VN

VN

EN

EN

15/07/2026, 10:39

Investment

Where Is real estate investment capital flowing?

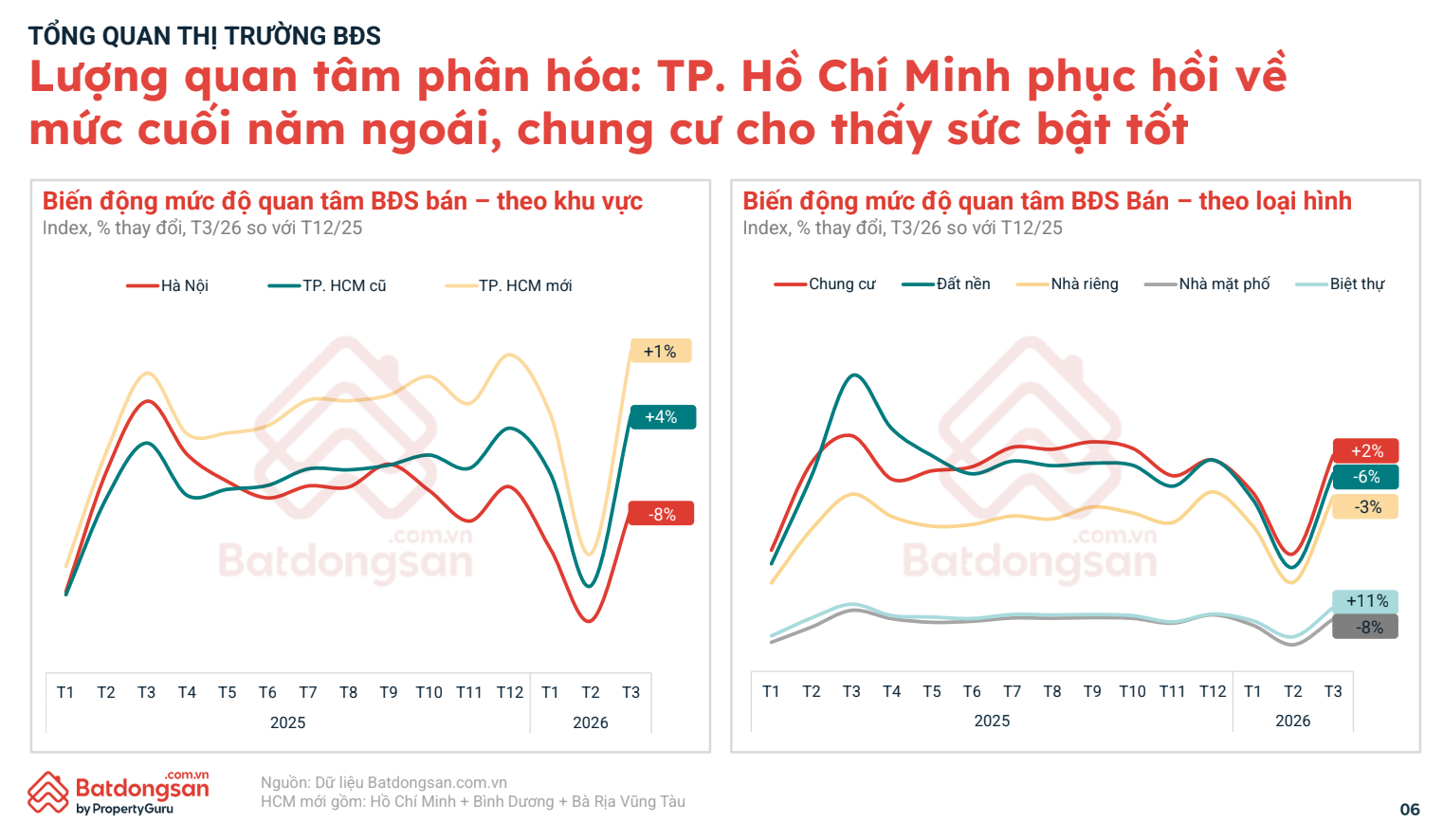

Vietnam’s real estate market in Q1 2026 showed signs of recovery after the Lunar New Year, though unevenly. Apartments led the rebound, land plots remained cautious, and landed houses displayed clear divergence between the two major cities.

.jpg)

Data from Batdongsan.com.vn indicates that the market is entering a phase of selective recovery, as capital flows and buyer behavior are no longer evenly distributed across segments.

Apartments Remain the Bright Spot

At the “Overview of the Real Estate Market in Q1 2026” event held on April 15, Ms Do Thi Ngoc Anh, Senior Sales Manager at Batdongsan.com.vn, noted that overall market interest improved after the Tet holiday. However, demand is increasingly concentrated in products with real utility value and resilience to macroeconomic volatility.

Notably, Ho Chi Minh City is recovering slightly faster than Hanoi. Demand for property searches in HCMC has begun to pick up again, while Hanoi has yet to return to the level of interest seen at the end of 2025.

Within this fragmented landscape, apartments continue to stand out, recording both increased interest and solid liquidity.

Data from March 2026 shows that interest in apartments across many areas rose by 4% to 7% compared to December 2025—significantly higher than other segments. This suggests that capital is flowing back into housing products that meet genuine residential demand.

A survey by Batdongsan.com.vn also highlights a clear shift in home-buying purposes. Up to 67% of apartment buyers purchase for owner-occupation, 30% for rental investment, and only 4% for short-term speculation. Compared to previous periods—when speculative activity accounted for 30%–40%—this shift indicates a move toward a more sustainable market foundation.

In terms of pricing, apartments continue to demonstrate strong price resilience despite ongoing market fluctuations. In Q1 2026, the average asking price in Hanoi reached approximately VND 87 million per square meter, while in HCMC it stood at around VND 69 million per square meter, marking modest quarter-on-quarter increases of 1.5% to 2.4%.

Beyond leading the market, the apartment segment also reflects urban development trends tied to infrastructure expansion. In Hanoi, projects are expanding along ring road corridors and across river developments. Meanwhile, in HCMC, new supply is concentrated in near-central areas and along major transport axes.

Demand migration patterns also differ between the two cities. Buyers in HCMC are increasingly expanding their search to suburban areas such as Thu Duc City and neighboring localities like Di An and Thuan An. In contrast, Hanoi-based buyers are looking toward provinces such as Hung Yen and Hai Phong, or even further to Da Nang and Khanh Hoa.

Interest levels diverge: Ho Chi Minh City rebounds to last year’s levels, apartments show strong momentum

Land Plots Remain Cautious, Landed Houses Diverge

In contrast to apartments, land plots remain highly sensitive to macroeconomic factors. Changes in interest rates, policies, or planning information quickly impact both buyer interest and transaction volumes.

In Q1 2026, both Hanoi and HCMC recorded declines in interest in land plots compared to the end of 2025, with Hanoi seeing a sharper drop. However, prices largely remained stable rather than declining, suggesting that sellers’ expectations remain high while buyers are becoming increasingly cautious.

Regionally, Central Vietnam has emerged as a bright spot, with interest in land plots rising by 10% to 28% in several localities, driven by new supply entering the market—particularly in tourism-driven urban areas.

For landed houses, the data reveals clear divergence between the two major markets. In HCMC, interest increased by about 7% compared to the end of 2025, while Hanoi experienced a sharp decline.

The primary driver lies in price movements. In Hanoi, landed house prices have risen continuously over the past year, with some areas seeing increases of 20% to 30%, weakening purchasing power. In contrast, in HCMC, after a period of rapid price growth, prices have adjusted slightly by 1% to 7% in certain areas, helping to revive demand.

In practice, districts such as District 5, Tan Binh, and District 8 have seen interest increase by 8% to 15% following price corrections. This underscores that pricing remains the key determinant of demand in the current market context.

Author: DIEU HOA - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS