VN

VN

EN

EN

22/07/2026, 02:38

Investment

VCB: A defensive stock with an attractive valuation

VCB - The stock of the Joint Stock Commercial Bank for Foreign Trade of Vietnam (Vietcombank, HoSE) is evaluated to have positive advantages thanks to policy benefits and the bank's strong fundamentals.

Two of the important recent policies from the monetary market regulatory authority are both related to VCB.

"Benefiting from Policies"

First, the State Bank of Vietnam (SBV) issued Circular 08/2026/TT-NHNN, which allows 20% of the State Treasury's term deposits to be calculated into the LDR (Loan-to-Deposit Ratio) denominator. This will help VCB improve liquidity, reduce fund mobilization pressure, and increase room for credit growth in the coming period.

Second, Circular No. 25/2026/TT-NHNN amends and supplements several articles of Circular 22/2019/TT-NHNN regulating limits and safety ratios in the operations of banks and foreign bank branches. Notably, the most remarkable point in this new Circular is the increase of the maximum ratio of short-term funds used for medium and long-term loans (SMLR) from the current 30% to 40%, effective from July 1, 2026.

VCB's participation in the mandatory transfer of a weak credit institution helps it secure a 50% reduction in the reserve requirement ratio and removes quarterly credit growth limits. (Illustration photo)

VCB's participation in the mandatory transfer of a weak credit institution helps it secure a 50% reduction in the reserve requirement ratio and removes quarterly credit growth limits. (Illustration photo)

Vietcombank Securities (VCBS) assesses that the most notable impact of Circular 25 is creating more space for banks to expand medium and long-term lending, thereby enhancing the capacity to supply capital to the economy.

VCBS also believes that the state-owned banking group consisting of BIDV, VietinBank, and Vietcombank currently maintains the SMLR ratio at a fairly safe level of around 20-25%. This group possesses the advantage of a stable, long-term deposit base and large capital scale. Combined with the modification of the LDR formula that allows adding back 20% of the State Treasury's term deposit balance into mobilization, state-owned banks will receive liquidity support to boost credit in sectors such as public investment, transport infrastructure, and energy.

Furthermore, aligned with Official Dispatch 5386/NHNN-TD which allows 18 key projects to be exempted from credit rooms, creating positive impacts on the banking and construction industries and promoting growth, it removes financing bottlenecks for 3 major enterprises accessing long-term capital (Vingroup, Sun Group, Masterise Aviation Infrastructure...). Consequently, leading banks in financing and co-financing national key infrastructure projects according to guidelines, such as VCB, BIDV, and CTG, will also "benefit".

In reality, VCB holds numerous advantages with its leading industry position, maintaining the "profit crown" across the entire system for many years. It possesses both internal strength and excellent asset quality with a low non-performing loan (NPL) ratio, a high bad debt coverage ratio, and a CASA ratio in the top tier of the system.

Outstanding Credit Growth

According to Ms. Nguyen Ky Duyen, an analyst at ABS Securities, VCB's business results are expected to be positive because:

- VCB maintains the advantage of a high CASA ratio and low cost of capital, helping mitigate NIM narrowing pressure compared to the industry.

- It holds strong advantages in corporate, FDI, and key infrastructure project customer segments. Notably, FDI outstanding loans continue to be an important growth driver thanks to the supply chain shifting trend and foreign investment capital inflows into Vietnam.

Additionally, VCB's participation in the mandatory transfer of a weak credit institution helps it secure a 50% reduction in the reserve requirement ratio, equivalent to about VND 24.5 trillion in disposable capital, while being exempted from quarterly credit growth restrictions.

The ABS expert also mentioned the advantages of improved liquidity, reduced mobilization pressure, and increased room for credit growth in the upcoming period thanks to the SBV's issuance of Circular 08/2026/TT-NHNN.

Remarkably, VCB is planning a private placement of up to 6.5% of its charter capital, which is expected to help VCB supplement its Tier 1 capital, improve CAR, increase credit growth room, and attract strategic investors.

This bank is also outstanding for its asset quality, which continues to be a prominent strength with an NPL ratio of only 0.62% and a bad debt coverage ratio of about 253%, among the highest in the system. This helps VCB maintain low credit costs and creates room for provision reversals in the future.

By the end of the first quarter, VCB maintained a positive performance with VND 17,651 billion in net interest income (29% YoY) and VND 11,803 billion in pre-tax profit (8.7% YoY), driven by outstanding credit growth (4.8% YTD) and an improved NIM.

For 2026, the bank aims for a credit growth target of around 10% and not exceeding the 13% cap assigned by the State Bank of Vietnam. Market 1 fund mobilization will be managed appropriately in line with credit growth. The bank sets a profit growth target of about 5%, with the NPL ratio maintained below 1.5%.

Reportedly, in 2025, VCB recorded outstanding credit of about VND 1.7 quadrillion, with total assets exceeding VND 2.4 quadrillion. Pre-tax profit reached VND 44,020 billion, continuing to lead the system, and market capitalization reached approximately USD 18 billion.

Ms. Nguyen Thi Ky Duyen noted, however, that investment risks could occur if credit growth falls short of expectations should the SBV continue to tighten regulations related to liquidity and credit growth.

Defensive Stock with an Attractive Valuation

According to VDSC's forecast for Q2/2026, projected net interest income is estimated at VND 17,900 billion (26% YoY), in which credit growth is expected to reach 6.5% YTD or 14.5% YoY, and the projected NIM will decrease slightly compared to Q1/2026 to 2.8% (-5 bps YoY and 15 bps YoY), reflecting the time lag of rising capital costs in Q2.

With the expectation that credit risk provisioning expenses will continue to increase sharply compared to the same period due to the low base of Q2/2025, and that the bank will partially provision for corporate bond bad debts that were not provisioned in Q1/2026 (VND 3,300 billion), credit risk provisioning expenses are estimated at VND 1,750 billion (116% YoY), corresponding to a credit cost (Q) of 0.1% in Q2/2026, reaching over VND 12,600 billion (14% YoY).

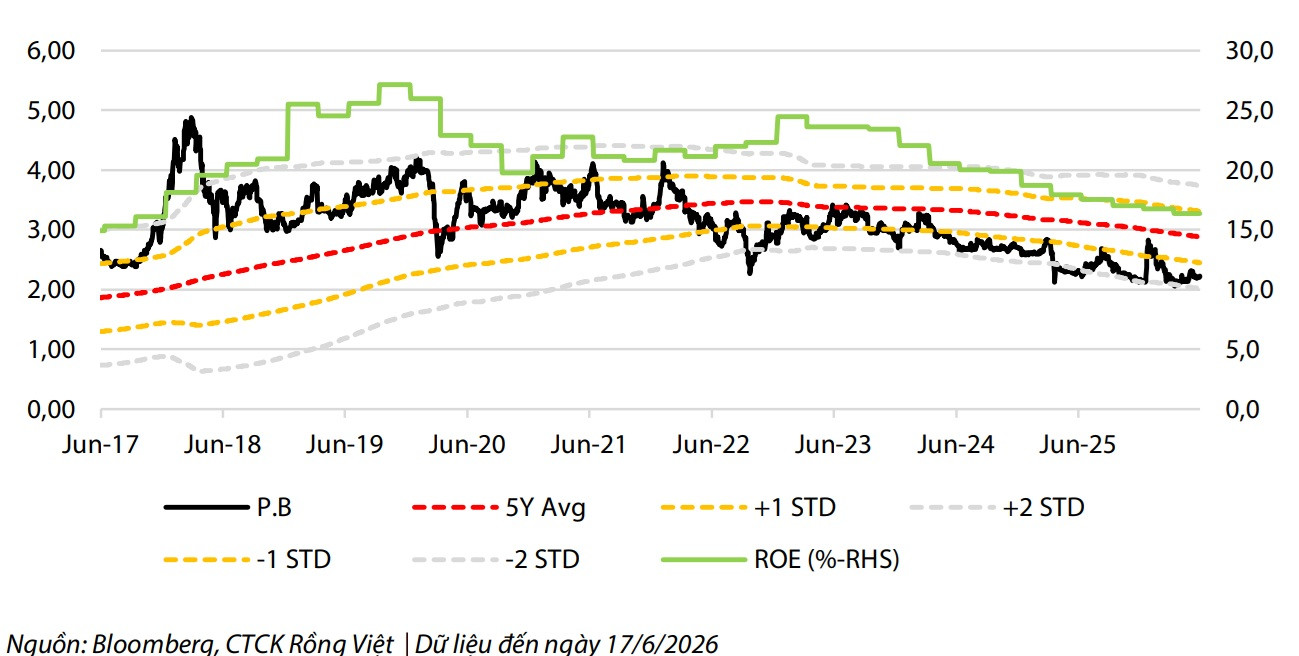

VCB is trading at its valuation bottom as ROAE continuously declines and pressure from the cost of equity is rising.

For the whole year of 2026, main assumptions are maintained: Projected credit growth reaches 14.6%, NIM expands by nearly 20 bps YoY to 2.8% as the NIM trend at the beginning of the year and Circular 08 reinforce this view. Projected net interest income increases by 25% YoY, helping total operating income grow by 18% YoY. With expectations that VCB will well control CIR at 33.4%, and the NPL ratio (including corporate bonds) at 1.0%, overall, VCB's pre-tax profit is projected to grow stably at 14% YoY.

VDSC values VCB's trailing P/B at 2.2x – lower than nearly 2 standard deviations compared to the 5-year average (2.9x) – while the projected 2026F P/B is only at 2.0x. Analysts state that this is an attractive valuation zone for a bank possessing sustainable competitive advantages: asset quality controlled at the top of the system with an overall NPL below 1% and a thick provisioning buffer; a Capital Adequacy Ratio (CAR) of nearly 12%, expected to be further strengthened by the private placement plan scheduled for implementation this year, ensuring sustainable room for credit growth in the long term.

In the context where interest rates could fluctuate and exchange rate risks continue to persist in 2026, VCB stands out as a defensive choice with an attractive valuation. Accordingly, the analyst group maintains an "Accumulate" recommendation with a target price of VND 68,500/share. Compared to the closing market price of VND 61,400/share on June 26, the expected return is approximately 11.56%.

Author: LE MY - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS