VN

VN

EN

EN

22/07/2026, 02:38

Investment

What outlook for CRT?

1Q26 net profit of Viettel Construction JSC (HSX: CTR) increased 23% YoY, supported by construction and solar installation activities, offsetting slower growth in new BTS tower deployments.

CTR benefits from the ongoing 5G rollout, supported by a stable workload from its parent company, Viettel.

CTR benefits from the ongoing 5G rollout, supported by a stable workload from its parent company, Viettel. The peak phase of tower deployment has largely passed, with the company planning to add only 1,000 BTS sites in 2026 and an average of 500 sites per year during 2027–30, depending on demand.

Going forward, MBS expects greater focus on margin expansion through improved operations and increased tower sharing. This trend is already evident, with the tenancy ratio improving to 1.04x in 1Q26 (from 1.03x at end-2025). It forecasts this to reach 1.043x in 2026 and 1.087x by 2030.

As workloads from the parent company gradually decline, CTR is diversifying beyond the group, transitioning from a telecom-focused company into a construction contractor, with a strong push into turnkey housing solutions (including construction, M&E, rooftop solar installation, and smart home IoT solutions).

Within a short period, CTR has demonstrated strong execution capability, gaining a leading position in the B2C residential construction and rooftop solar segments, with a surge in backlog growth since 2H25. Going forward, the company will continue to complete its contractor service ecosystem and expand further into B2B construction, including public investment projects. MBS views this as a key new growth driver, with revenue projected to deliver 30% CAGR during 2026–2028.

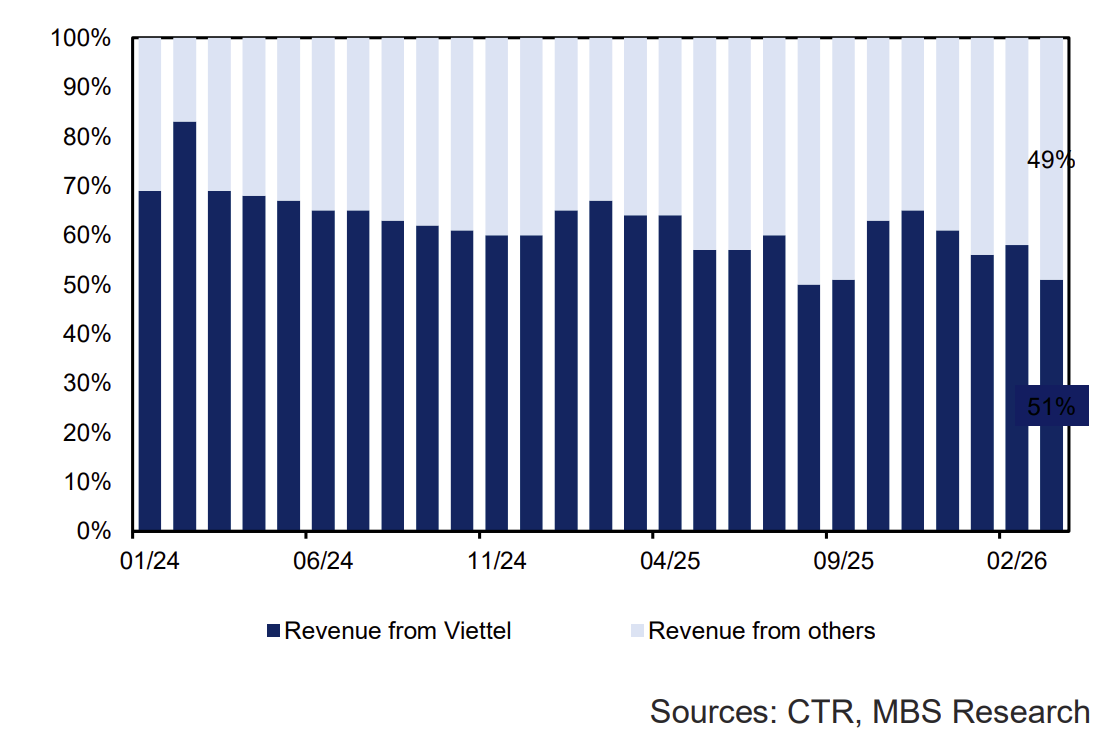

Revenue from outside Viettel increased significantly, from 30% in 2024 to 49% in 1Q26, highlighting efforts to diversify revenue through civil construction and rooftop solar installation.

Following a significant correction from its peak, CTR is currently trading at EV/EBITDA (7.3x) and P/E (16.4x), near the bottom of its 2-year range and below the sector average, while maintaining sustainable ROE levels. MBS believes CTR offers an attractive risk-reward profile, with limited downside risk and improving growth prospects driven by its construction contractor expansion strategy.

“We revise our target price downward by 4% compared with the previous estimate, mainly due to a reduction in medium-term earnings growth (2027–30) from 19% CAGR to 17% CAGR, reflecting a more cautious view on TowerCo segment growth, while construction activities remain cyclical and less sustainable. Currently, CTR is trading at 16.4x P/E, near the bottom of its 2-year average, indicating an attractive valuation with limited downside risk. Our valuation is based on a blended approach between DCF and EV/EBITDA with equal weighting," said MBS.

DCF valuation (10-year horizon) with assumptions: WACC 13.5%, cost of equity 14.7%, and terminal growth rate 0%. MBS considers this method appropriate given CTR’s integrated business model and relatively stable cash flows. MBS views EV/EBITDA as suitable because (1) companies are capital-intensive, with significant fixed asset investments; and (2) stable cash flows, with EBITDA excluding non-cash items, allowing a clearer assessment of operating performance rather than capital structure effects.

Factors supporting CTR’s upside include stronger-than-expected 5G demand, driving higher infrastructure deployment and tower leasing demand; better-than-expected gross margins in the construction and integrated solutions segments; expansion into new business areas, including a 50MW wind project in Quang Tri and initial entry into social housing development (targeting 50,000 units by 2030).

However, this company also faces downside risks: a slower-than-expected increase in tenancy ratio in the TowerCo segment, affecting infrastructure leasing earnings growth, a prolonged slowdown in the real estate market following tighter government credit policies, which may lead to weaker-than-expected project pipeline growth.

Author: NGOC ANH

RECOMMENDED TOPICS