VN

VN

EN

EN

26/07/2026, 11:20

Investment

Outlook for 1Q26 earnings

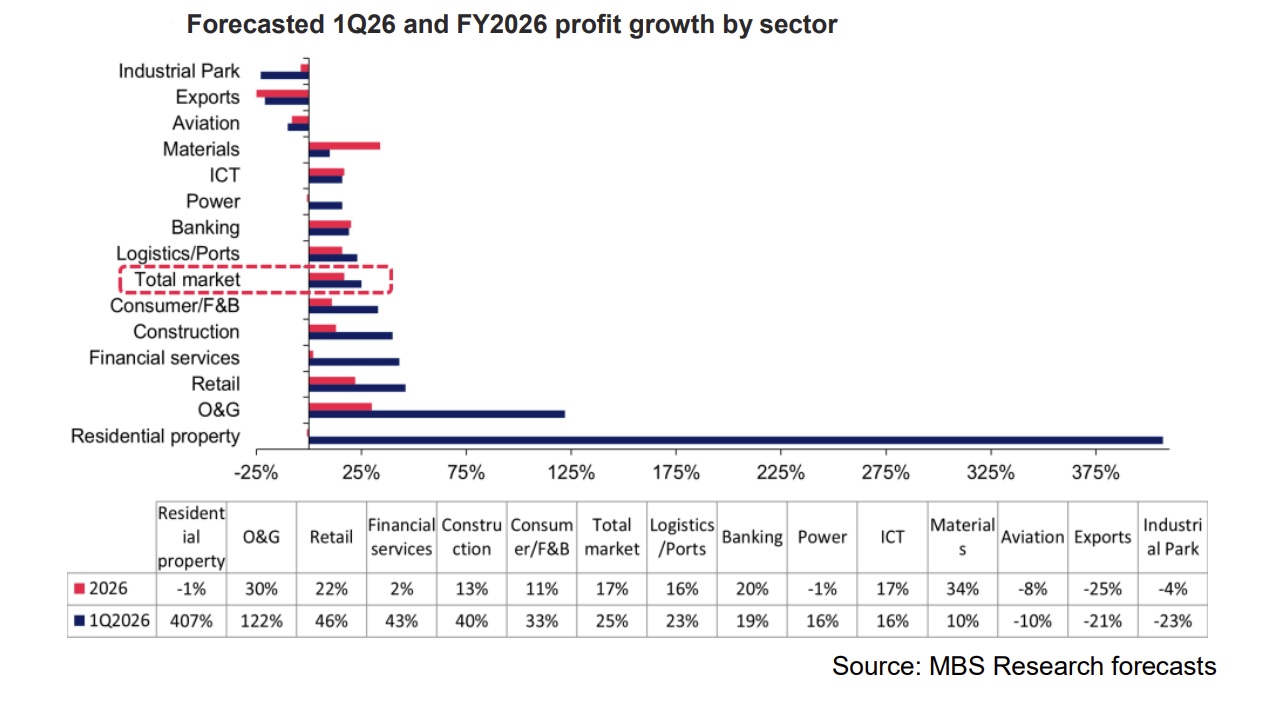

In 1Q26, MBS estimated that earnings across the overall market would post strong yoy growth of approximately 25%. However, this growth is unlikely to be broad-based, with gains concentrated in only a few sectors or companies benefiting from exceptional factors.

MBS estimates that net profit after tax of the listed banks under our coverage will increase by approximately 19% yoy in 1Q2026

Banking: Positive earnings growth

MBS estimates that net profit after tax of the listed banks under our coverage will increase by approximately 19% yoy in 1Q2026, supported by: (i) industry-wide credit growth of around 3%, with banks receiving compulsory transfers expected to post stronger credit growth as they are not subject to lending growth caps in the first quarter of 2026; (ii) a modest recovery in NIM, driven by higher lending rates, while deposit rates, although increasing, have not risen strongly enough to outpace credit growth; (iii) provisioning expenses among banks under our coverage are expected to increase by 30.1% yoy.

Joint-stock commercial banks may record a higher increase of 47.2% yoy due to weaker asset quality in 2025 and the lingering impact of Decree 86/2024. Bank valuations have corrected to levels below their one-year average, while earnings growth prospects remain favorable.

Residential property: Strong earnings driven by bulk sales

The real estate market remained subdued in 1Q26, mainly due to persistently high and rising interest rates. Higher rates, combined with tighter credit conditions for the property sector, have resulted in: (1) developers to be more cautious in deploying new projects while facing financial pressure on ongoing ones; (2) a slowdown in homebuyer absorption, particularly among speculative buyers or those using high leverage. Weak market liquidity led to modest price corrections in several property segments during 1Q26.

According to batdongsan.com.vn, land plot prices in Hanoi declined by 4% compared with end-2025, while housing prices in Ho Chi Minh City fell by 2%. The market recorded some positive points to offset the impact of rising interest rates, including: (1) project legal procedures have become more transparent and complete, with several new regulations helping resolve legal bottlenecks in the real estate sector; (2) news that Dong Nai may become a centrally governed city has created expectations for stronger infrastructure investment and capital inflows.

Among listed property developers, companies expected to post strong profit growth generally benefit from one-off factors such as bulk project sales or financial gains from selling project stakes. Most other developers are forecast to report flat or slightly lower earnings yoy.

Industrial park: Long-term outlook remains positive

Q1 earnings are weak due to timing of land handover FDI into the manufacturing and processing sector remained strong in the first two months of 2026. Realized FDI and newly registered FDI increased by 10% and 82% yoy, respectively. Export and import activities of FDI enterprises also recorded robust growth, with export and import value rising by 30% and 42% yoy. The industrial park market has shown signs of recovery, especially in readybuilt factory and warehouse leasing.

Notably, in 1Q26, many new policies to attract domestic and foreign investment into high-tech fields have opened a new stage of development for the industry, such as Decree 20/2026 on private economic development and the draft Resolution on foreign investment economics currently under consideration. MBS believes these policies will directly stimulate demand for industrial parks and accelerate the transformation from traditional industrial parks to eco-industrial and high-tech parks.

For listed industrial park enterprises, MBS believes that large developers such as BCM, KBC, and IDC will benefit greatly from these policies. However, 1Q2026 earnings will remain highly dependent on the timing of land handovers. KBC and SZC may see profits decline from last year’s high base, while BCM and IDC could still achieve profit growth of 8% and 18% yoy, respectively.

Construction materials: Earnings supported by recovery in steel prices

In 1Q26, consumption of construction steel and HRC by domestic enterprises is forecasted to grow by 12%/30% yoy thanks to positive demand growth as civil construction and public investment accelerate; in FY2026, construction steel and HRC output is projected to increase by 10%/31% yoy. Steel prices also saw a recovery in 1Q26 with increases of 4%/3% compared to the beginning of the year for construction steel and HRC, respectively.

MBS forecasts that in FY2026, construction steel and HRC prices will recover by 6%/5% yoy, while galvanized steel prices will recover by 4% yoy. Despite a slight decrease in raw material prices, due to DQ2 depreciation, MBS assesses that HPG's gross margin will remain stable yoy at 14.2%. For galvanized steel enterprises, the upward trend of HRC while galvanized steel prices remain flat could cause the gross margins of HSG and NKG to decrease by 1.2 percentage points and 1 percentage point yoy, respectively. Thanks to increased revenue and stable gross margins, HPG's net profit is forecasted to increase by 13% yoy, reaching 3,800 billion VND. Meanwhile, galvanized steel enterprises like HSG and NKG, due to reduced gross margins and export difficulties, recorded decreases of 17% and 38% yoy.

Oil & Gas: Benefiting from oil price volatility

A high oil price environment is supportive across the entire oil & gas value chain. In the upstream segment, higher oil and condensate prices improve investment efficiency, encourage FID decisions, and boost demand and pricing for oilfield services. PVS benefits from its large M&C backlog, especially the EPCI progress of Block B, with expected profits of 480 billion VND. PVD is expected to post 86% yoy earnings growth thanks to re-signed rig contracts at higher day rates and contributions from partner rigs.

In the midstream, PVT operates mainly in domestic and Southeast Asian markets, thus facing less direct impact from Middle East bottlenecks; rising freight rates provide support, but the benefit is limited as it does not own VLCC vessels, with profits estimated to increase by 19% yoy. GAS encountered LPG supply disruptions starting in early March, causing a slight dip in late-quarter output; however, LPG prices doubling and LNG nearly tripling helped improve selling prices. While profit margins faced input cost pressure, they were partially offset by high LPG premiums, with profits estimated at 3,174 billion VND (15% yoy).

In the downstream, BSR maintained production in Q1 and benefited significantly from recovering crack spreads, with profits estimated at 4,217 billion VND (957% yoy). PLX was supported by rising domestic petroleum price levels, with profits expected to reach 286 billion VND (114% yoy).

Power: LNG prices as tailwinds for renewable energy

Total electricity output in 1Q26 is estimated to increase by 7.1% yoy, broadly in line with the National System and Market Operator target of 7.5%. Hydropower generation is expected to rise slightly yoy. According to the National Center for Hydro-Meteorological Forecasting, nationwide rainfall is generally expected to remain around the long-term average, with only some areas in Central Vietnam recording above-average rainfall.

MBS expects Ha Do Group and REE Corporation to record modest yoy earnings growth. Gas-fired power generation is expected to improve by 17% yoy from last year’s low base, with plants using gas from Southeast Vietnam, such as Phu My and Nhon Trach 1&2, showing a clear recovery. In 1Q2026, additional output from Nhon Trach 3&4 will also be recognized. Domestic gas prices remained around USD8.5-9/mmbtu in the first two months of 2026, but are likely to increase again from March due to the sharp rise in global oil prices.

Meanwhile, the Japan Korea Marker (JKM), the benchmark LNG price in Asia, has nearly doubled since the start of the year and is currently trading at around USD20/mmbtu, putting upward pressure on gasfired electricity prices. However, plants assigned a high contracted output (Qc), such as Nhon Trach 1&2, should still maintain favorable dispatch prospects and gross margins.

Accordingly, MBS estimates that earnings of Nhon Trach 2 Power JSC will recover strongly from last year’s low base, while Petrovietnam Power Corporation is likely to remain broadly flat due to pressure from Nhon Trach 3&4. For coal-fired power producers, dispatch is expected to remain broadly flat yoy in 1Q2026, while the electricity market price has remained stable at around VND1,100/kWh.

As a result, MBS estimates that gross margins will see limited changes. Earnings of coal-fired plants should improve further during the peak summer season in 2Q-3Q2026. Regarding policy, the Ministry of Industry and Trade approved the adjustments to the Power Development Plan for the 2021- 30 period in March. Key highlights include increasing the proportion of renewable energy, raising peak emission commitments (to support slowing down the coal power phase-out process), and adjustments aimed at balancing the feasibility of energy planning to serve double-digit economic growth. This is particularly crucial amid volatile LNG price risks and domestic oil and gas extraction potential declining faster than expected, which could impact energy security. Accordingly, better mechanisms are expected to promote renewable energy in the coming time.

Consumer retail: Modern retail expands while jewelry retail surges

In the first 2 months, total retail sales of goods and consumer service revenue increased by 7.9% yoy - significantly lower than the 9.3% rate of the same period last year. Excluding price effects, real growth was only 4.5%, the lowest since May 2024. Within this, retail sales of goods increased by 7.8% yoy. Overall, general consumer demand remains quite slow, and prices of essential products have increased due to pressure from input costs (transportation, production). Within the essential consumer goods: The dairy sector is recovering from a low base thanks to tighter control of smuggled milk and improved distribution systems among major companies. Stable raw material costs are also supporting high gross margins, leading us to expect double-digit net profit growth in 1Q2026.

Within retail, essential retail models (WCM, Bach Hoa Xanh) are benefiting from a strong shift in transactions from traditional trade. They continue their aggressive scale expansion, particularly in the Central and Northern regions, with total stores estimated to increase by 360 (10% compared to the end of 2025); net profit is expected to grow steadily through cost optimization in new areas.

The pharmaceutical retail industry continues to record scale growth across major chains: Long Chau, Pharmacity, and An Khang in existing regions. Consumer electronics maintain a stable scale, with revenue per store growing 20% yoy, while consumption demand shows single-digit yoy growth. The jewelry industry is capitalizing on high gold price volatility, leading to a high probability of double-digit yoy growth in price levels. Investment gold products are being sold significantly more due to rising customer demand and the restored supply capacity from manufacturers. As a result, jewelry retailers may deliver a significant earnings breakout in 1Q2026.

Transportation & Logistics: Rising fuel costs begin to pressure margins

MBS believes the 1Q2026 earnings outlook for the logistics sector remains broadly positive, although higher fuel prices will create downside risk for margins. In the first two months of 2026, container throughput at Vietnamese ports is estimated to have increased by 18.2% yoy, mainly driven by efforts to diversify export markets. For postal and express delivery services, parcel volume is expected to continue growing strongly, supported by 7.9% yoy growth in retail sales during the first two months of the year, stronger spending during the Lunar New Year period, and continued rapid expansion of e-commerce.

However, cost pressure is intensifying as Brent oil prices have risen sharply since early March. This will directly erode gross margins for transportation and logistics companies such as HAH and VTP. By contrast, port operators such as GMD, which have lower fuel cost exposure and already raised service prices earlier this year, are expected to be less affected and should maintain earnings growth thanks to strong cargo throughput.

Author: NGOC ANH

RECOMMENDED TOPICS