VN

VN

EN

EN

26/07/2026, 11:20

Investment

Listed real estate firms hard to see breakthrough profits

The beginning of the year is typically not a peak handover period for real estate projects. As a result, profits of listed real estate companies in Q1 2026 are unlikely to see significant breakthroughs.

.jpg)

Higher interest rates combined with restricted credit for the real estate sector have made developers more cautious in launching new projects.

In the first quarter of 2026, the real estate market in general—and real estate stocks in particular—remained relatively subdued, largely due to the impact of persistently high and rising interest rates.

According to MBS Securities, higher interest rates combined with restricted credit for the real estate sector have made developers more cautious in launching new projects, while also increasing financial pressure on ongoing developments.

At the same time, homebuyer demand has slowed, particularly among speculative buyers or those relying on high financial leverage. Weak market liquidity has led to slight price corrections in some segments during Q1 2026. Data from Batdongsan.com.vn shows that land prices in Hanoi fell 4% compared to the end of 2025, while housing prices in Ho Chi Minh City declined by 2%.

Nevertheless, MBS noted several positive factors offsetting the impact of higher interest rates. First, legal frameworks for projects are becoming more complete and transparent, with new regulations issued to resolve longstanding legal bottlenecks in the real estate sector.

Second, progress in public investment projects is improving the outlook for property values in surrounding areas.

Third, signals from the State Bank of Vietnam to stabilize interest rates may help maintain monetary stability and prevent further rate hikes in the near term.

Fourth, expectations surrounding Dong Nai potentially becoming Vietnam’s seventh centrally governed city could boost infrastructure development and attract investment, thereby increasing property values.

Regarding earnings outlooks, MBS noted that companies expected to post strong profit growth typically benefit from one-off factors—such as bulk sales of project units or financial gains from divestments. Meanwhile, most other firms are projected to report flat or slightly declining profits year-on-year.

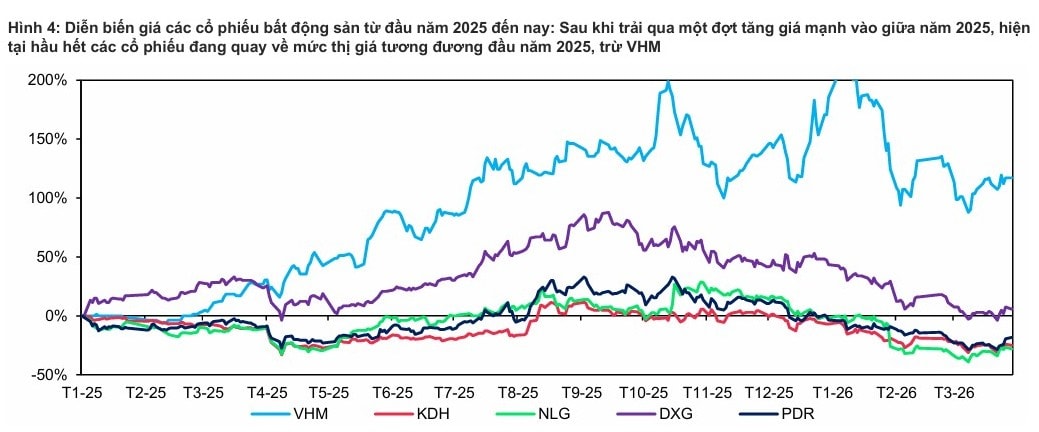

Given that early-year quarters are not peak handover periods, MBS does not expect significant profit breakthroughs in Q1 2026. However, a notable point is that real estate stocks are currently trading at valuations below their five-year average and median levels, reflecting the sector’s sensitivity to interest rate movements.

“With expectations that interest rates may stabilize in the near term and improve market liquidity—particularly in the end-user segment—we believe some real estate stocks are now worth accumulating for long-term investment, notably NLG, KDH, and PDR,” MBS said.

The firm also provided earnings forecasts for several key residential real estate developers:

For VHM, MBS expects strong net profit growth in Q1 2026 from a low base in the same period last year, driven by a major transfer deal at Green Paradise (estimated value of around VND 50 trillion, accounting for about 15% of the project’s area). However, sales volumes may decline due to high mortgage interest rates.

For DXG, Q1 2026 is unlikely to see major breakthroughs as the company still relies heavily on brokerage activities and has not yet recorded large-scale project handovers. That said, the company is expected to recognize some high-margin brokerage contracts, along with modest financial gains from divesting its stake in Dat Xanh Mien Nam.

For KDH, early-year profits will mainly come from handing over low-rise units previously sold at the Gladia by the Waters project, improving from a low base last year. However, remaining products are higher-value units that require longer decision-making from buyers, further affected by rising interest rates and seasonal disruptions from the Lunar New Year.

For NLG, Q1 2026 will continue to see handovers of land plots at the Nam Long II Central Lake project in Can Tho, as well as low-rise units at Waterpoint and Izumi City (phase 1A1), which will serve as the main profit drivers. While handovers at Izumi are expected to proceed smoothly, volumes remain limited, and handovers at Nam Long Can Tho depend heavily on sales progress. Overall, profits are likely to remain flat compared to last year’s low base.

For PDR, the company has signed a deal to transfer its stake in Thien Long High-Rise Investment and Development Real Estate JSC (owner of the Thuan An 1 project) and received the first payment of VND 1.9 trillion. Financial gains from this transaction are expected to be the main profit driver in Q1 2026.

Author: DINH DAI - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS