VN

VN

EN

EN

09/07/2026, 11:15

Investment

Capital costs rise to meet bond maturity pressures

The pressure of corporate bond maturities remains immense. Statistics show that 42.2 trillion VND will mature in Q2/2026, followed by another 73.3 trillion VND in Q3/2026, heavily concentrated in the real estate sector.

Statistics from the Vietnam Bond Market Association (VBMA) indicate that in May 2026, bond issuances continued to recover slightly compared to the previous month, though they saw a significant drop compared to the same period last year.

The Government issued Decree No. 200/2026/ND-CP dated June 5, 2026, regulating the private placement and trading of corporate bonds in the domestic market, as well as the offering of corporate bonds to the international market. Effective from the date of signing, the decree enhances the responsibilities of issuing enterprises. This new regulation is expected to impact the market starting from the end of the second quarter. (Illustrative photo)

Corporate Bonds Experience Slight Recovery

Banking and real estate continue to be the two leading sectors driving primary issuance activity. However, the banking sector far outpaced real estate in terms of capital mobilization needs over the past month.

Specifically, as of May 29, 2026, the market recorded 29 private corporate bond placements with a total value of 36,263 billion VND, alongside 3,999 billion VND raised through 4 public offerings.

Consequently, total corporate bond issuance in May 2026 reached 40,262 billion VND, marking a 21.46% increase compared to the previous month but a 42% decline compared to the same period last year.

Cumulatively for the first 5 months of the year, the total value of corporate bond issuances exceeded 127,300 billion VND. Of this, private placements accounted for 107,018 billion VND, while public offerings contributed 20,333 billion VND.

As mentioned above, commercial banks and real estate enterprises continue to play the dominant role in corporate bond issuance activities. Specifically, the banking sector accounted for approximately 48% of the total issuance value, while real estate enterprises contributed about 44% of the total issuance scale (predominantly driven by companies within the Vingroup ecosystem).

While the banking group commanded up to 70% of the total market issuance in May 2025, this share has now declined to 48%. Conversely, the issuance proportion of the real estate group doubled compared to the same period last year, rising from 22% to around 44%. Nevertheless, this group still ranked behind banks in terms of mobilization volume for the month.

In the first 5 months of this year, real estate bond issuance surpassed 56,000 billion VND, a 2.1-fold increase compared to the volume issued during the same period last year (26,500 billion VND).

Regarding extraordinary disclosures, May recorded 2 bond codes with delayed principal and interest payments, amounting to 125 billion VND in principal and nearly 88 billion VND in interest.

VBMA also noted that in May, businesses bought back 19,780 billion VND worth of bonds ahead of maturity, down 9% compared to the same period in 2025.

Substantial Maturity Pressure Ahead

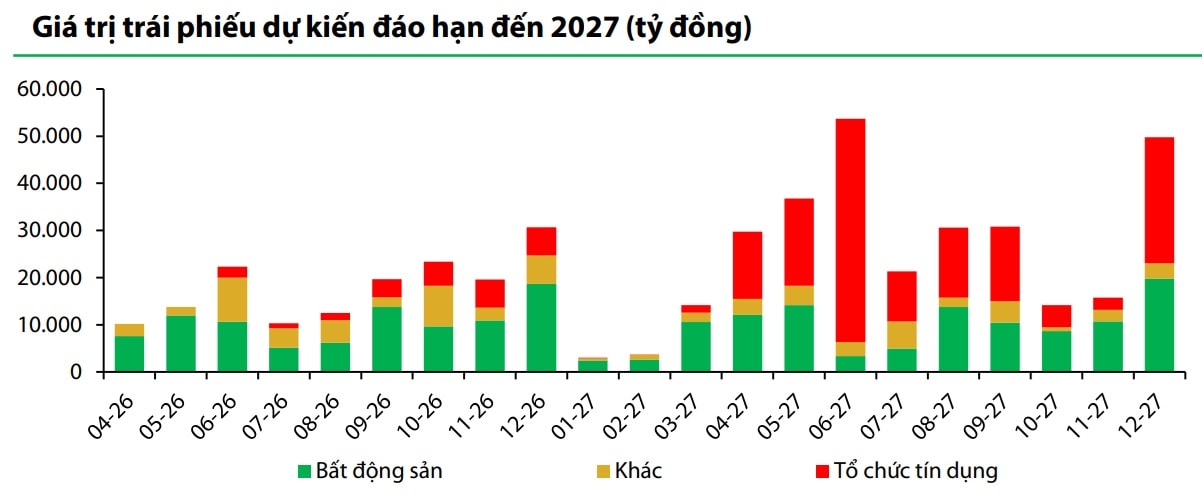

In the remaining 7 months of 2026, the estimated maturity value stands at 141,908 billion VND.

Breaking it down by quarter, data from Rong Viet Securities (VDSC) shows that 42.2 trillion VND worth of corporate bonds are due to mature in Q2/2026. Moving into Q3, the volume of corporate bonds reaching maturity will climb to 73.3 trillion VND, concentrated heavily in the real estate sector.

This demands that issuers proactively balance their cash flows or negotiate with bondholders to handle debt obligations in the coming period, VDSC noted.

Analysts point out that if businesses face difficulties in restructuring cash flows or issuing new bonds, capital pressure could flow back into the banking system through new loan demands.

Data also shows that the cost of capital is rising and may not cool down immediately. According to VBMA, Vinhomes led the market in May 2026 with an issuance interest rate of 12.5%, while the issuance costs for commercial banks also rose sharply compared to the same period last year (8.3% - 8.6% per annum).

This rising cost of capital comes amid shifting benchmark interest rates. At the end of Q1/2026, issuance interest rates increased compared to the previous quarter in two main categories: credit institutions (up 67.8 basis points) and real estate (up 40.0 basis points), VDSC concluded.

In the secondary market, average bond yields (YTM) recorded corresponding movements, reflecting investor expectations regarding interest rates and the necessary risk premium ahead of liquidity pressures in near-term maturities.

However, experts noted that the level of impact varies across the board. For projects with solid legal frameworks backed by reputable, highly-rated enterprises, negotiating lower interest rate margins or tiered interest structures will still offer a cost-of-capital advantage compared to current bank loan rates.

Author: LE MY - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS