VN

VN

EN

EN

22/07/2026, 02:38

Investment

How the Middle East conflict impacts the Vietnamese stock and gold markets

According to market strategists, gold prices are poised to surge this week toward the resistance range of $5,429–$5,734 per ounce, while global equity markets may decline by 1–2% or more.

Gold is expected to open the week with a “gap up” due to elevated geopolitical risk.

Market reactions are unfolding as investors assess escalating tensions in the Middle East ahead of trading sessions. Analysts warn that the conflict could significantly disrupt oil supply and price dynamics, with spillover effects on gold, equities and other asset classes.

Oil Prices Set to “Boil”

Mr. Trần Hoàng Sơn, Market Strategy Director at VPBankS, noted that Iran’s crude production currently stands at 3.3 million barrels per day (bpd), of which 1.5 million bpd are exported—mostly to China. About 86% of Iran’s output is onshore, concentrated in the southwest Khuzistan region near the Iraqi border.

Should supply from Iran be disrupted, the immediate impact may be manageable, as OPEC members have pledged to raise output if needed. Saudi Arabia alone could offset Iran’s exports within weeks or months.

The United States remains the world’s largest oil producer, and global reliance on Iranian crude is relatively limited. Even China maintains diversified supply sources. On Sunday, OPEC agreed to increase production by 206,000 bpd starting in April—a modest increment representing less than 0.2% of global demand.

However, the closure of the Strait of Hormuz presents a far more consequential risk. The strait handles approximately 20–22% of global oil supply—equivalent to 20–21 million bpd—as well as significant volumes of LNG from Saudi Arabia, Iraq, the UAE, Kuwait, Qatar and Iran. Tanker and LNG traffic through the strait has nearly halted.

Shipping data early Sunday showed only a few vessels exiting the strait, with none entering. Iran issued VHF radio warnings prohibiting passage and confirmed attacks on tankers defying restrictions. Several energy firms and trading houses have suspended shipments along the route.

Roughly three-quarters of oil transported via Hormuz is destined for China, India, Japan and South Korea. China alone sources about 50% of its crude imports through this corridor.

Analysts caution that even short-lived restrictions could sharply reduce supply. Oil prices could spike by $10–$50 per barrel—or more—with worst-case projections ranging from $90 to $150 per barrel.

Global retail fuel prices, including in Vietnam, would likely rise, adding inflationary pressure. Brent crude surged 10% to around $80 per barrel in OTC trading Sunday.

As of the morning session on March 2, Brent was up 4.5% at $76.07 per barrel, briefly exceeding $82. U.S. crude gained 3.9% to $69.59 per barrel.

“If the U.S. deploys naval forces to reopen the strait as expected, disruptions may be short-lived,” Sơn said. “But if escalation continues—such as Iranian attacks on Gulf oil infrastructure—global supply losses of 10–20% could push prices above $130–$200 per barrel under extreme scenarios.”

Oil Shock and CPI Risks

Maybank Investment Banking Group (MIBG) outlines two scenarios:

- Base case: If Iran’s retaliation remains contained and political transitions occur swiftly, oil markets may experience only a temporary shock. Brent could spike 10–15% before stabilizing as supply concerns ease. Early signals suggest muted risk-off sentiment: Bitcoin initially dropped but quickly recovered to trade sideways, reflecting resilient investor confidence.

- Bearish case: Escalation and sustained disruption at Hormuz remain the primary risk. Such an outcome could drive crude above $100 per barrel, reigniting inflationary pressures and triggering broad-based risk asset sell-offs. However, this scenario is deemed lower probability given China’s heavy reliance on Hormuz transit and its vested interest in preventing prolonged disruption.

Data show that oil price volatility directly affects Vietnam’s CPI. MIBG estimates that in a severe disruption scenario, an oil price shock could add 3.1 percentage points to Vietnam’s headline inflation.

Sensitivity analysis indicates:

- Minor disruption (10% oil): 0.5 percentage points to CPI

- Moderate disruption (30% oil): 1.5 percentage points

- Major disruption (60% oil): 3.1 percentage points

- “Black swan” event (100% oil): 5.1 percentage points

Nonetheless, analysts expect any conflict-related supply disruptions to be short-term. With abundant domestic food supply and flexible policy management, Vietnam’s inflation risk is considered manageable.

