VN

VN

EN

EN

26/07/2026, 11:20

Investment

VHC to face many challenges

As a major pangasius exporter to the U.S. market, Vinh Hoan Corporation (HoSE: VHC) continues to face pressure from large, high-priced inventories and increasingly intense competition. This is the challenge VHC must address to maintain its growth momentum in 2025.

High Inventory Levels

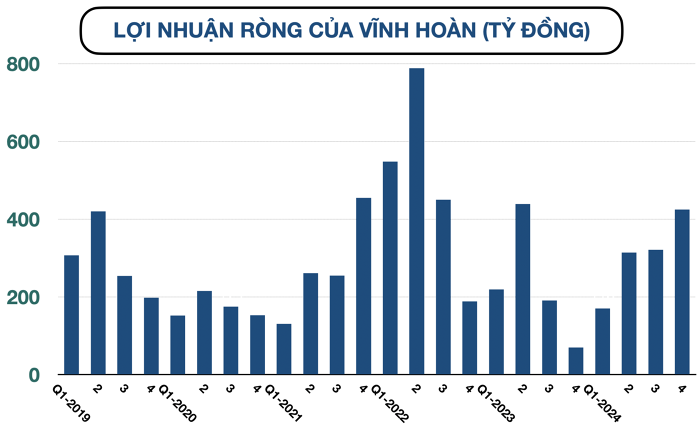

According to VASEP, the current price of commercial pangasius hovers around VND 32,000–33,000/kg for fish weighing one kilogram or more, allowing farmers to turn a profit. These attractive profit margins encourage farmers to expand their farming areas. As a result, VHC’s business performance improved, with revenue in 2024 growing by 24.9% to reach VND 12,535 billion, and net profit surging by 34.6% to VND 1,310 billion.

Despite favorable business results, VHC’s 2024 financial statements show that at the end of 2024, the company’s inventory was valued at nearly VND 3,000 billion, accounting for 23.8% of total assets. This means that VHC held an average of 126 days of inventory at the time. From 2017 to 2022, VHC’s average inventory ranged from 67.3 to 94.1 days—about three months’ worth—to serve production and business needs. Thus, the inventory at the end of 2024 was high compared to previous years, and it was also high-priced inventory, as VHC procured and stockpiled raw materials in the final months of 2024.

The U.S. market has been VHC’s largest export destination for pangasius for many years, contributing about 43.8% of the company’s total export revenue, followed by the EU market at 23.5% and China at 13.9%. Currently, VHC focuses on producing fingerlings and juvenile fish through Vinh Hoan Hatchery Co., Ltd., while also expanding its own farming areas, covering about 70% of its raw material needs. This strategy helps ensure a stable supply of raw materials for processing and exporting pangasius, yet the company remains vulnerable if exports drop significantly again—especially since it has not fully liquidated its existing high-priced inventory from the previous period.

According to VASEP, Vietnam’s pangasius exports to the U.S. in 2024 reached USD 345 million, an increase of 27% compared to 2023. VHC continued to lead market share in exports to the U.S., at 46%. In the first two months of this year, VASEP data shows Vietnam’s pangasius export value at over USD 253 million, down 0.8% year-on-year. In February 2025 alone, Vietnam’s pangasius exports reached more than USD 120 million, a 32.8% increase compared to the same period last year. The fluctuating U.S. tariff policies appear to be the primary cause of the large inventory pressure on pangasius exporters like VHC.

Competitive Pressures

Industry analysts predict that 2025 will present both opportunities and challenges for Vietnam’s pangasius sector. The pangasius industry is known for high cyclicality, typically lasting one to two years. When pangasius prices rise, it stimulates farmers to increase production, which can lead to oversupply and a subsequent price decline.

On the demand side, the U.S. is currently moving to end the Russia-Ukraine conflict quickly, potentially lifting its ban on Russian seafood exports—including cod and pollock. This could create added pressure on Vietnam’s pangasius exports, as pangasius has been the American alternative to Russian cod and pollock ever since the ban on Russian seafood exports took effect.

Ms. Nguyen Ha Minh Anh, an analyst at Bao Viet Securities (BVSC), noted that the U.S. currently imposes a 0–3% tariff on Vietnamese pangasius products (excluding anti-dumping and countervailing duties), whereas Vietnam imposes a 15–30% tariff on similar U.S. products. If the U.S. were to impose reciprocal tariffs of 15–30% on Vietnamese pangasius, its price competitiveness would drop, and consumer demand in the U.S. would likely decline, impacting VHC’s largest market.

Opportunities amid Challenges

VASEP forecasts that Vietnam’s seafood exports may exceed USD 10 billion by 2025. As an industry leader, VHC will likely see more opportunities than challenges—particularly in the U.S. market, where it enjoys distinct advantages, although the company may face difficulties in Hong Kong and China.

Additionally, many experts predict pangasius production will continue to rise in 2025, with pangasius seen as a substitute for tilapia in the U.S. due to its stable and usually lower price, especially if tariffs on tilapia increase. This presents favorable conditions for VHC.

Moreover, on January 17, 2025, in the U.S., the governments of Vietnam and the U.S. reached a bilateral agreement to end the disputes in case DS536 at the World Trade Organization (WTO). Under this agreement, VHC is the only company exempt from the scope of anti-dumping duties on pangasius and basa exports to the U.S. This decision will allow VHC greater access to the U.S. market without the threat of anti-dumping tariffs.

However, challenges remain. Pangasius prices in China are expected to continue declining due to competition with tilapia and other fish. In particular, because China faces tariffs from the U.S., it may reduce its demand for Vietnamese pangasius imports, potentially causing VHC’s exports to China to drop.

Author: PHUONG HA - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS