VN

VN

EN

EN

26/07/2026, 02:00

Investment

What outlook for 2Q25 earnings of listed companies?

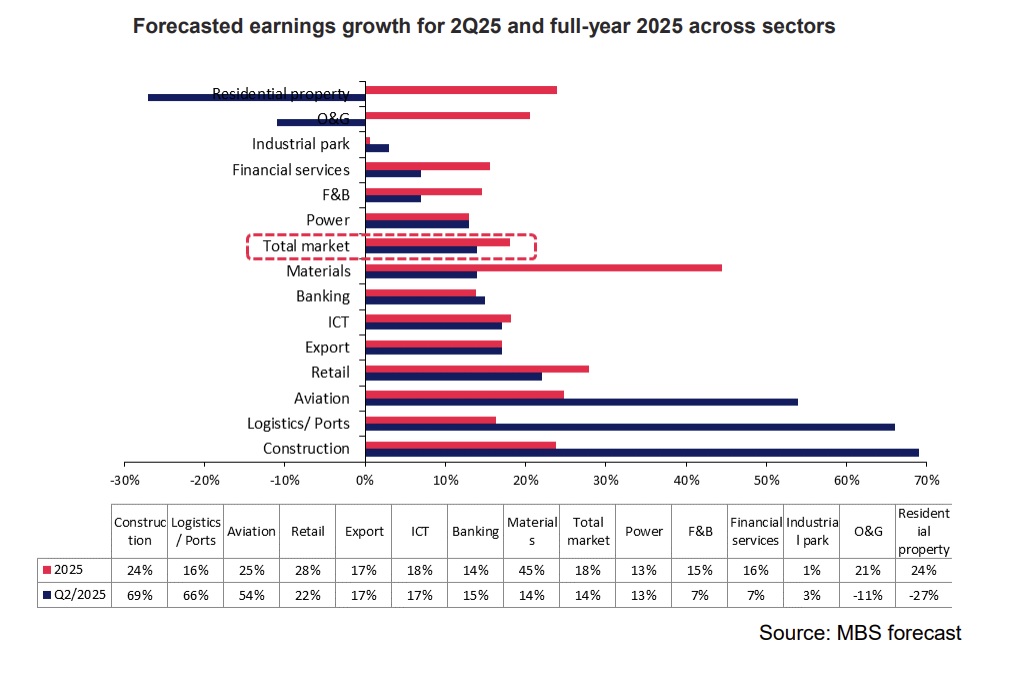

Earnings of listed companies on the Vietnam stock market could grow by 14% YoY in 2Q25, despite ongoing pressures from geopolitical tensions and tariff-related trade wars, according to MBS.

Banking sector earnings could improve

In 2Q25, credit growth accelerated, reaching 6.99% YTD as of June 16, significantly higher than the 3.75% in the same period last year. This was driven by a low interest rate environment and accommodative monetary policy supporting the 8% GDP growth target. Joint-stock commercial banks (e.g., MSB, EIB, VPB, SHB, CTG) led the expansion, backed by robust corporate loan demand and attractive funding costs.

Net interest margin (NIM) is expected to remain stable QoQ as lending rates hold steady while deposit rates may ease slightly on strong deposit growth (5.09% YTD vs. 0.92% in 2024), reducing competition for capital. Listed commercial banks’ net profit is forecast to grow 14.7% YoY in Q2, improving from 11.0% in Q1. Key beneficiaries include VPB, CTG, and EIB, supported by strong credit momentum and resilient NIMs.

On the policy side, Decree 69/2025/ND-CP raises foreign ownership caps to 49% for banks under mandatory restructuring (e.g., VPB, MBB, HDB), enhancing capitalraising potential though not yet urgent given high CARs. Meanwhile, the draft law institutionalizing Resolution 42 is expected to improve NPL resolution, benefiting banks with high provisioning needs such as CTG, VPB, and smaller banks like OCB, MSB, and VIB.

Real estate earnings to show breakthrough

In the first half of 2025, Hanoi’s real estate market exhibited clear segmentation: the low-rise segment experienced positive growth in both supply and absorption, while the high-rise segment slowed due to a concentration of supply in the eastern area. In Ho Chi Minh City, Q1/2025 apartment supply dropped 36% YoY as developers limited new launches, although the absorption rate remained high thanks to sustained demand.

For landed property, supply increased slightly, but the absorption rate was only 53% as selling prices remained elevated. Moving into 2Q25, the market has shown more positive signals: FDI into real estate surged, accounting for 25.9% of total registered capital; the legal framework has been further completed; and many major projects have been approved (such as Aqua City, Subdivision C4 in Dong Nai, and 148 projects in Hanoi).

In addition, discussions about provincial mergers have fueled expectations for infrastructure development and real estate growth. However, Q2 earnings of residential real estate developers are not expected to show significant improvement, due to the limited number of handovers. MBS believes the outlook for real estate developers will improve in the second half of 2025, supported by a pipeline of projects expected to be delivered during this period.

Industrial park sector to await trade talks

According to the General Statistics Office (Ministry of Finance), Vietnam attracted USD 18.39 billion in total registered FDI during the first five months of 2025, up 51.2% YoY. However, newly registered capital declined by 13.2% YoY to USD 7.02 billion, reflecting investor caution amid tariff-related policy risks and the fact that new investors are waiting for the outcome of trade negotiations between Vietnam and the U.S.

In 2Q25, MBS believes earnings of industrial real estate developers primarily stem from MOUs signed prior to the U.S. announcement of retaliatory tariff policies. We forecast flat earnings growth for BCM, IDC, and SZC, while KBC is expected to post a 59% YoY profit increase, driven by land lease revenue from Goertek, which will be recognized this quarter. It maintains a cautious outlook on the earnings prospects of industrial real estate companies in the upcoming quarters.

Domestic market drives steel sector

In 2Q25, domestic steel consumption is expected to surge by 22% YoY, reaching approximately 7.1 million tons, driven mainly by public investment disbursement and a recovery in the real estate sector. Construction steel consumption is forecast to reach 3.1 million tons (14% YoY), with Hòa Phát (HPG) likely increasing output by 15% YoY.

For hot-rolled coil (HRC), the temporary antidumping duties of 19–28% have narrowed the price gap between Chinese and Vietnamese HRC to just USD 50/ton, making local HRC more competitive. HPG reported that the share of domestic HRC used in galvanized steel production rose from 15–20% to 40%. Benefiting from the Dung Quat 2 plant and favorable tariff policies, HPG's HRC output in Q2 could reach 2.2 million tons (40% YoY).

On the flip side, total industry export volume is projected to fall 20% YoY to 1.5 million tons due to anti-dumping tariffs imposed by the EU and U.S., adding pressure on exporters. Domestic steel prices remained stable thanks to strong demand and supportive policies. Construction steel prices were flat YoY, up slightly 1% QoQ.

Meanwhile, input material costs declined — iron ore down 3% and coal down 4% YoY due to oversupply from Australia and Brazil. “This supports margin expansion for producers like HPG and galvanizers like HSG, which may reverse provisions. With falling input costs and steady selling prices, industry-wide gross margins are expected to improve notably in 2Q25”, said MBS.

Oil & gas earnings diverge across segments

Oil and gas companies are expected to report improved earnings versus Q1/2025; however, oil price volatility and a high base in Q2/2024 will likely lead to mixed results across segments. In the upstream segment, PVD is projected to post positive results as the PVD VI rig resumed operations in Malaysia on April 26, 2025, and maintenance costs incurred in Q1 are no longer present. Day rates for jack-up rigs also saw a slight increase in the first two months of the quarter. PVD VIII is expected to start operations in Vietnam from Q3/2025 and thus will not impact Q2 results. PVS continues to execute the Block B project and deliver the Greater Changhua offshore wind substructure, but profits remain concentrated in port logistics and oil vessel services. M&C margins improved only marginally, and no one-off gains like in Q1 are expected.

In the midstream segment, GAS is likely to show better results than Q1 thanks to stronger gasfired power demand during the dry season and potential provision reversals if the new electricity pricing framework is approved. However, lower average oilprices YoY could compress gas selling prices and margins. PVT may see a slight YoY decline due to weaker freight rates for crude and refined oil, partially offset by Binh Son Refinery’s lack of maintenance shutdowns this year.

In the downstream segment, BSR faces a high comparison base from last year and narrower crack spreads due to subdued global demand, leading to YoY profit decline. However, in MBS’s opinion, geopolitical tensions in late Q2 may lift crack spreads and improve results compared to Q1. PLX benefited from higher oil prices during the quarter via improved fuel trading margins, though Q2 earnings may still fall YoY due to the high base in 2024.

Hydropower outperforms, evolving regulatory landscape

In 2Q25, electricity consumption grew slowly, rising only around 1% YoY in April– May, well below the full-year target of 11%. Although total installed capacity increased modestly (1.8%), power shortage risks remain limited ahead of Q3. EVN raised electricity prices by 4.8% in May, supporting the sector’s financial health and encouraging power dispatch and investment. Hydropower output surged by 35% YoY in the first five months, thanks to a low base last year and heavy rainfall in Central Vietnam—benefiting operators such as REE and HDG.

In contrast, coal and gas power generation declined slightly, pressured by lower spot electricity prices and weak demand. Imported coal prices dropped 14% YoY, but mixed-coal prices fell less sharply, limiting margin recovery for coalfired power producers. Gas-fired power continues to face challenges from gas shortages and high LNG prices; however, POW and NT2 benefit from high contracted output (Qc) and stable gas supply. Renewable energy (RE) generation remained stable, with technical risks easing and dispatch priority maintained.

“A highlight in Q2 was the issuance of new RE pricing policies, notably with onshore and nearshore wind power tariffs rising by 17% and 8%, respectively over the transitional rates—attractive enough for new investment. However, solar power remains cautious, as pricing improvements are still limited. Some firms, such as REE and GEG, have shown interest in floating solar projects”, said MBS.

Modern retail expands

In the first five months of 2025, retail and consumer services revenue (excluding price factors) rose 7.4% YoY, outpacing the 2024 average and the same period last year (5.4%), signaling a clearer recovery in domestic consumption. This creates favorable conditions for essential goods retail chains to expand. In May, the implementation of mandatory e-invoicing and removal of lump-sum tax policies impacted small household businesses, promoting transaction transparency and reducing unfair competition for modern retail chains. In 2Q25, the modern retail sector continued to grow, adding approximately 620 new stores (11% YTD), especially in the Central region.

However, MBS notes expansion costs may slow net profit growth, likely keeping it flat YoY. The pharmaceutical sector saw mixed results: Long Châu remained the leader with 155 new stores (8%), reaching an estimated 2,100 pharmacies (23% YoY) and sustained profit growth through scale and product transparency. An Khang narrowed losses thanks to product portfolio restructuring. The ICT-CE (consumer electronics) segment remained stable in store count, but sales per store rose 13% YoY due to price recovery and slightly improved demand.

Conversely, the jewelry segment faced continued challenges from high material costs and weak demand. However, gross margin improvements are expected to keep net profit flat YoY. The draft amendment to Decree 24/2012 and plans to reopen gold import quotas after 13 years are positive signals for PNJ, DOJI, with potential upside for earnings in upcoming quarters if approved.

Logistics & ports benefits from US tariffs

In 2Q25, this sector broadly benefited from vibrant trade activity, supported by the 90-day postponement of new tariff measures. Vietnam’s total import-export turnover in the first five months rose 15.7% YoY, with exports to the U.S. surging 28.6% YoY. As a result, container throughput at ports in Ba Ria – Vung Tau is expected to rise significantly, as 50–55% of export volume in this region is bound for the U.S.—supporting earnings growth for port operators such as GMD. Global sea freight rates rebounded strongly, up approximately 70.7% from the earlyApril bottom.

Additionally, charter rates for vessels sized 1,700–1,800 TEUs increased by about 7% QoQ and 37% YoY in 2Q25, driving strong revenue growth for shipping companies like HAH…

Author: Thanh Liem

RECOMMENDED TOPICS