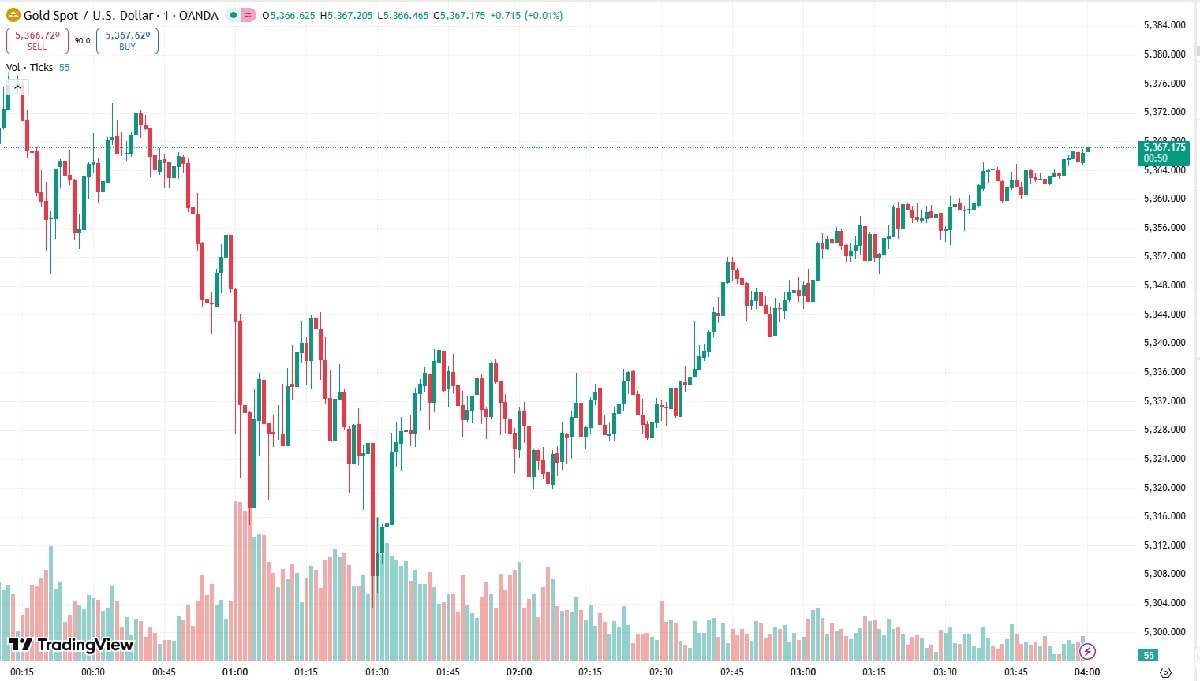

Gold surged nearly 2% immediately after the attack and has climbed roughly 22% in the first two months of 2026—the strongest start since 2012—reflecting heightened safe-haven demand, according to VPBankS.

As of 10:00 a.m. (GMT7) on March 2, spot gold was up 1.64% at approximately $5,365.6 per ounce. Analysts forecast continued momentum toward the $5,429–$5,734 resistance zone this week.

Vietnamese Stocks Face Limited Direct Impact

Global equity markets are shifting into risk-off mode, potentially dragging major indices such as the S&P 500, Nasdaq and Dow Jones down by 1–2% or more. Airlines, logistics and financial stocks may face pressure, while defense and energy shares outperform.

Historically, major military conflicts tend to cause temporary market pullbacks driven by oil price concerns and geopolitical risk. Markets typically rebound quickly if the conflict remains contained.

The VN-Index has historically been less sensitive than the S&P 500, with short-term reactions lasting one to two sessions unless indirect effects materialize through oil prices or global macro conditions. Middle East tensions have typically shaved 0.5–2% off the S&P 500 before swift recovery within one to two weeks.

The Russia–Ukraine war in 2022 marked the most severe and prolonged downturn due to surging oil prices and global inflation. Vietnam’s market reaction has generally been muted—usually under 1%—except for April 13, 2024, when Iran’s attack on Israel triggered stronger declines amid FX pressure and foreign net selling.

For the week of March 2–6, 2026, Sơn expects short-term volatility if U.S.–Israel–Iran tensions escalate. The VN-Index, currently near its historic peak of 1,900–1,920 points, may experience corrective pullbacks toward 1,850–1,870—or deeper to 1,800–1,830—if selling pressure intensifies, particularly from foreign investors.

However, declines are likely to be limited and short-lived if the conflict does not persist. Vietnam’s market has minimal direct exposure to Iranian oil and reacts primarily through sentiment and capital flows.

Beneficiary sectors include:

- Oil & Gas / Energy: GAS, BSR, PVS, PVD, PVC, OIL, PLX

- Petrochemical-related fertilizers: DPM, DCM, BFC, CSV

- Ports & Logistics: GMD, PVT, HAH

These sectors tend to benefit from higher oil prices, improved margins, and stronger upstream and infrastructure activity.

Conversely, inflation-sensitive sectors such as consumer goods, manufacturing and road transport may face headwinds if retail fuel prices rise sharply.

As of 11:00 a.m., the VN-Index remained in positive territory, up approximately 0.15% and holding above 1,880 points, despite 252 decliners across the board. Oil and gas stocks continued to hit their upper trading limits.

Author: LE MY - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS