VN

VN

EN

EN

26/07/2026, 02:00

Investment

Oil prices rebound: Mixed impacts on two groups of stocks

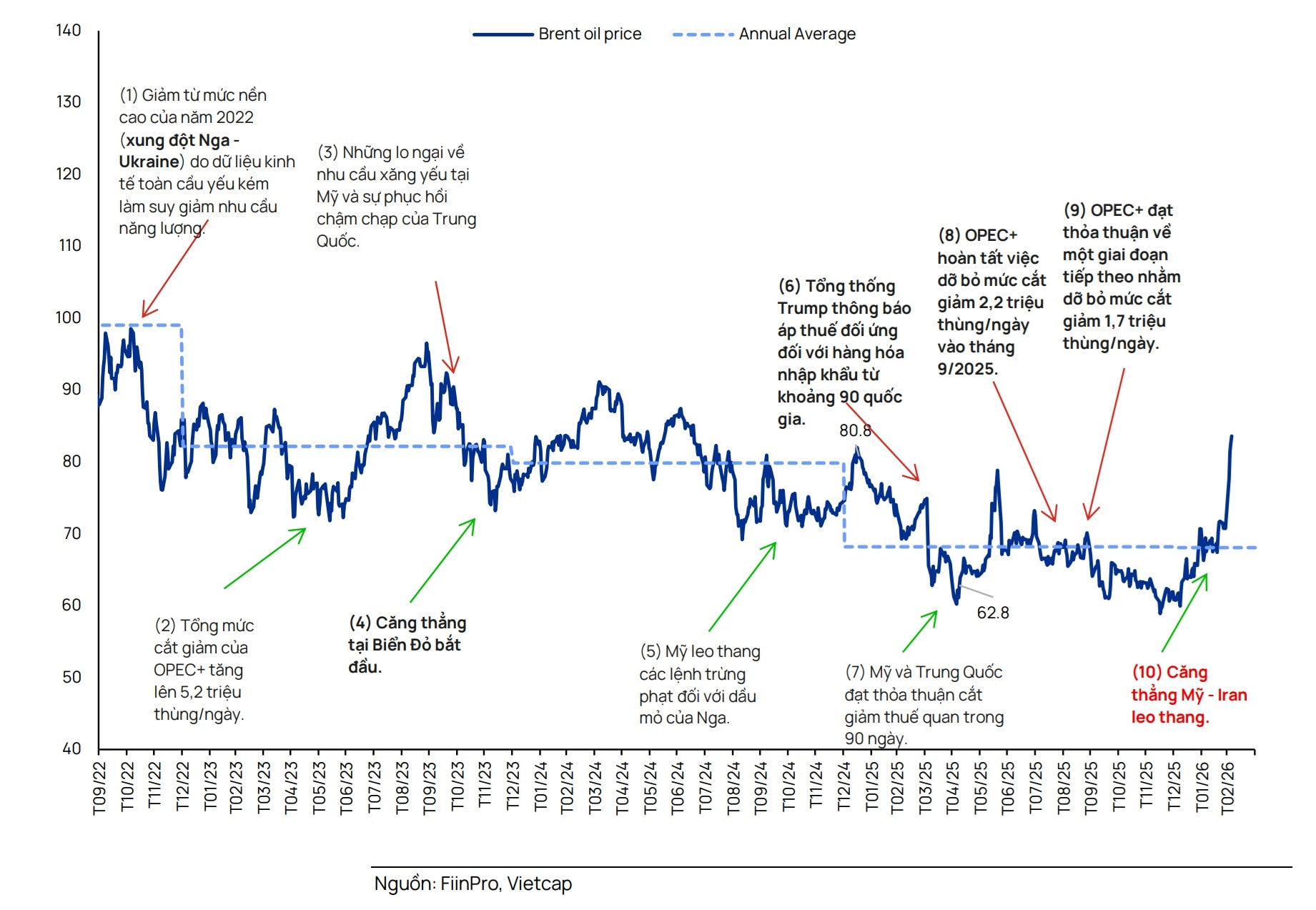

Global oil prices have surged back above the $100-per-barrel mark, underscoring the unpredictable impact of the Middle East conflict on global energy flows.

In the early hours of March 13 (Vietnam time), Brent crude futures traded at $100.03 per barrel, up 8.75%, equivalent to a rise of $8.05 per barrel. Meanwhile, WTI crude reached $95.29 per barrel, climbing 9.21% or $8.04 per barrel.

Higher oil prices could create diverging effects across Vietnam’s stock market.

The rebound follows a recent pullback that had briefly pushed Brent below $90 per barrel, highlighting the volatility in global energy markets as geopolitical risks intensify.

Two Scenarios for Oil Prices

Analysts say the latest surge reflects escalating attacks by Iran targeting oil facilities and transport infrastructure across the Middle East. At the same time, Iran’s supreme leader has reiterated plans to keep the Strait of Hormuz closed — a strategic chokepoint for global energy shipments — as leverage in the ongoing conflict.

According to Goldman Sachs, traffic through the Strait of Hormuz — which accounts for roughly 20% of global oil supply and 30% of global LNG trade — has fallen by about 80–85%.

As of March 4, the bank assumed that traffic through the strait would remain at only 15% of normal levels for the next five days, then recover to 70% within two weeks, before eventually returning to full capacity over the following two weeks.

However, in a March 8 warning, Goldman Sachs said global oil prices could exceed $100 per barrel within days and potentially reach $150 per barrel by the end of March if the conflict shows no signs of resolution. The bank estimated that the impact of the disruption could be 17 times greater than the April 2022 peak triggered by the Russia–Ukraine conflict, which pushed oil prices to around $120 per barrel.

In a recent sector update, analysts at Vietcap Securities noted that oil prices had already surged roughly 50% following the airstrikes, reaching $109 per barrel by March 9. They emphasized that the spike was driven primarily by risks to transport bottlenecks rather than an outright supply shortage.

According to Rystad Energy, the closure of the Strait of Hormuz could disrupt 8–10 million barrels of crude oil per day, equivalent to 8–10% of global supply, even after some shipments are rerouted via Saudi Arabia’s East–West pipeline and Abu Dhabi’s export pipeline.

Iran itself is a major oil producer, pumping around 3 million barrels per day, accounting for roughly 3% of global production.

“Although sanctions have restricted Iran’s exports, its crude still finds its way to global markets, particularly China,” Vietcap analysts noted.

Historical data shows that disruptions in the Strait of Hormuz typically last 30–45 days, after which oil prices tend to cool once conflicts ease.

Assuming a disruption of 10 million barrels per day for two months, the global oil market could face a shortfall of around 0.8 million barrels per day, equivalent to roughly 1% of global supply.

Global inventories may serve as a short-term buffer. According to the International Energy Agency (IEA), global oil stocks stood at approximately 8.23 billion barrels at the start of 2026.

However, if supply disruptions range between 5–10 million barrels per day, it would take 66–133 days for global inventories to fall to levels seen during the Russia–Ukraine conflict.

In 2025, about 13.4 million barrels of crude oil per day passed through the Strait of Hormuz, with more than 80% shipped to Asian countries, underscoring the region’s heavy reliance on the route.

Asian economies currently hold roughly 68 days of crude inventory, according to data cited by Khaosod English. Meanwhile, China and Thailand have recently announced suspensions of exports of certain petroleum products.

Against this backdrop, analysts have outlined two scenarios for Brent prices and raised their average Brent forecasts for 2026–2030 by 9% and 19% respectively.

Under the base case, Brent is projected to average $70 per barrel in 2026, up 17% from the previous forecast of $60 per barrel. In a more optimistic scenario, prices could average $90 per barrel, roughly 50% higher than earlier projections.

A $70-per-barrel average for 2026 would represent a modest 2% year-on-year increase and align broadly with planning assumptions by Petrovietnam (PVN).

Speaking to the press on March 12, Suan Teck Kin, Head of Global Economics and Market Research at UOB (Singapore), offered a relatively optimistic outlook.

He expects the Middle East conflict to last only four to five weeks, as mounting economic damage pressures all sides to seek a resolution.

Under this scenario, oil prices may spike briefly to around $100 per barrel, before gradually easing back toward $80.

Most countries are oil importers and therefore vulnerable to energy price shocks — including the United States, he noted. Rising energy costs are already weighing on economic activity and consumers.

Even oil exporters such as Saudi Arabia and Qatar face losses, as export disruptions leave storage facilities overloaded while production must be curtailed.

“The significant economic damage will likely force the parties involved to resolve the conflict sooner rather than later,” Suan Teck Kin said.

He also noted that the current tensions largely involve three key actors — the United States, Iran and Israel. The absence of broader alliances entering the conflict increases the likelihood of a relatively swift resolution compared with multi-country wars.

Still, in a more pessimistic scenario where tensions persist, oil prices could remain in the $100–110 per barrel range, potentially fueling inflation and slowing economic growth.

Implications for Vietnam’s Energy Market

Higher oil prices are expected to push up other energy costs as well.

Vietcap analysts raised their assumptions for fuel oil (FO) prices, which serve as a reference for Vietnam’s gas pricing. In the base scenario, average FO prices for 2026–2030 are expected to rise 10%, while the optimistic scenario assumes a 20% increase, largely reflecting Brent price forecasts rising 9% and 19% respectively.

Vietnam’s LNG import prices are also projected to increase slightly. In the base case, average LNG import prices are expected to rise 2%, driven mainly by a 29% increase in 2026 compared with earlier forecasts and a 22% year-on-year increase, before moderating in later years.

Under the optimistic scenario, LNG import prices could increase by 9% on average during 2026–2030.

Coal prices are also expected to rise, by 5% in the base scenario and 10% in the optimistic scenario, as demand grows for coal as a substitute energy source when oil and gas prices climb.

Vietnam remains structurally dependent on energy imports. According to Vietcap, the country typically imports two-thirds of its crude oil, about one-third of its refined petroleum products, roughly 70% of its LPG, and around 15% of its gas demand in the form of LNG.

Despite the growing reliance on imported energy, refineries and distributors have maintained at least two months of inventories, including around 30 days at refinery level and 25–30 days at the distributor level.

On March 2, PVGas Trading declared force majeure on certain LPG deliveries due to disruptions beyond its control, delaying or reducing shipments scheduled through March 10.

However, on March 3, Petrovietnam Gas (GAS) announced that it had secured LPG supply by diversifying imports beyond the Middle East, prioritizing domestic demand and increasing output at the Dinh Co and Ca Mau gas processing plants by around 5%. LNG supply remains stable, mainly sourced from Australia and partly from the United States.

Stock Winners and Losers

Higher oil prices could create diverging effects across Vietnam’s stock market.

According to Vietcap, PVS remains the top pick in the sector, while several companies could benefit directly from the price surge, including BSR, PVT, DPM and DCM.

GAS may see a mild positive impact, as higher FO prices could lift gas selling prices for parts of its portfolio that account for roughly 23% of expected 2026 volumes. Higher LPG prices may also partially offset lower sales volumes due to elevated prices.

Oilfield service providers such as PVS and PVD could benefit moderately, as higher oil prices improve profitability for upstream producers, supporting demand for EPC services, drilling activity and rig day rates.

BSR, the operator of Vietnam’s largest refinery, is expected to benefit from inventory gains and stronger refining margins. Diesel crack spreads in Singapore have reportedly surged to around $58 per barrel, doubling after the conflict, while gasoline spreads have risen to roughly $24 per barrel.

Shipping company PVT could also benefit from rising tanker freight rates. Spot and pooled contracts account for around 25–30% of its volumes, allowing it to capture higher rates.

Aframax tanker rates have climbed 49% year-on-year, Medium Range tanker rates 22%, and Handysize tanker rates 12%. Rerouting vessels around the Cape of Good Hope to avoid the Strait of Hormuz could further increase shipping distances and freight rates.

The Baltic crude tanker index has risen to around 3,083 points, up 55% since the conflict began, while the refined products shipping index has climbed 83% to about 1,654 points.

Fertilizer producers DPM and DCM may also benefit. Iran accounts for roughly 10% of global urea exports, and international urea prices have risen about 22% to $600 per ton, helping offset higher gas input costs.

Meanwhile, PLX and OIL carry a neutral outlook. While higher oil prices could support short-term earnings due to lower input costs in late 2025, prolonged high prices may squeeze margins if retail fuel prices remain regulated.

Power producers such as NT2, POW, QTP and PPC could face mild negative impacts as higher oil, gas and coal prices raise generation costs and potentially reduce dispatch levels, although most input cost fluctuations are passed through to EVN under contracted volumes.

Author: LE MY - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS