VN

VN

EN

EN

12/07/2026, 02:38

Investment

Opportunity to disburse into the banking stocks

Liquidity pressure from the gap between mobilization and outstanding loans, rising bad debt risks, and the diverging business results of commercial banks have not dampened the positive outlook for banking stocks.

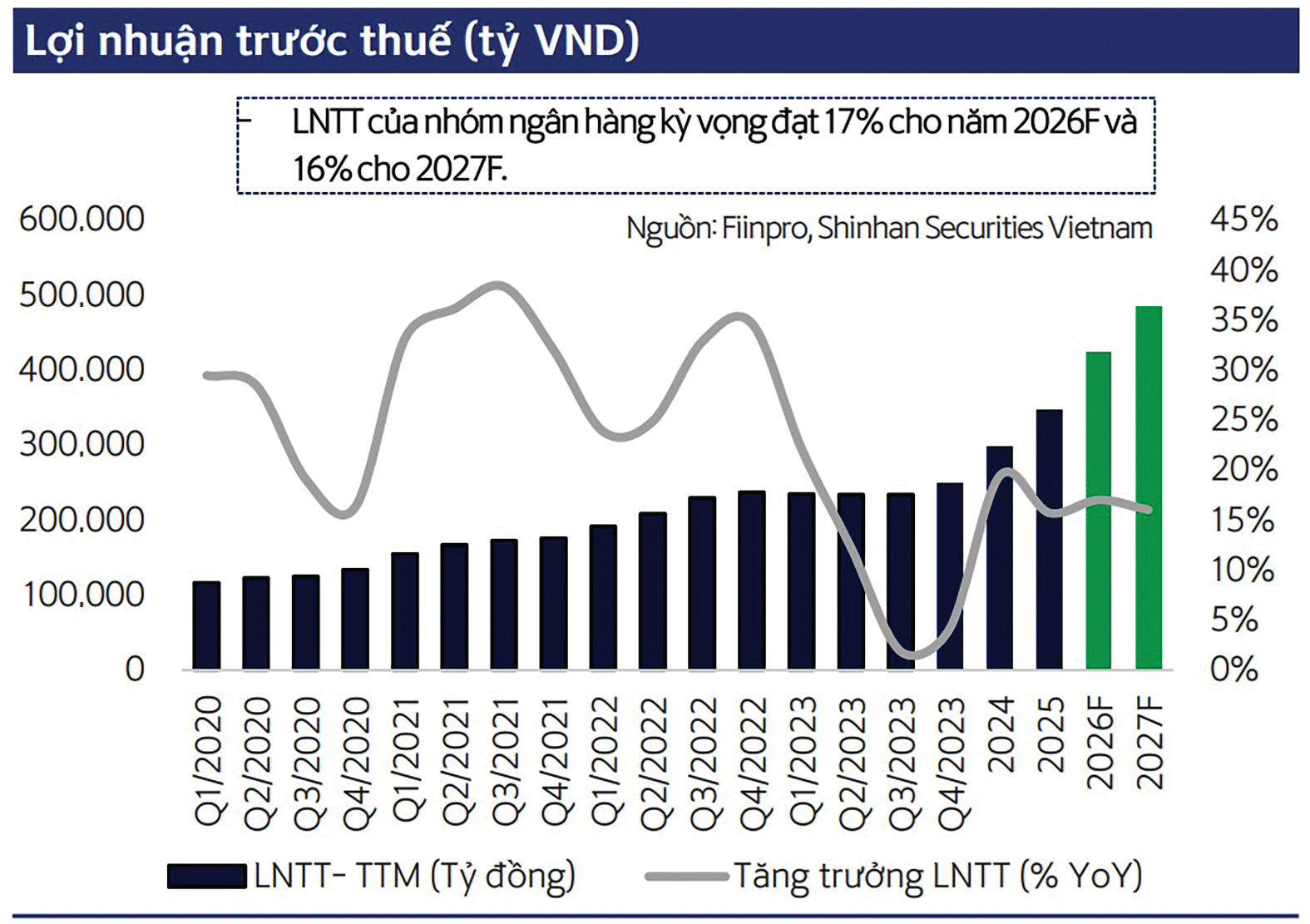

Forecasted profits of the banking sector. (Source: SSV)

Forecasted profits of the banking sector. (Source: SSV)

Investors may consider disbursing into this stock group if liquidity turns positive and profit growth reaches around 17%.

The Foundation of Profit

Updated data shows that in May, the entire banking industry achieved credit growth of 5.71%, and 7.4% in June. Capital mobilization reached 5% by June. This indicates that the gap between mobilization and lending remained negative, at up to 2.4%, which is a very large figure. Within this, the credit growth of listed banks showed divergence. In particular, banks participating in the restructuring program for weak banks, such as HDB, MBB, and VPB, recorded outstanding growth compared to the industry average. Most of the remaining banks maintained growth closely aligned with the credit limits assigned by the State Bank of Vietnam (SBV) since the beginning of the first quarter of 2026.

Meanwhile, interest rates rose rapidly in the fourth quarter of 2025 and maintained this high level throughout the first and second quarters of 2026. However, customer deposit growth in Market 1 of listed banks in the first quarter diverged and was generally much slower than the pace of credit growth.

Mr. Nguyen Duong Phuong, CFA, Head of Analysis at Shinhan Securities Vietnam (SSV), explained that this could be attributed to the high volume of cash in circulation at the end of the year, related to tax policies and Tet seasonal factors. This led to a large amount of demand deposits being withdrawn, slowing down deposit growth at some banks in the first quarter of 2026.

"When Market 1 grows slowly and fails to keep pace with lending growth, banks are forced to promote other mobilization channels. Systemic liquidity faced pressure at certain times in 2026 due to several key factors, but with the regulatory efforts and policies of the SBV, this situation is expected to improve in the second half of this year," Mr. Phuong assessed.

Divergent Results, Attractive Valuations

According to first-quarter business results, banks experienced divergence, but the common thread was flat or slightly declining Net Interest Margins (NIM) due to the impact of high interest rates. Accordingly, Mr. Nguyen Duy Phuong highlighted several key points, such as banks' net interest income growing by about 16%. NIM was flat, with some banks pushing medium and long-term loans recording better NIM improvement compared to the State-owned commercial banks group. For private commercial banks involved in restructuring projects, the growth in net interest income primarily came from expanding asset scale rather than improving NIM.

According to Mr. Nguyen Duong Phuong, CFA, Shinhan Securities Vietnam (SSV), the banking industry's profit is projected to grow by approximately 16-17% during 2026-2029. (Illustration photo: Quoc Tuan)

The average return on cost of funds fluctuated relatively in tandem with the upward trend of deposit and lending rates in the market. Non-interest income recorded a slight increase of about 6%. Income from service activities is a segment that many banks highly expect to develop strongly in the near future to reduce reliance on net interest income.

Notably, according to Mr. Phuong, building ecosystems, wealth management, and insurance distribution are being pushed forward to diversify revenue sources.

In the market, many commercial banks are expanding into strong ecosystems, from the listed Big 3 group like VCB, BID... to top-tier private commercial banks like TCB, VPB, SHB, HDB... The ecosystem trend is unlikely to stop, with banks driving internal restructuring to rise up, such as EIB, OCB, KLB... and the market will likely witness many other "expansions" in the future. However, it is still too early for income from consolidated ecosystem benefits to reflect a corresponding growth rate.

In addition, optimizing and cutting inefficient operating costs has been a clear trend over the past two years. Thanks to this, the cost-to-income ratio (CIR) of banks was very well controlled during 2024 and 2025, and is expected to be maintained in the coming years. However, overall operational efficiency has declined compared to the previous period. The reason is that net interest income and NIM have continuously decreased year after year. Even though costs have been tightly controlled, overall operational efficiency still faces downward pressure.

Pre-tax profit of banks is estimated to have grown by about 13% in the first quarter, closely tracking the targets approved by the Annual General Meeting of Shareholders (AGM). Consolidated data shows that the profit target for this banking group is projected to increase by 17% this year. By the end of the first quarter of 2026, the progress achieved was about 23%, fully in line with the set plan.

"Regarding asset quality, first-quarter 2026 data is still too early to provide more comprehensive long-term analysis, especially since bad debts usually manifest more clearly at the end of the second quarter," Mr. Phuong observed. Projecting a further outlook for both 2026 and 2027, Mr. Phuong believes that the banking sector's profit will grow by about 16-17%. The main underlying assumptions include credit growth reaching 15% and NIM remaining flat at 3%. Regarding asset quality, a conservative forecast indicates that bad debt may rise slightly in 2027. Consequently, pre-tax profit will maintain a growth rate of around 17% throughout the 2026-2027 period.

According to SSV's valuation, listed bank stocks are currently trading below their 5-year average P/B ratio. This valuation level has already priced in concerns over capital costs, rising interest rate pressures, as well as risks related to liquidity and asset quality in the first half of the year. However, if liquidity moves positively as expected in the coming period and profits sustain a 17% growth rate, the current valuation range is completely suitable for considering investment disbursement.

Author: LE MY - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS