VN

VN

EN

EN

26/07/2026, 11:20

Investment

What contruction stocks to watch in 2026?

Amid Vietnam’s favorable construction industry conditions as well as its attractive valuations, MBS expects emerging investment opportunities in the construction sector.

CII’s net profit is projected to grow 70% YoY in 2026, driven by construction from the Trung Luong–My Thuan BOT project.

Gross margin remains stable

In Q1 2026, industry backlog is expected to benefit from continued momentum in civil construction and public investment disbursement. In 2026, new apartment supply in HCMC and Hanoi is projected to grow by 14% and 4% YoY, respectively, while social housing supply may rise by 50% YoY. Public investment disbursement is forecast to increase by 18% YoY, supported by key railway projects (Ben Thanh–Can Gio, Hanoi–Hai Phong–Lao Cai) and strategic ring roads (Ring Road 4 in Hanoi, Ring Road 3 in HCMC).

Accordingly, backlog across our coverage is projected to grow by 7%–45% YoY, with stronger growth among civil-focused contractors, driven by (i) accelerated execution of large-scale projects by major developers and (ii) increased delegation to leading developers in key projects. CTD is expected to record the strongest backlog growth, supported by both large civil projects and new wins in major infrastructure projects (e.g., Phu Quoc and Gia Binh airports). For infrastructure corporations (VCG, CII, HHV), backlog growth remains supported by new highway and BOT project wins.

Notably, VCG’s backlog is projected to increase by 7% YoY to VND 26tn, driven by projects such as the Ninh Binh expressway. Meanwhile, BOT operators CII and HHV are expected to see backlog growth of 30% and 25% YoY, respectively, supported by the Trung Luong–My Thuan (Phase 2) project.

In addition to backlog expansion, higher bid prices and stable input costs (notably steel and cement) are expected to support margin expansion. CTD is well-positioned to benefit from technically complex projects (e.g., Trong Dong Stadium, Can Gio), enabling improved pricing; its gross margin is projected to increase by 0.3ppt YoY to 3.4%. VCG’s gross margin is expected to expand by 1.5ppt YoY, supported by its real estate segment, while construction margins remain stable at 5%. Meanwhile, BOT operators (CII, HHV) are likely to maintain stable margins as projects reach steady-state operations.

“Supported by revenue growth and more stable gross margins, Q1 2026 net profit of construction contractors is expected to recover strongly from a low base in Q1 2025. CTD is projected to reach VND 120bn (111% YoY), while CII may increase by 233% YoY. Meanwhile, VCG and HHV are expected to post more moderate growth of 21% and 13% YoY, respectively, driven by solid revenue expansion," said MBS.

Core operations to deliver solid growth

In 2026, earnings of civil construction contractors are expected to improve, underpinned by revenue growth and gross margin expansion. CTD’s revenue is projected to increase by 24% YoY, with gross margin expanding by 0.4ppt, resulting in net profit growth of 83% YoY. By contrast, VCG’s net profit is projected to decline 56% YoY, mainly due to the absence of divestment gains, despite stable core operations.

BOT operators (CII, HHV) are expected to benefit from new awards, notably the Trung Luong–My Thuan (Phase 2) project, supporting backlog expansion and construction revenue growth. CII’s net profit is projected to increase by 70% YoY from a low 2025 base, driven by revenue growth and margin expansion amid stable BOT operations. Meanwhile, HHV’s net profit is expected to rise modestly by 5% YoY, supported by the completion of the Dong Dang–Tra Linh project and a 10% YoY increase in BOT traffic volume.

