VN

VN

EN

EN

26/07/2026, 02:38

Business economics

Will deposit rates continue to ease by year-end?

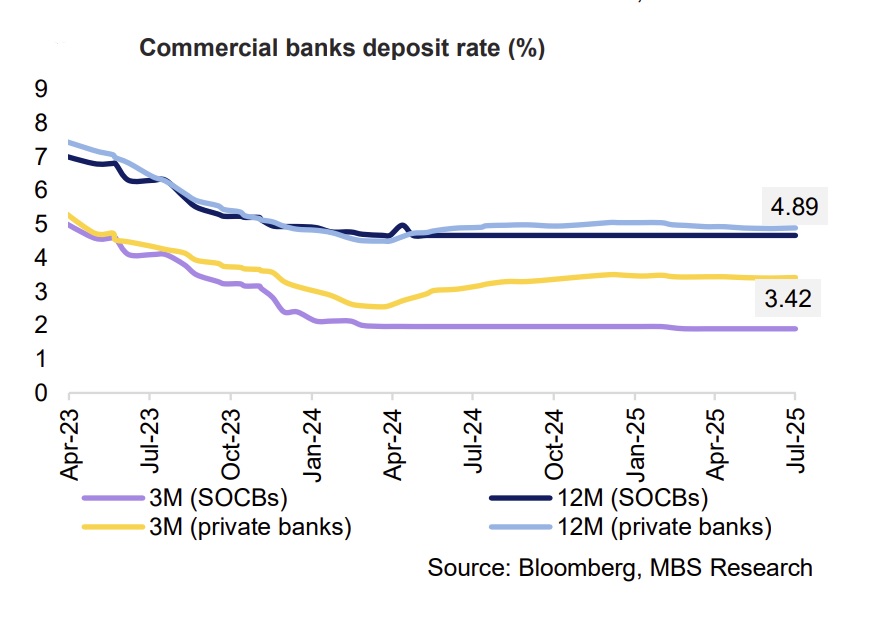

MBS anticipates that the average 12-month deposit rates of large commercial banks will have room to decrease slightly by 2 bps, easing to 4.7% by the end of 2025.

Transactions at MB

Following the SBV’s strong net injection in June, the overnight interbank interest rate dropped significantly by 3.4% from the end of June to 3.5% in early July. However, since then, interbank rates have steadily risen through the end of the month, even peaking at a one-month high of 6.2% on July 25. This signals liquidity pressure despite the SBV's efforts to conduct net injections during the month.

Specifically, the SBV ceased issuing treasury bills from July 17. During the month, the SBV issued nearly VND 45.8 trillion in treasury bills with interest rates of 3.4% - 3.5% and a 7-day tenor. Concurrently, the SBV significantly increased the scale of capital injection through the OMO channel, reaching over VND 426.4 trillion (more than three times the previous month) at a 4% interest rate for tenors ranging from 7 to 91 days. The total matured OMO capital and T-bills were approximately VND 362.8 trillion and VND 68.3 trillion, respectively.

Cumulatively, the SBV conducted a net injection valued at nearly VND 86.2 trillion. By the end of the month, the overnight rate cooled significantly to 3.1%. Meanwhile, rates for tenors ranging from one week to one month fluctuated between 3.7% and 4.6%.

After stabilizing in June, the deposit interest rate level showed a slight upward trend in July. Among the banks we monitored, three banks - TPB, VPB, and EIB - slightly increased their deposit interest rates by 0.1% - 0.2% per year for tenors ranging from 1 to 36 months. This development occurred amid robust credit growth in recent times.

According to the SBV, as of July 29, credit growth has increased by 9.8% compared to the end of 2024 and by 19.8% yoy. We estimate that credit growth outpaced deposit growth by approximately 1.3 - 1.5 times. Consequently, this has exerted some upward pressure on deposit interest rates among private commercial banks to attract deposits. By the end of July, the average 12-month deposit rate at commercial banks increased slightly by 2 bps compared to June and decreased by 16 bps from the beginning of 2025, reaching 4.89%, while the rate for state-owned banks remained steady at 4.7%.

Toward year-end, deposit rates may face pressure from credit growth, particularly following the SBV’s announcement of increased credit growth quotas for banks to meet the economy’s capital needs. However, the SBV also requested credit institutions to implement comprehensive measures to stabilize and strive to reduce deposit interest rates, contributing to stabilizing the money market and creating room to lower lending interest rates. This, combined with the expectation of a 50 bps interest rate cut by the FED in the second half of 2025, will help narrow the VND-USD interest rate gap and create room for the SBV to maintain a low interest rate environment. Based on these factors, MBS anticipates that the average 12-month deposit rates of large commercial banks will have room to decrease slightly by 2 bps, easing to 4.7% by the end of 2025.

Author: NGOC ANH

RECOMMENDED TOPICS