VN

VN

EN

EN

10/07/2026, 02:38

Business economics

Interest rates may fall further in 2H26

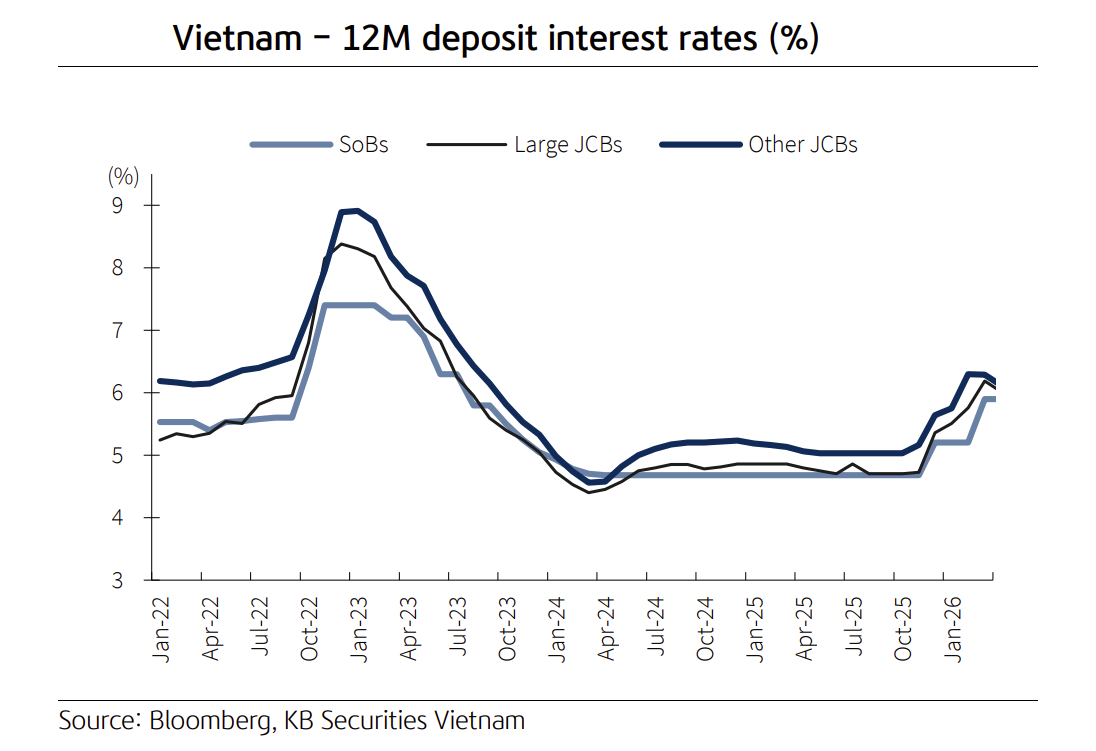

Interest rates peaked at the beginning of 2Q26, but a steeper fall is projected for 2H26, according to the KBSV.

Transactions at Seabank

Pressures on interest rates in 1Q

1Q26 interest rates extended the increases from the previous quarter. After the banking system's liquidity shortage at the end of 4Q25 due to slow deposit growth, the pressure partly eased in 2026 thanks to improved public investment disbursement in the last few weeks of 2025, the rebound of FDI and remittances, and the cooling of the exchange rate, giving the SBV more room to loosen the money supply (the amount of outstanding OMOs at the end of January dropped to VMD240 trillion at times).

However, this state did not last long, as the market still experienced localized tensions at certain times (especially before the Lunar New Year and at the beginning and end of March, when cash shortages caused interbank overnight interest rates to surge above 10%). In KBSV’s view, there are two main reasons for this: (1) The demand for cash in circulation increased amid the impact of tax policies, and (2) a large amount of capital is tied up in the state budget as public investment disbursement shows signs of slowing down. In addition, the high demand for cash before Tet from people, or banks having to prepare cash to meet CAR at the end of the quarter, also put pressure on system liquidity.

The coordinated injection and withdrawal through the OMO channel, combined with the use of foreign exchange swap operations by the SBV quickly helped to cool down interbank interest rates during these periods.

Entering 1Q26, the deposit and lending interest rates of commercial banks extended their uptrend. The average 12M deposit interest rate of commercial banks increased by 71bps compared to the end of 2025, with state-owned banks making one adjustment of 70bps and large private commercial banks also recording an increase of approximately 100-110bps. The average medium and long-term lending interest rate of commercial banks as of the end of February 2026 also increased by 40bps compared to the average of December 2025, reaching 7.1-9.4% (according to the SBV).

After the meeting between the SBV and commercial banks on monetary policy management held on the afternoon of April 9, 2026, with the goal of lowering interest rates to address the competition in capital mobilization and reduce real lending rates, many commercial banks have lowered their deposit interest rates. Accordingly, deposit interest rates of state-owned banks such as Vietcombank (VCB), VietinBank (CTG), and Agribank (AGR) recorded a decrease of 50 bps for terms of 24 months or more. Private commercial banks such as Techcombank (TCB), Military Bank (MBB), VPBank (VPB), Southeast Asia Commercial Bank (SSB), and An Binh Commercial Bank (ABB) also took similar action, reducing deposit interest rates mainly for medium and long-term terms, with a decrease of about 30-50 bps.

Outlook for 2026 interest rates

After the meeting on April 9, 2026, interest rates in 2Q are likely to see a slight decrease from their high levels after commercial banks agreed to cut deposit interest rates by 0.5-1% per year. Along with the Government signaling its readiness to support system liquidity (through OMO channels, foreign exchange swaps, and refinancing loans), interest rates are expected to peak in early 2Q and drop further in the second half of 2026.

In the short term, KBSV believes that the downtrend in interest rates is not yet clear, as liquidity shortages may continue in 2Q for some main reasons. First, the trend of high credit growth exceeding deposit growth will not reverse in the short/medium term and will continue to put pressure on liquidity in 2Q (data shows that by the end of 1Q26, credit and deposit growth came in at 2.15% and 0.44%, respectively). In absolute terms, by the end of September 2025, the difference has reached VND1.5 trillion. Besides, the net LDR of commercial banks remains high, and the LDR according to Circular 22 has almost reached the ceiling of 85%.

Second, the sentiment of holding and trading cash before changes in tax policy continues to make it difficult for banks to mobilize funds in 2Q. In addition, the disbursement of public investment is unlikely to increase sharply this quarter, which will also cause the treasury to continue to have a budget surplus. Both of these factors will narrow the flow of money back into the banking system.

Third, complex developments in the Middle East have cast more shadows on inflation and exchange rates, leaving the SBV with little room to support liquidity for the system.

However, in 2H26, KBSV expects the trend of cooling interest rates to be clearer, with an average reduction of about 0.5-1%/year compared to the current level thanks to: (1) abundant capital from strong disbursement of public investment capital flowing into the banking system; (2) the easing of the conflict in Iran relieves inflationary and exchange rate pressure, thereby helping the SBV to be more flexible in supporting liquidity for the banking system; and (3) many new policies will be launched in the second half of the year by the Government and the SBV to strive to achieve the 10% GDP growth target, including lowering interest rates.

Following the meeting with the new Governor of the SBV, lending interest rates have only seen a decrease of 50-100 bps at a few commercial banks such as AGR, Nam A Commercial Bank (NAB), and SSB. However, KBSV said this decrease would mainly be temporary and does not reflect a simultaneous adjustment across the entire system.

In general, KBSV believes that lending interest rates will remain stable at the current level in 2Q mainly due to the continued high deposit rates, while banks' NIMs are currently low compared to previous years, and the risk of increased NPLs still exists. For 2H26, lending interest rates should see bigger cuts, mirroring the decrease in deposit interest rates, in order to support economic growth. Notably, this downtrend is likely to be selective, prioritizing key sectors such as exports and industrial production.

Author: NGOC ANH

RECOMMENDED TOPICS