after-tax profit to possibly expand by 14-23% each year.

Many financial analysts believe that while HAH's fleet expansion investment has the potential to increase revenue, it also entails the danger of large debt. VPS predicts that HAH's financial leverage ratio might peak in 2027-2028, corresponding with the delivery of the majority of its new vessels between 2026 and 2030. However, given the positive growth prospects of its transportation operations and its prudent capital management strategy, HAH's debt-to-total assets ratio is expected to remain in the 30-35% range, while its interest coverage ratio (EBIT/interest expense) will remain high, reducing financial risks during the expansion investment cycle.

Furthermore, the slowdown in global trade tensions caused by the Middle East war will have a detrimental influence on the shipping operations of container shipping firms in general, as well as HAH specifically.

Furthermore, freight rates may revert to normal levels earlier than predicted in 2027, which means HAH may no longer profit from price rises. BIMCO predicts that global transport supply and demand will be about balanced in 2026, with supply growing at 3% and demand varying between 2.5% and 3.5%. In 2027, supply is predicted to expand faster (3.5%) than demand (2.5-3.5%), resulting in a minor deterioration in the transport market balance. In this scenario, the supply-demand mismatch is expected to reverse, placing downward pressure on transport rates in the medium term.

Author: NGOC ANH

RECOMMENDED TOPICS