VN

VN

EN

EN

16/07/2026, 10:55

Investment

Vietnam power sector: A new cycle is emerging

The Vietnam power sector’s next phase is expected to focus on clean and flexible power—renewables, LNG-to-power, nuclear, pumped-storage hydropower and BESS.

POW is pursuing an ambitious LNG pipeline, including Quang Ninh LNG (1,500MW), Quynh Lap LNG (1,500MW) targeted before 2031.

The Vietnam power sector has entered 2026 amid negative developments involving misconduct at several power consulting and construction firms, weighing on sentiment throughout the first half while legacy issues remain unresolved. Nevertheless, decisive government action to complete the policy framework has created bright spots. The power sector remains essential to economic development and should offer opportunities in the next cycle. MBS expects the next phase to focus on clean and flexible power—renewables, LNG-to-power, nuclear, pumped-storage hydropower and BESS. Recent policy developments are concentrated on these areas, and a clearer, more stable framework should improve investor confidence.

Electricity consumption grew a solid 10% in 1H26 as extreme heat drove a surge in residential demand. Thermal generation improved and offset weaker hydropower, while renewable dispatch remained stable and curtailment was no longer significant.

Looking into 2H26, a strong El Niño cycle should keep temperatures and electricity demand elevated. The key theme will be greater thermal dispatch to offset hydropower. MBS expects dispatch conditions to remain stable versus 2025; hydropower and coal plants may benefit from stronger market prices, while gas-fired plants should continue receiving adequate contracted output (Qc) to maintain system readiness as supply pressure rises.

As for the long-term outlook, with power-plant implementation facing material delay risks, the Government is building a legal framework to accelerate investment in priority sources. We see three key themes: (1) promoting clean renewable investment; (2) maximising distributed generation—rooftop solar plus BESS—to reduce system pressure; and (3) introducing tailored mechanisms and removing bottlenecks for flexible sources such as LNG-to-power, offshore wind and nuclear.

The amended 2026 Electricity Law is being finalised, prioritising a stable, predictable and coherent legal framework. Supporting circulars and decrees are also being completed in parallel for expedited issuance:

First are the renewables. Amend Decree 57/2025/NĐ-CP on DPPAs and Decree 58/2025/NĐ-CP on renewable development. The DPPA mechanism is broadened by expanding eligibility, removing price-cap constraints and improving service-cost transparency. Rooftop solar is strongly encouraged, with surplus sales raised from 20% to 50%, streamlined investment procedures and added incentives for BESS integration.

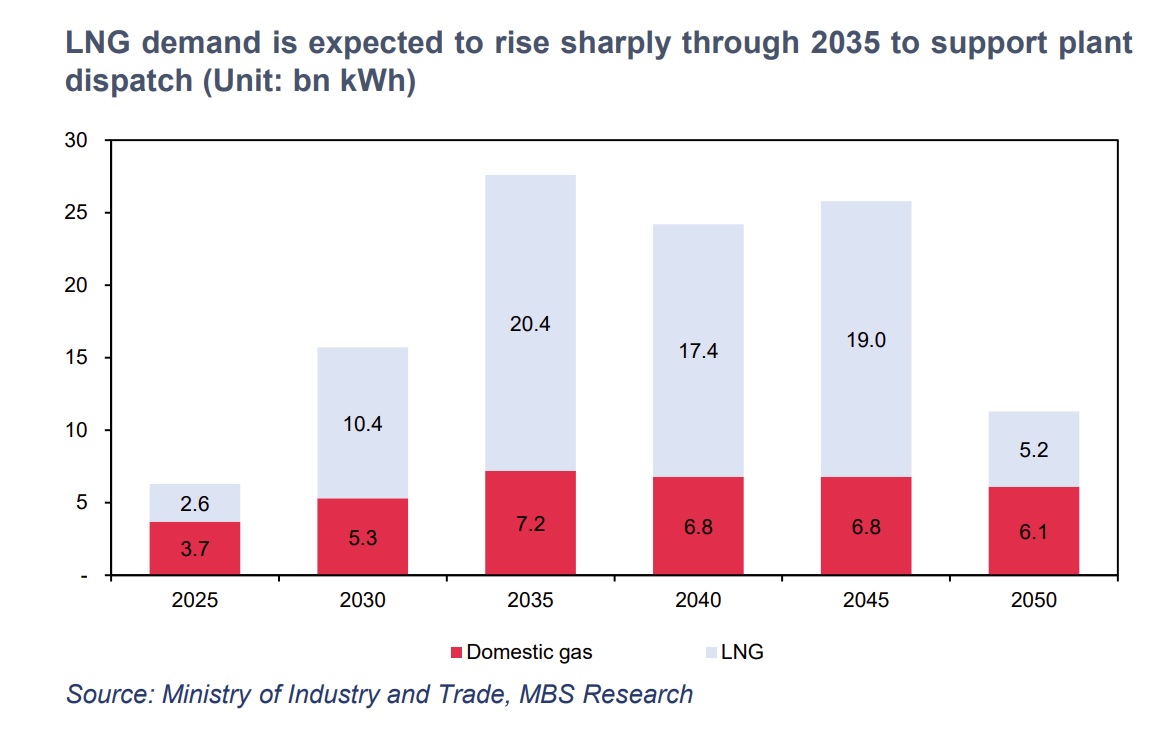

The gas-fired power comes in second. Amend Decrees 56/2025/NĐ-CP and 100/2025/NĐ-CP, proposing incentives for LNG plants commissioned before 2031, including raising the minimum Qc from 65% to 75% and extending the offtake period from 10 to 15 years. The changes aim to attract investment in a segment facing high delay risk under PDP8.

Among power stocks, MBS selected POW, REE for the 2026 investment strategy, consistently favoring companies positioned to benefit from policy support:

For POW, it is pursuing an ambitious LNG pipeline, including Quang Ninh LNG (1,500MW), Quynh Lap LNG (1,500MW) targeted before 2031. The sector outlook is improving as the Ministry of Industry and Trade finalises measures to remove gas-power bottlenecks, notably a proposal to raise LNG Qc offtake from 65% to 75% for the first 15 years. After Nhon Trach 3&4 began operation in 2026, POW is pursuing Quang Ninh LNG (1,500MW), Quynh Lap LNG (1,500MW) targeted before 2031, and potential investments in Ca Mau 3 LNG (1,200MW) and Nhon Trach 5 (600MW), reinforcing its leading position.

Dispatch conditions have improved over the past two years, with high QC allocations every six months—a minimum of 48% for domestic gas and 65% for LNG. This is increasingly important as high selling prices reduce gas plants’ competitiveness in the market.

POW’s exceptional 2026 earnings growth is driven by improved plant gross margins and one-off revenue at Vung Ang and Ca Mau 1&2. From 2027, sustained electricity demand growth above 10% through 2030 should support plant dispatch.

As for REE, it is a diversified utility company with strong cash flow from power, clean water and office leasing. Its financial capacity and healthy balance sheet support proactive M&A and high-return investments.

Power projects are the main growth focus. In 2026–2028, REE plans about 400MW, including 376MW of nearshore wind and the 30MW Tra Khuc 2 hydropower project. It is also seeking approvals for floating solar on its reservoirs and studying the 500MW Southern Offshore Wind 3 project. MBS views REE’s power-growth potential positively, given its capital base and execution track record.

P/B has returned to its two-year trough average of 1.5x while 2026–27 ROE remains about 10–11%, making REE attractive amid interest rate and inflation risks. Strong cash flow, sound finances and reasonable leverage support a defensive investment case, with net profit expected to grow at a sustainable 14% CAGR in 2026–2027.

Author: NGOC ANH

RECOMMENDED TOPICS