VN

VN

EN

EN

15/07/2026, 10:39

Investment

What prospects for Vietnam’s 87 securities firms?

Vietnam currently has 87 licensed securities firms offering a broad range of services, including brokerage, investment advisory, financial services (margin lending), investment banking and proprietary trading.

Four groups of securities firms

According to S&I Ratings, securities firms in Viet Nam can be divided into four strategic groups based on ownership models, each carrying distinct credit profiles and risk characteristics.

The first group consists of securities firms within banking ecosystems, including VCBS, MBS, TCX, VPX, ACBS, Kafi, HDBS, BSI, CTS, SHS, OCBS, LPBS and TPS. These firms benefit from competitive funding costs, cross-selling opportunities and access to existing customer bases. Their key risk factor is closely tied to the health of their parent banks.

The second group includes securities firms affiliated with major conglomerates, such as FTS and VI. Their advantage lies in aligning with broader group strategies, while risk exposure varies depending on the parent group’s business profile.

The third group comprises foreign securities firms such as Mirae Asset, KIS, Maybank, Shinhan, Yuanta, Pinetree, KB and JB. These companies benefit from technology, low-fee structures and access to foreign investor networks. However, their market share is often concentrated in narrower segments and influenced by capital allocation policies from overseas parent companies.

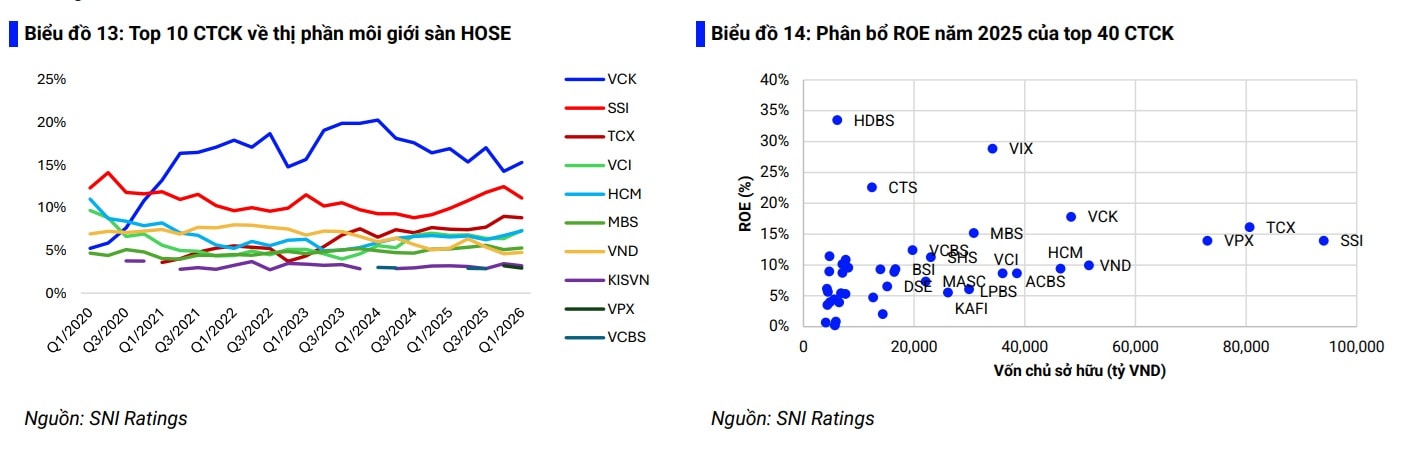

The final group includes independent securities firms — or firms effectively controlled by related shareholder groups that together form broader financial ecosystems — such as SSI, HCM, VCI, VND, VCK, VDS and DSE. According to S&I Ratings, these firms benefit from strategic flexibility and diversified services, although their access to capital remains more dependent on market conditions.

S&I Ratings noted that even within this “independent” category, firms such as SSI, VCI and VND have effectively evolved into large financial ecosystems. These firms are increasingly active in securing syndicated international loans worth tens of millions of US dollars, helping them obtain long-term funding at competitive costs and strengthen their market positions. However, not all independent firms possess this level of capital access.

Industry credit outlook

In its 2026 outlook report on Viet Nam’s securities sector, S&I Ratings maintained a “Stable” assessment while acknowledging that the outlook could gradually shift toward “Positive” if firms effectively manage risks.

The agency said the sector entered 2026 with significantly strengthened capital foundations built during 2023–2025, alongside sweeping legal reforms and the expected FTSE market upgrade scheduled to take effect in September 2026.

Notably, Viet Nam is undergoing what S&I Ratings described as the most comprehensive legal and infrastructure reform cycle in the 25-year history of its stock market. For the first time, the legal framework has been revised simultaneously across all three regulatory layers — laws, decrees and circulars — focusing on three strategic objectives:

- Upgrading Viet Nam from a frontier market to a secondary emerging market;

- Shifting regulatory focus from procedural control toward investor protection and market discipline;

- Preparing the legal infrastructure for next-generation financial products.

The agency described this as an unprecedented effort reflecting the Government’s determination to align Viet Nam’s capital markets with international standards and strengthen their role as a medium- and long-term funding channel for the economy.

At the same time, a new legal framework for next-generation financial products is emerging. Resolution 05/2025/NQ-CP launched a five-year pilot programme for digital asset markets from September 9, 2025, formally bringing crypto assets under a controlled regulatory framework for the first time. Circular 32/2026/TT-BTC also introduced tax policies for digital asset transactions.

In addition, the Law on the Digital Technology Industry 71/2025/QH15 and Decree 232/2025/ND-CP removed the state monopoly on gold bars, opening opportunities for securities firms to expand into new services such as token brokerage, digital asset custody and gold trading. However, firms will also face rising costs related to IT systems, AML/CFT compliance and competition from specialized fintech platforms.

S&I Ratings expects the sector’s short- and long-term credit outlooks to diverge. Over the long term, the new legal framework is viewed positively as it could improve market quality, broaden the investor base and diversify products and services. In the short term, however, securities firms will need to increase spending on IT systems, staff training, risk management upgrades and capital adequacy requirements, potentially weighing on profit margins.

“Credit differentiation will continue to widen between leading securities firms that clearly benefit from these reforms and smaller firms with high leverage and dependence on a narrow range of activities,” S&I Ratings said.

The race to raise capital

To meet market demand and maintain competitiveness as smaller firms face mounting pressure, S&I Ratings expects 2026 to become an active year for capital raising across the securities industry. This trend is being driven by three simultaneous pressures.

First, Decree 245/2025/ND-CP officially lifted foreign ownership limits in securities firms to 100%, removing one of the biggest barriers to strategic foreign investment.

Second, many leading securities firms are approaching the regulatory ceiling for margin lending relative to equity capital — including HCM at 194%, KBSV at 188%, MBS at 182%, MASC at 177% and VCBS at 176% — forcing them to raise additional capital to expand lending capacity.

Third, Circular 102/2025/TT-BTC increased risk coefficients by 10%–30%, making additional regulatory capital increasingly necessary.

As a result, many securities firms have announced aggressive capital-raising plans to support ambitious business expansion strategies.

SSI leads the sector with plans to raise approximately VND 9.262 trillion in 2026, potentially lifting its charter capital above VND 30 trillion by year-end. If completed, SSI could become the first securities firm in Viet Nam to surpass this threshold. Its fundraising plans include preferential offerings, ESOP issuance and share sales to existing shareholders.

VIX Securities plans to raise around VND 9.189 trillion through a rights offering, increasing its charter capital to more than VND 24.5 trillion. VCK targets a VND 9.131 trillion increase, mainly through retained earnings capitalization, while TCX plans to raise around VND 4.628 trillion to lift its charter capital to nearly VND 27.8 trillion.

S&I Ratings expects three main fundraising channels to dominate in 2026: (i) rights offerings to existing shareholders; (ii) private placements to foreign strategic investors; and (iii) long-term bond issuance to improve funding maturity structures, which currently remain heavily skewed toward short-term funding.

Meanwhile, several mid-sized firms such as Kafi, HDBS and OCBS are preparing IPO plans following the successful listings of larger firms including TCX, VCK and VPX in 2025.

Total capital raised across the industry in 2026 is estimated to remain at a high level comparable to 2025, at roughly VND 100 trillion. While this wave of capital raising is viewed positively in the long run due to stronger capital buffers and more diversified funding sources, S&I Ratings cautioned that investors should closely monitor dilution risks and the effectiveness of capital deployment.

Author: LE MY - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS