VN

VN

EN

EN

16/07/2026, 02:38

Investment

The Sustained Decline of Open-Ended Funds: A Cause for Investor Concern?

Huynh Hoang Phuong, a Financial Investment Analyst, asserts that the disappointment of many investors is completely understandable given the performance of equity open-ended funds over the past two years.

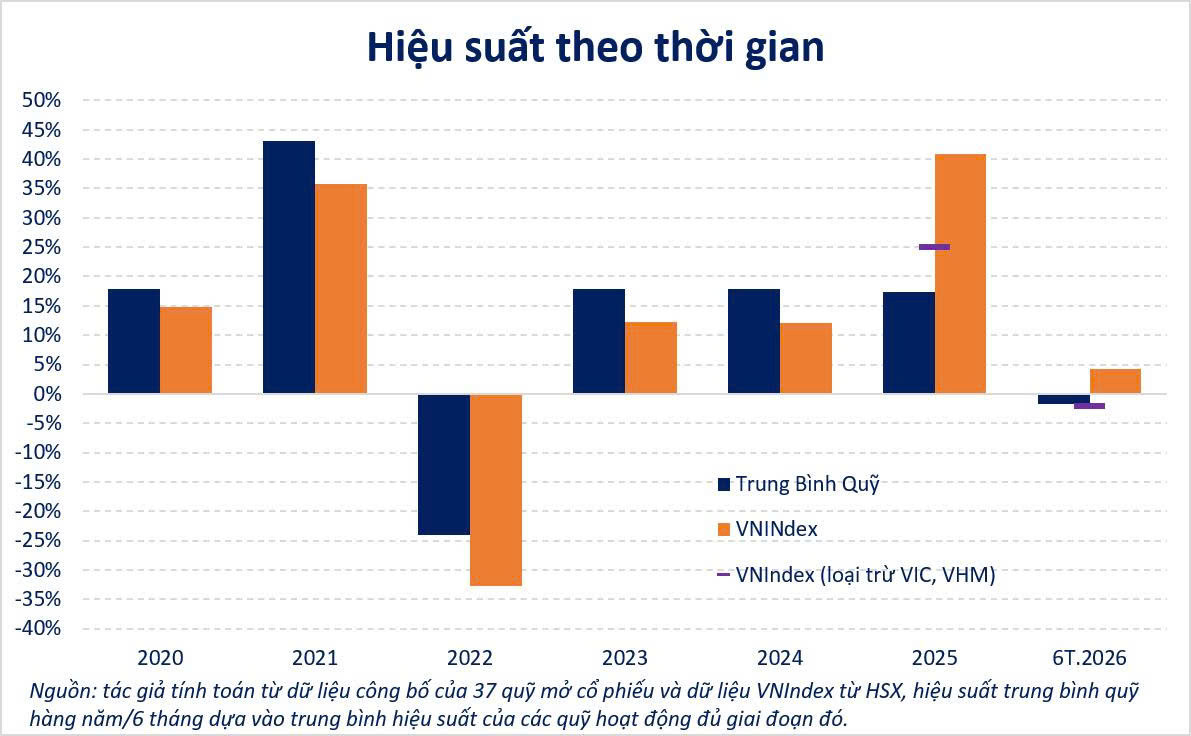

In 2025, not a single equity open-ended fund surpassed the growth rate of the VN-Index. Moving into the first half of 2026, the situation has barely improved, with only 1 out of 37 equity open-ended funds on the watchlist outperforming the VN-Index.

Open-ended funds are continuously "beaten by the market"; should investors be discouraged? (Photo: Quoc Tuan)

Looking at these figures, many naturally ask: If investing through funds still cannot beat the market, is it worth continuing? This question is completely justified and is something fund management companies must take seriously. Investment performance remains the most critical criterion for investors, and prolonged poor results will inevitably erode trust.

However, focusing solely on the last two years might obscure a crucial part of the broader picture. During the five consecutive years from 2020 to 2024, the average performance of equity open-ended funds beat the VN-Index by 3 to almost 9 percentage points annually. The proportion of funds outperforming the index consistently ranged between 73% and nearly 90%, even during sharp market downturns like in 2022.

This raises a more thought-provoking question: If the same management teams, with the same investment philosophies, historically generated relatively stable alpha (outperformance over risk) for years, what caused almost the entire industry to collectively underperform in just two years? Perhaps the answer lies not solely with the funds themselves.

When the market only rewards a highly distinct strategy

The year 2025 witnessed the VN-Index surge by over 40%. Yet, behind that impressive figure lies a stark contrast to previous cycles: the index's profitability was heavily concentrated in a small number of large-cap stocks, particularly the Vingroup's ones.

Performance over time

Meanwhile, the majority of equity open-ended funds did not allocate a high proportion to this specific group. This is not necessarily a "missed opportunity," but rather a reflection of how funds operate: prioritizing portfolio diversification, risk control, and avoiding over-reliance on a few individual stocks. Consequently, the performance gap between these funds and the VN-Index widened significantly.

In the first six months of 2026, this paradox became even more pronounced. The VN-Index increased by over 4%, but excluding the impact of a few leading stocks, the broader market actually performed poorly. In other words, many investors likely felt their portfolios "didn't grow at all," even as the index continuously set new milestones.

This period also coincided with numerous fundamentally sound businesses—traditionally favored by funds and weighted more heavily than the index—suffering from legal issues or governance risks. Cases like DGC, PC1, or recently PNJ caused significant drawdowns in many investment portfolios.

From a fund management perspective, this is a period of "dual impact." On one hand, funds missed out on the narrow rally driven by a few index-heavy stocks. On the other hand, the very stocks they selected based on fundamental criteria encountered unpredictable headwinds.

More importantly, this phase demonstrates that the VN-Index and the broader market no longer move in tandem as they did in previous years. When the index's growth depends too heavily on a select few stocks, "beating the VN-Index" is no longer just about picking good companies; it relies heavily on concentrating allocations in the right market leaders. While this strategy can yield outstanding returns, it also carries significantly higher risks if the trend reverses.

Don't let a specific period dictate your entire investment strategy

The preceding analysis does not aim to deny the reality that open-ended funds have underperformed the VN-Index for the past two years. This is a truth both investors and fund management companies must acknowledge. However, it does not imply that all funds have lost their edge or that their investment philosophies are obsolete.

Investing is inherently a process of trade-offs. A highly concentrated portfolio may outperform during periods led by a few large caps, but it will face extreme volatility when those stocks reverse. Conversely, a diversified portfolio accepts short-term underperformance against the index in exchange for superior long-term risk control.

For individual investors, rather than obsessing over one or two years of performance rankings, this might be the ideal time to evaluate funds over a longer cycle by answering three critical questions:

First, does the underperformance stem from a breakdown in the fund's investment process, or is it a symptom of a highly specific market phase?

Second, does the fund maintain its investment discipline and consistent philosophy, or has it chased short-term trends to artificially inflate its track record?

And finally, is your ultimate goal to maximize profits every single year, or to build and accumulate assets sustainably across multiple market cycles?

Ultimately, the hallmark of a successful long-term investment strategy is not ranking first every year, but the ability to deliver stable growth across various market cycles. Data from 2020–2024 demonstrates that the majority of equity open-ended funds achieved exactly that. The 2025–2026 period, therefore, serves as a timely reminder for investors to calibrate their expectations and address these three fundamental questions to ensure their fund strategy aligns with their path to long-term wealth building.

Author: TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS