VN

VN

EN

EN

26/07/2026, 02:38

Business economics

What are the prospects for global oil price?

Global oil price could continue its uptrend thanks to the sluggish supply and global demand recovery. However, FED's rates hike and US-Iran nuclear talks could be considered major risks.

In VNDirect’s view, the average Brent oil price is expected to be resilient on the price band around US$70/bbl in FY21-23F.

Global demand on track to the recovery

Thanks to the positive vaccination campaigns (e.g., the vaccinated rate in US, UK is 63.4% and 71.4% as of 24 September, respectively) combined with the fiscal stimulus, some major economies have strong recovery in 1H21. In June 2021, World Bank forecasted that China's GDP could increase 8.5% in 2021 instead of the target of 6% set by the Chinese Government. Hence, the strong growth of China, along with the US recovery, will be the leading driver of the global economic prosperity after the pandemic, thereby boosting global oil demand.

Based on US Energy Information Administration (EIA) in September, the U.S. stockpiles fell by 3.5 million barrels to 414 million, which is near a three-year low. EIA forecasts the global oil demand could increase by 5.0 million barrels per day (mbd) in 2021F to the average of 97.4 mbd from the sharp fall of 8.6 mbd in 2020, before reaching the average of 101.0 mbd in 2022F, almost even with pre-Covid level (2019).

Currently, in the context of natural gas in short supply leading to the soaring gas prices, there would be more focus on crude oil as one of the only viable alternatives. VNDirect expected this would be potential bullish catalyst for the oil market this winter, larger than the downside risk to global oil demand from another Delta-like Covid wave. Goldman Sachs has predicted that Brent could reach US$90/bbl if the weather in the northern hemisphere turns out to be colder than normal this winter, which is a US$10/bbl more than its current forecast.

Supply seems to be still tightened

Despite the strong recovery in global demand, OPEC is still conservative in raising outputs. On 18 July, OPEC decided to gradually increase overall crude production by 400.000 barrels per day on monthly basis starting from August to December 2021, ramping up output by 2 mbd in total by the end of this year. Additionally, the deal also gives that the supply management pact is extended from Apr 2022 to end-2022. This agreement shows that a moderate increase in production would keep the market in supply deficit in the coming months. Meanwhile, despite increasing production following the agreement, OPEC’s oil production was still at 10% below the total quota applicable to the 10 members in August due to lack of investment or delayed maintenance during the pandemic.

The US oil production has been sluggish in response to price rally. According to Baker Hughes, the number of oil operating rigs in the U.S. is 521 in September 2021, but only equal to 55% of the average level in 2019 (around 943 rigs). Consequently, the US oil production has been lacked direction in response to the global oil demand recovery. Beside some issues related to the weather like the cold blast in February or Hurricane Ida in September, VNDirect sees that one of the main reasons comes from the new policy of US President Joe Biden in constraining the US oil industry, reducing the uses of fossil fuels to cope with climate change. In September, EIA estimates the US oil production to reach 11.1 mbd in 2021F (10% lower than the pre-Covid level) and 11.7 mbd in 2022F. Hence, this stock company believed supplies would not rise fast enough to keep pace with the predicted demand recovery, creating the shortage gap that could support for the oil price in coming times.

For the supply risk, VNDirect considers US-Iran nuclear talks as the major risk as this could lead to the return of Iranian exporter with the additional capacity up to 2.1 mbd.

Impact on oil industry

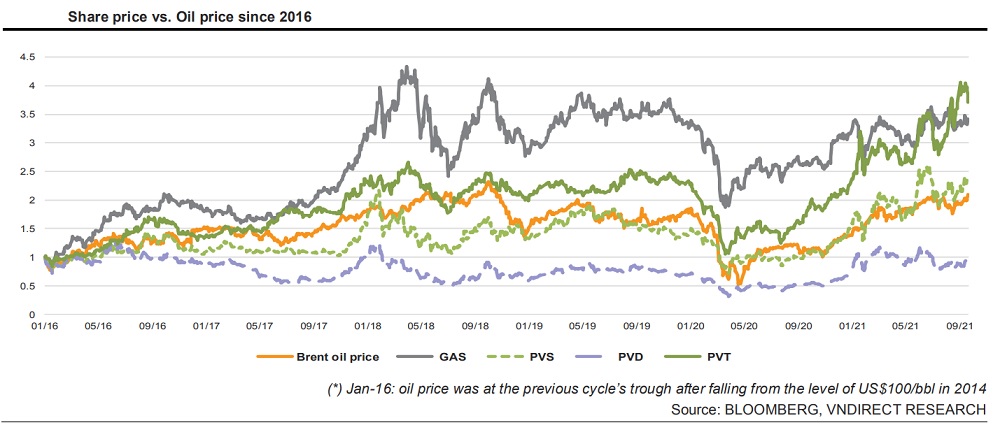

Due to the high correlation to Brent oil price, VNDirect considers oil price would be still the leading driver for oil & gas stocks in coming times. Despite the difficulties in the O&G industry’s activities in 2021 due to the current Covid-19 wave, it believed stronger oil price would not only drive share prices sentiments in short-term, but also improve the industry’s fundamental in coming years as it could give more incentives for relevant units to restart the major projects in Vietnam, firstly providing huge opportunities for upstream companies like PVD and PVS. For instant, all PVD’s jack-up rigs has signed the contracts in 2H21F, signalling that E&P activities in Vietnam have been heating up thanks to higher oil price. Notably, in Vietnam, the Brent oil price sustaining above US$60/bbl is the favourable condition for E&P activities to operate effectively.

In VNDirect’s view, the average Brent oil price is expected to be resilient on the price band around US$70/bbl in FY21-23F, however it still builds other scenarios for oil price mainly on the recovery scenarios of the global economy.

Author: NGOC ANH

RECOMMENDED TOPICS