VN

VN

EN

EN

25/07/2026, 02:38

Investment

Middle East conflict: Impacts on oil and gas stocks

Sustained elevated oil prices are expected to serve as a key catalyst for oil and gas equities in the near term.

The elevated oil prices are expected to incentivize operators to accept higher day rates and increase rig utilization.

Oil supply tightness

Amid escalating geopolitical tensions in Iran and several neighboring countries, MBS expects partial supply disruptions to materialize. Market signals and reports indicate that Iran has declared a closure of the Strait of Hormuz, with tanker traffic effectively halted, directly impacting crude shipping flows.

According to Kpler data, approximately 13mb/d of crude oil transited through the Strait of Hormuz last year, accounting for roughly 31% of global seaborne crude trade and 20% of total global oil production. The closure has also prompted Iraq to cut output by 1.5mb/d (equivalent to 1.4% of global supply), further tightening the global supply balance. In the event of a prolonged and complete closure of the Strait of Hormuz, oil prices could exceed USD 100/bbl, with extreme scenarios projecting USD 130–200/bbl if 10–20% of global supply were disrupted, equivalent to a loss of approximately 10– 20mb/d.

However, MBS assigns a low probability to this worst-case assumption. Our base case assumes that flows through the Strait of Hormuz will not be entirely cut off but rather face congestion and logistical disruptions. The impact would primarily affect overall transit and export capacity, delaying shipments to key consuming hubs rather than eliminating supply outright.

Under this scenario, MBS estimates that approximately 2–5mb/d could be temporarily “absent” from the market following the escalation, equivalent to 1.8–4.7% of global oil supply, instead of the 10–20% loss implied in the extreme case. Accordingly, MBS projects a supply shortfall of around 2.9mb/d in 2026 when assessing the global supply–demand balance.

In the event of a prolonged conflict that materially constrains supply and sustains oil prices above USD 100/bbl for an extended period, coordinated mitigation measures are likely to be implemented to stabilize the market, including:

First, naval escorts and multinational patrols: Deployment of destroyers, minesweepers, and surveillance UAVs to safeguard tanker convoys, alongside enhanced maritime intelligence-sharing mechanisms among Gulf states and major importing countries to secure key transit routes.

Second, reactivation of war-risk insurance coverage: The restoration of war-risk insurance and trade finance (e.g., L/C issuance) would incentivize shipowners and cargo holders to resume operations, effectively easing financial bottlenecks that constrain physical supply flows.

Third, logistics adjustments and alternative routes: Crude flows may be rerouted via the East–West (Petroline) pipeline in Saudi Arabia, transporting oil from the Persian Gulf to Yanbu on the Red Sea, or through Egypt’s SUMED pipeline linking the Red Sea to the Mediterranean. Importers may also increase sourcing from the U.S., Brazil, and West Africa, accepting higher ton-mile demand and freight costs to maintain delivery volumes.

Fourth, plicy intervention and market regulation: OECD and IEA members could coordinate short-term releases from strategic petroleum reserves (SPR) to cushion supply shocks. OPEC may also temporarily adjust production quotas should tangible supply disruptions materialize.

Global oil demand on a recovery trajectory

Global crude demand continues to expand, primarily driven by emerging Asian economies—most notably China and India—as well as non-OECD countries. In contrast, OECD demand remains on a structural downtrend amid energy transition policies, efficiency gains, and rising electric vehicle penetration. This divergence underscores a clear bifurcation in demand dynamics: growth in the East versus gradual contraction in the West.

In addition, precautionary strategic stockpiling amid heightened geopolitical risks is reshaping short-term demand patterns. Major importers such as China and India are reportedly increasing crude purchases to replenish inventories, temporarily strengthening spot demand.

Importantly, real end-use consumption has shown limited sensitivity to the current Middle East tensions. Industrial fuel use, logistics activity, and inventory accumulation are expected to sustain positive demand growth this year. According to OPEC projections, global oil demand could reach approximately 106.5– 107.7mb/d by end-2026, representing an increase of roughly 1.3–1.4mb/d yoy.

MBS leans toward a base-case scenario in which tensions in the Middle East persist at a moderate level, with Brent crude fluctuating within the USD 75–85/bbl range. A swift and comprehensive de-escalation appears unlikely in the near term, given the extent of damage incurred and Iran’s ongoing retaliatory actions across the region. The extreme scenario—a prolonged and full closure of the Strait of Hormuz—would likely materialize only in the event of broader military intervention and a deliberate decision by Iran to halt maritime transit entirely. Such a move would, in turn, trigger significantly stronger military responses from multiple parties, raising the risk of a wider regional conflict.

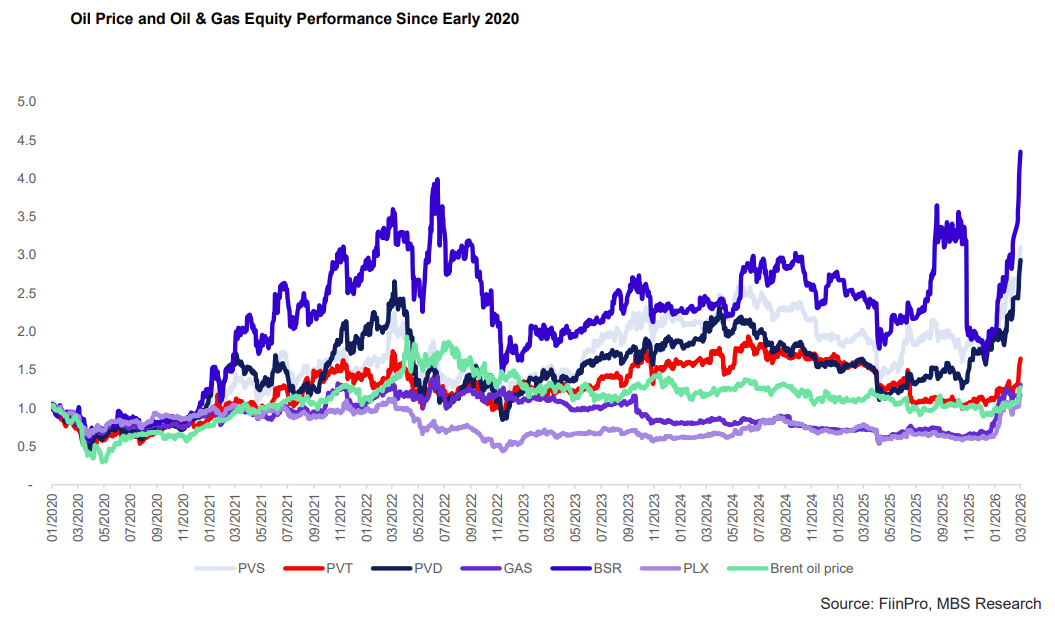

What stocks to consider?

Among the oil and gas stocks, investors could consider opportunity investment for the following ones:

First, in a high oil price environment driven by the Iran conflict, PVS’s FSO leasing segment benefits indirectly as operators prioritize output optimization, supporting long-term floating storage demand. Given the long-term, fixed day-rate structure of FSO contracts, cash flows remain relatively stable and less sensitive to short-term oil price volatility.

While higher war-risk insurance costs may exert mild pressure on operating expenses, earnings impact should be limited absent large-scale transport disruptions. Elevated oil prices also stimulate EPCI demand, with more projects being reactivated or accelerated, leading to stronger order backlog growth. Notably, sustained high prices could expedite the development timeline of the Cá Voi Xanh project, providing additional upside to PVS’s medium-term workload.

Second, MBS expects elevated oil prices to incentivize operators to accept higher day rates and increase rig utilization. PVD I, VI, VIII, and IX— scheduled to commence new drilling contracts in 2026—are well positioned to benefit from improved pricing terms and stronger demand conditions.

Third, higher oil prices typically lift gas selling prices indexed to international oil benchmarks, supporting revenue and earnings growth across most of GAS’s commercial gas portfolio. However, regulated gas volumes sold under fixed-price offtake agreements may not fully capture the upside due to fiscal adjustments and benefit-sharing mechanisms with the state.

In addition, any delay in LPG supply could weigh on earnings, as projected price increases may not fully offset volume shortfalls. That said, LPG contributes only 6% of GAS’s gross profit, limiting downside impact, which is likely to be offset by stronger margins in the dry gas segment (76% of gross profit) as non-regulated gas prices adjust upward.

Fourth, rising oil prices typically translate into higher freight rates, or fuel cost pass-through mechanisms, thereby protecting transportation cash flows. The majority of PVT’s fleet operates under medium- to long-term contracts (1–5 years), limiting immediate exposure to short-term geopolitical volatility. However, in a prolonged Hormuz closure scenario (oil > USD 100/bbl), vessel utilization could decline, potentially weighing on PVT’s earnings performance.

Fifth, elevated oil prices significantly increase input costs; however, MBS expects crack spreads to widen in response to tighter product supply conditions, partially offsetting feedstock pressure. BSR benefits from access to domestic crude and the operational stability of Dung Quat Refinery, supporting throughput and margin expansion in line with global crack spread trends. That said, in a more severe escalation scenario—particularly if oil exceeds USD 90/bbl—imported crude (accounting for 30–35% of BSR’s feedstock) could face disruptions. Limited ability to promptly substitute with domestic supply may pressure refinery utilization and earnings.

Sixth, price stabilization mechanisms (e.g., the fuel price stabilization fund) may limit the pace of domestic price adjustments, preventing PLX from fully passing through higher input costs in the short term. PLX currently holds approximately VND 2,763bn in inventories (raw materials, in-transit goods, and finished products) at lower historical costs, creating potential short-term inventory gains if oil prices continue to rise. MBS assesses that under a moderate oil price increase (contained conflict scenario), PLX could benefit from low-cost inventory sales. However, in a severe escalation scenario, margin compression and potential supply shortages may outweigh short-term gains.

Author: NGOC ANH

RECOMMENDED TOPICS