Investment strategy

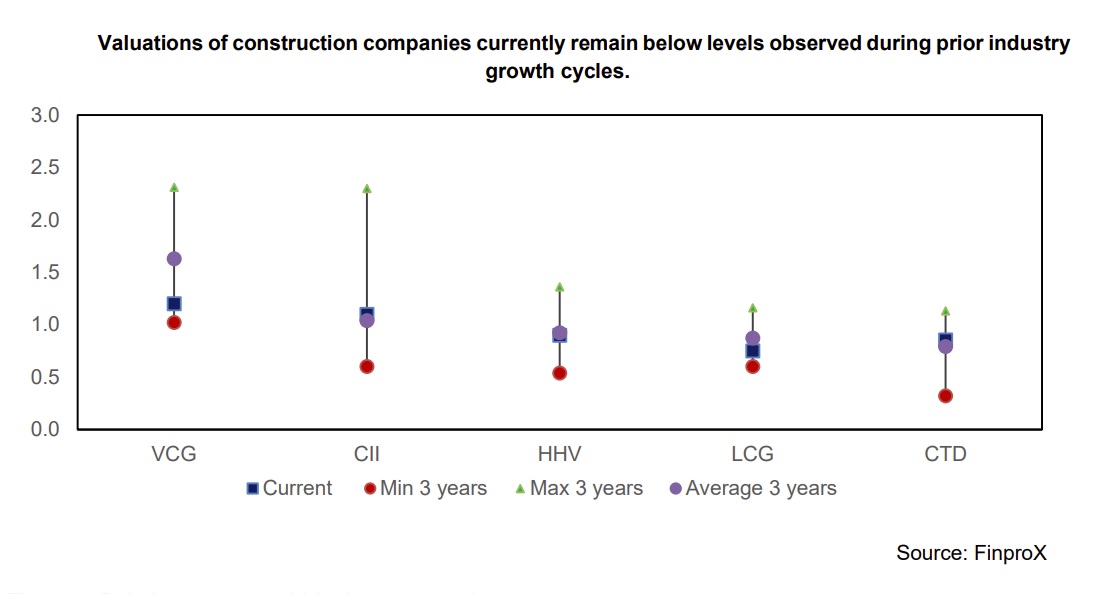

MBS maintained a positive outlook on CTD, CII, and HHV. First, CTD is expected to benefit significantly from the recovery of the construction sector, supported by civil construction and public investment. FY2026 backlog is projected to increase by 40% YoY to VND 63bn, driven by partnerships with major developers. Gross margin is expected to recover by 0.4ppt YoY, supported by a more favorable project pipeline and mitigation measures against input cost pressures. A recovery in the real estate market is likely to limit bad debt recognition in 2026–27, thereby supporting projected net profit growth of 83% YoY. The stock is currently trading at a P/B of 0.9x, below the 1.1x level observed during prior construction recovery cycles. MBS raised its target price by 4% (vs. our report dated 30/09/2025), supported by a stronger backlog and improved gross margins, to VND 97,500 per share.

Second, CII’s net profit is projected to grow 70% YoY in 2026, driven by construction from the Trung Luong–My Thuan BOT project. MBS expects earnings to accelerate further from 2028, supported by this BOT. Real estate: CII is awaiting approval for 9.6ha in Thu Thiem to finalize land-use payments; a decision is expected in Q3 2026 amid accelerated land pricing. Upcoming Q2 land auctions may support asset revaluation. The stock is trading at a P/B of 0.9x, below the 1.2x level seen during growth periods. MBS set a target price of VND 24,000 per share.

Third, continued to benefit from public investment growth, with backlog projected to increase by 8% YoY. VCG’s FY2026 net profit is projected to decline by 40% YoY, reflecting a high base in 2025 driven by project divestment gains. We will reassess VCG’s valuation upon resolution of legal issues related to VIW’s land bank. The current P/B of 1.2x is considered appropriate within the growth cycle. MBS maintained its target price of VND 26,400 per share (unchanged from our report dated 26/05/2025), supported by stable operating performance.

Fourth, HHV’s FY2026 net profit is projected to grow 6% YoY, supported by the BOT segment amid a 10% YoY increase in traffic volume. The construction segment is also underpinned by projects such as Trung Luong–My Thuan and Dong Dang–Tra Linh. The current P/B of 0.8x remains below the 1.0x level typically observed during growth periods.

Author: NGOC ANH

RECOMMENDED TOPICS