VN

VN

EN

EN

15/07/2026, 10:39

Investment

How the Middle East conflict impacts Vietnam stock market sectors

In the short term, the Vietnamese stock market will also be negatively affected by the downtrend of global stock markets.

Binh Son Refinery – BSR may benefit from a more favorable business environment.

KBSV believes that the escalating conflict in the Middle East will not directly impact Vietnam's economy because the proportion of exports, imports, and FDI from these two countries is quite small. Vietnam's total import and export turnover with Israel is around USD3 billion in the last two years (corresponding to about 0.4% of Vietnam's total turnover), while the turnover with Iran is very small and lack of statistical data. Furthermore, the proportion of FDI from both countries in Vietnam is less than 0.1%.

However, indirect impacts from cost-push inflation risks due to energy price pressure and transportation costs should be considered. At the same time, geopolitical instability may prompt investors to seek safe-haven assets (gold & USD) if the DXY rises again in the near term, weighing on the exchange rate.

In the short term, the Vietnamese stock market will also be negatively affected by the downtrend of global stock markets. However, in the medium term, KBSV said, the extent of the impact on the market would depend on whether the two sides can soon sit down at the negotiating table and find common ground. If the conflict continues, escalating tensions will disrupt supply chains, especially crude oil, potentially affecting inflation and exchange rates (similar to the situation in 2022 with the Russia-Ukraine conflict). Emerging stock markets, including Vietnam, may face protracted downward pressure.

In KBSV’s view, the Middle East conflict could impact market sectors as follows:

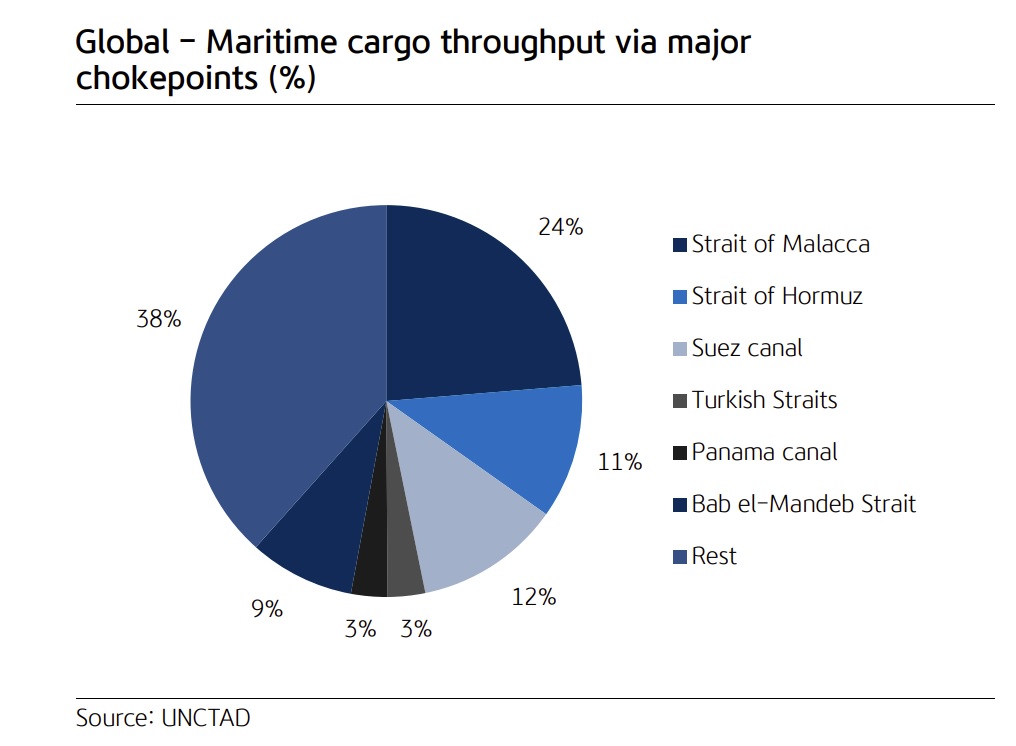

First, as international shipping distances and times are extended, the demand for chartering will increase, pushing charter rates up and creating opportunities for shipping lines to benefit from better freight rates. Shipping companies (like PVT, HAH, and VOS) are expected to raise charter rates for floating-rate and term contracts after renegotiation.

Second, disruptions in the global petroleum supply chain will increase the demand for refinery operations, thereby increasing the crack spread in the short term. In this context, Binh Son Refinery – BSR may benefit from a more favorable business environment. On the other hand, rising and sustainably high oil prices are often accompanied by improved profit margins for oil refiners due to reduced provisions for inventory devaluation.

Third, POW currently owns the Nhon Trach 3&4 power plants, which rely entirely on imported LNG and will therefore be subject to disruptions in petroleum supply. However, thanks to its diversified power generation (hydroelectric, coal-fired, and gas-fired), the company can minimize the impact on its business results. For power generation companies using coal and water as input fuels, the impact from gas shortages is negligible.

Fourth, urea fertilizer producers such as DPM and DCM often benefit during Middle East fertilizer supply disruptions. Natural gas accounts for 70-80% of fertilizer production costs, so when world gas prices rise, fertilizer prices are likely to increase. Vietnamese businesses with the advantage of domestic gas self-sufficiency can benefit from the price difference compared to international competitors.

Fifth, equities that are particularly sensitive to rising interest rates and exchange rate volatility—such as brokerage firms, companies heavily reliant on imported raw materials, and those carrying substantial USD-denominated debt—would face indirect downside pressure if elevated oil prices and shipping costs persist. Prolonged increases in input and financing costs could compress margins and weigh on earnings visibility.

Sixth, the aviation sector (e.g., HVN, VJC) is likely to be among the hardest hit. Jet fuel (Jet A1) typically accounts for around 40% of operating expenses. A 30– 40% increase in oil prices would materially strain profitability, particularly if airlines are unable to pass higher fuel costs on through ticket price adjustments. In addition, airspace closures across parts of the Middle East would force Europe-bound flights to reroute, increasing fuel burn and operating costs. For plastics and rubber manufacturers, most key inputs—such as PVC and PP resins—are petroleum derivatives. A sustained rise in input prices would directly compress gross margins for companies such as BMP, NTP, DRC, and CSM, especially if cost pass-through to end customers proves limited.

Author: NGOC ANH

RECOMMENDED TOPICS