VN

VN

EN

EN

16/07/2026, 02:38

Investment

Is ACB's attraction sustainable?

The attraction of ACB shares of Asia Commercial JSC (HOSE: ACB) comes not only from the expectation of anticipating the 2025 dividend but also from the prospects of a bank that is growing in a controlled and cautious manner.

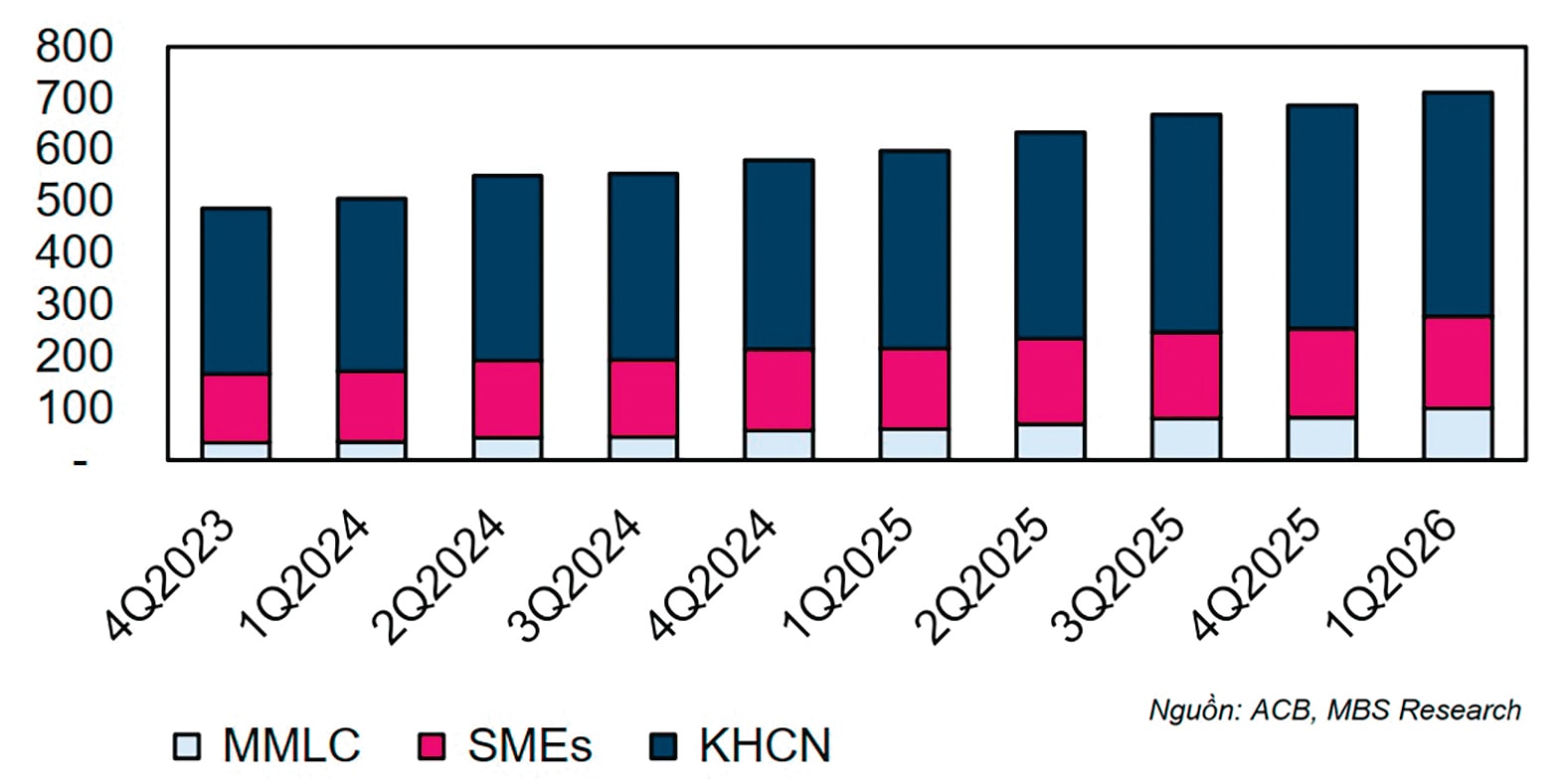

Loan structure of ACB by customer group. Unit: Billion VND. Source: ACB, MBS Research

For financial investors, especially long-term financial investors, they often highly evaluate and place great expectations on businesses that have a growth rate of book value per share (BVPS) thanks to retained earnings. For ACB, the prospect of BVPS growth stems from a solid business foundation and the ability to overcome variables to achieve positive profits.

Cash Flow Pouring into ACB Shares

ACB pays dividends in both cash and shares, with a total ratio of 20%. The final registration date was June 16, so investors rushed to accumulate ACB shares before this date. However, besides the buying demand, ACB shares have been making strong waves since May and extending into the early sessions of June, with continuous reversals of foreign capital flow and net selling by proprietary trading blocks, while a group of shareholders quietly accumulated.

Most notable is the Au Lac shareholder group represented by Ms. Ngo Thu Thuy—a familiar financial investor who previously invested in ACB and was also a major shareholder of Eximbank. Market transaction data shows that over the past nearly two months, this shareholder group has net-bought about 102 million ACB shares, raising their ownership rate at ACB to approximately 9%.

According to observers, there are two reasons why financial investors are currently interested in ACB shares. First of all, ACB's valuation is at a very attractive level (even though it has adjusted after nearly two months of riding the waves to a new market price floor).

According to MBS's valuation, ACB's current valuation at P/B = 1.2x is considered attractive compared to the 5-year average and the entire industry. The target P/B of 1.6x applies to the book value at the end of 2026 and 2027 at a rate of 25% and 75%, respectively. MBS adjusted the 12-month target price for ACB to 33,700 VND/share and maintained an "outperform" recommendation. In addition to the basis of business prospects, there is also the return of the Au Lac group, a former major shareholder of ACB, which MBS expects can help solve the corporate lending puzzle in the coming time.

ACB's consolidated profit in 1Q26 reached 5,368 billion VND, an increase of about 17% over the same period last year

Business Prospects

In the first quarter of 2026, like many other credit institutions, ACB also faced difficulties in reducing capital costs when interest rates rose high, impacting NIM, which reached 2.8%, down 18 basis points compared to the same period last year and the previous quarter. However, consolidated profit reached 5,368 billion VND, an increase of about 17% over the same period last year; ACB's credit growth increased by 2%; and the cost-to-income ratio was controlled at a low level. Notably, ACB's non-interest income segment recorded a 33% growth from bancassurance, and the bank expects this to continue to increase in the future.

ACB's credit growth recorded its main driver from the MMLC customer group (mid-end affluent customers with high stickiness), reaching 14.8% compared to the beginning of this year. Meanwhile, outstanding loans to small and medium enterprises (SMEs) and science & technology groups were quite modest, reaching 0.8% and 1.6% respectively compared to the beginning of the year. ACB's outstanding margin loans at the end of Q1/2026 reached more than 19,560 billion VND, up 12.8% compared to the beginning of the year, contributing significantly to the retail lending segment.

With the forecast that the lending interest rate floor in the remainder of 2026 will tend to decrease slightly, this will help credit flow more strongly into infrastructure construction, energy, and production projects, while retail loan demand is forecast to remain slow. MBS forecasts that ACB will achieve full-year credit growth of about 12%, reaching 100% of the currently granted credit room. In this, lending to the MMLC customer group will still play a key role, especially with support from the return of the Au Lac shareholder group, which holds a major advantage in the ecosystem of industrial parks, logistics, and shipping.

According to their introduction, right from the early days of establishment (2002), Au Lac oriented its development strategy and deployed operations in the field of domestic and international petroleum transportation by sea. To date, the company has established strategic partnerships and directly signed transport contracts with many large domestic cargo owners such as Saigon Petro, Skypec, Thalexim, Petrolimex, PV Oil, Petimex... and foreign cargo owners like Shell, Conoco Phillips, PTT Thailand, Sinopec, Unipec, BP Singapore, Trafigura, PetroSummit, Sojitz, Elico, Petrochina, Petamina, Petron, Horizon Petroleum... At the same time, the company has proven its capacity to operate and exploit the fleet according to international standards, expanding transportation market share and achieving high efficiency.

In 2026, MBS projects that ACB can fully achieve the cautious plan set forth, with total assets by the end of 2026 increasing by 16% compared to the beginning of this year. Credit balance is projected to increase by 16% and will not exceed the credit growth limit approved by the State Bank of Vietnam. Mobilization (including valuable papers) is projected to increase by 16%. The bad debt ratio will be controlled below 2%. Pre-tax profit for 2026 is expected to increase by 14% compared to the 2025 results, equivalent to 22,274 billion VND.

Nevertheless, investors must also be cautious with factors that could affect the bank's business operations as bad debt signals are ticking up with Group 2 debts rising, the real estate market is unlikely to flourish, and the impact of the interest rate environment if it is difficult to adjust downwards as expected... Among these, risks include uncontrollable risks regarding interconnectedness on the National Credit Information Center (CIC) system. Specifically, when an individual or business incurs bad debt at another credit institution, all debts of that customer at the bank will also be automatically downgraded by the system, leading to provisioning pressure that cannot decrease as quickly as initially expected.

Author: LE MY - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS