VN

VN

EN

EN

16/07/2026, 02:38

Investment

Will credit flow into lower-risk real estate?

Providing bank loans to the real estate sector through a classification-based lending approach could help limit risks and improve loan quality.

Capital flows can be directed toward priority areas that form the foundation of the market and meet genuine housing demand

By classifying and identifying strategic segments while “ring-fencing” speculative activities, capital flows can be directed toward priority areas that form the foundation of the market and meet genuine housing demand, healthy investment needs, and social welfare objectives.

Real Estate Capital “Barrier”

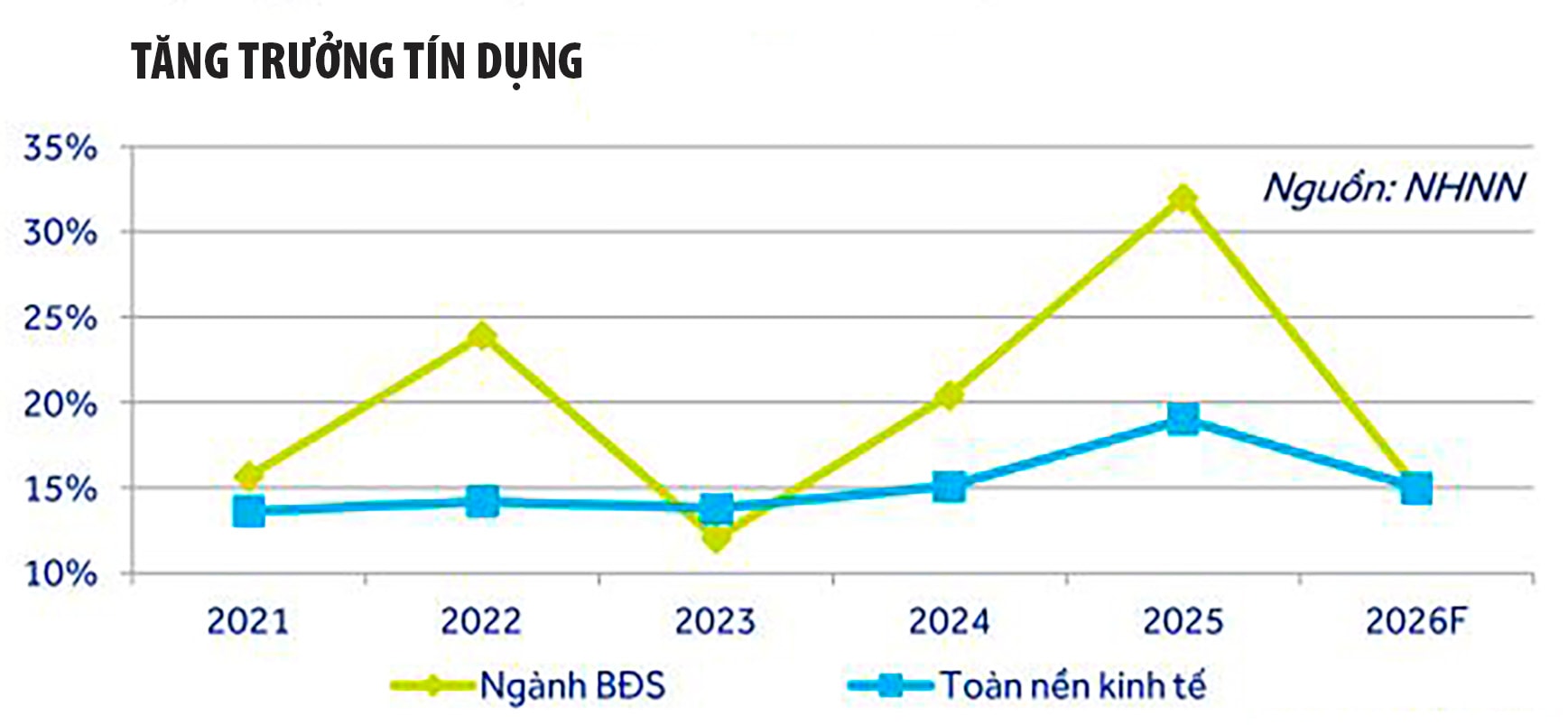

As of the end of March 2026, according to statistics from the State Bank of Vietnam, total outstanding credit across the banking system exceeded VND 19.18 quadrillion, up 3.18% compared to the end of 2025. Meanwhile, according to a report from the Ministry of Construction of Vietnam, as of 28 February 2026, total outstanding credit serving real estate business activities reached approximately VND 2.235 quadrillion, up 11.7% compared to the fourth quarter of 2025 and as much as 43% year-on-year.

In the first quarter, the State Bank directed banks to control credit growth so that it would not exceed 25% of their annual assigned quota, in order to ensure system safety and avoid overheating. At the same time, real estate lending was not allowed to exceed each bank’s overall credit growth rate compared to the end of 2025. Business results at the end of the first quarter showed that major banks were holding millions of billions of dong worth of collateral assets securing loans, led by the Big Four banking group and two private banks with large ecosystems, Techcombank and VPBank.

During the first quarter, the market also witnessed spikes in interest rates and the possibility of a “shutdown” in real estate lending as some banks exhausted their lending room under regulatory requirements. Real estate loan interest rates, especially floating rates, also rose to 12–14% per year at many banks, creating a major “barrier” for homebuyers seeking access to credit.

At the same time, this became a “bottleneck” for capital flows into real estate segments tied to genuine demand and lower speculative activity, causing real estate credit to decline in some areas such as Ho Chi Minh City and limiting the leverage effect of capital flows into important segments such as industrial parks, affordable commercial housing, and social housing. As a foundational sector linked to more than 40 industries in the economy, according to Mr. Lê Hoàng Châu, Chairman of the Ho Chi Minh City Real Estate Association, these bottlenecks are hindering the sector’s recovery and ability to accelerate strongly enough to contribute to the double-digit growth targets of both the real estate market and the wider economy.

Unlocking High-Quality Capital Flows

At a working session with the State Bank on banking operations in the first months of 2026 and key tasks going forward, Prime Minister Lê Minh Hưng instructed the State Bank to urgently study and propose amendments to legal regulations related to extending credit beyond lending limits for strategic and nationally significant projects. This would be tied to increasing the responsibility of credit institutions in controlling credit quality and evaluating project effectiveness. At the same time, authorities were instructed to carefully calculate, control, and closely supervise lending to potentially risky sectors, including studying the classification of different real estate categories in order to establish appropriate credit limits and encourage the development of social housing and industrial parks.

Classifying credit for the real estate sector could help limit risks and improve loan quality.

Regarding the task of classifying real estate categories as a basis for capital allocation, experts believe this is the correct and necessary policy direction, aligned with the practical shift from administrative-command management toward modern risk management under Basel II and Basel III standards, which the banking sector is pursuing. Through classification that identifies strategic segments and “contains” speculation, capital flows can be redirected toward priority sectors that support genuine housing demand, healthy investment, and social welfare. At the same time, this could help control inflated property valuations used for borrowing, thereby curbing asset inflation and making capital flows into real estate more effective and less overheated.

Classification linked to lending is already being applied by the State Bank through risk-weight coefficients for different segments. However, if implemented in greater depth and detail, it could have a stronger effect in regulating market behavior. In this context, policy acts as a filtering mechanism, forcing developers to shift from a “debt-intensive” model toward a more “equity-intensive” model focused on real demand.

However, to effectively implement the assigned tasks, Dr. Đinh Thế Hiển, a financial expert, believes that strict and thorough enforcement of policy, along with the elimination of vested-interest groups, is the “master key.” In practice, Mr. Hiển noted, the banking sector has a Bankruptcy Law but does not apply it. Regulations on capital scale, sectoral credit allocation, and Basel II and III standards have all been established, yet supervision and enforcement still need to be strengthened, from the oversight and internal control capacity of individual credit institutions to system-wide supervisory capacity. This is necessary to ensure that capital flows into the intended sectors, prevent “virtual capital,” and avoid asset price inflation that artificially drives up market prices and undermines asset quality.

Overall, the policy of classifying credit limits is an inevitable step toward “cleaning up” the monetary market and redirecting capital toward the “real” economy instead of allowing it to circulate endlessly in speculative asset cycles. However, its success will depend heavily on the State Bank’s real-world supervisory capacity and close coordination with fiscal policy.

Author: LE MY - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS