VN

VN

EN

EN

22/07/2026, 02:38

Investment

Will real estate earnings rebound to a high level?

Many real estate companies are continuing to set ambitious profit growth targets for this year.

The 2026 Annual General Meeting of Shareholders (AGM) of Vingroup JSC (HOSE: VIC) is among the most anticipated.

VIC and VHM target strong revenue and profit growth in 2026, driven by core pillars, particularly real estate projects. (Illustration: Vinhomes Green Paradise project in Can Gio)

VIC, VHM set breakthrough profit targets

At the AGM held on April 22, Vingroup approved an adjusted business plan with higher revenue and after-tax profit targets for 2026. Specifically, projected revenue is VND 485 trillion, up nearly 46% year-on-year, while after-tax profit is expected to reach VND 35 trillion—roughly three times the 2025 figure.

Compared to the plan announced on April 1, shareholders approved increases of VND 35 trillion in revenue and VND 10 trillion in profit.

Vingroup’s business plan is built on actual operating results and forward-looking prospects across the group and its subsidiaries. Notably, this follows a strong 2025 performance, with consolidated revenue reaching VND 331.8 trillion (up 76% year-on-year) and after-tax profit of VND 11.1 trillion, exceeding targets.

This year, Vingroup continues to focus on key pillars such as Technology–Industry (VinFast) and Tourism–Hospitality (Vinpearl, HOSE: VPL). At the same time, new pillars such as Infrastructure and Green Energy are positioned as long-term growth drivers. Through projects like the Ben Thanh–Can Gio and Hanoi–Quang Ninh high-speed rail lines, VinSpeed aims to pioneer modern infrastructure development, shaping the future of Vietnam’s railway industry. Meanwhile, VinEnergo focuses on renewable energy, carbon credits, and energy storage, gradually building a sustainable energy ecosystem.

In residential real estate, Vinhomes continues to assert its leadership with a strategy centered on next-generation mega urban developments aligned with ESG standards, modern transport infrastructure, strong connectivity, and premium amenities to meet real demand.

Vinhomes’ large-scale urban projects across key growth hubs such as Ho Chi Minh City, Da Nang, and Quang Ninh not only drive sustainable urbanization and attract population inflows but also create significant medium- and long-term growth potential.

Previously, on April 21, Vinhomes JSC (HOSE: VHM) held its AGM, approving record targets for 2026: projected revenue of VND 285 trillion and after-tax profit of VND 60 trillion, maintaining its leading position in Vietnam while gradually expanding globally.

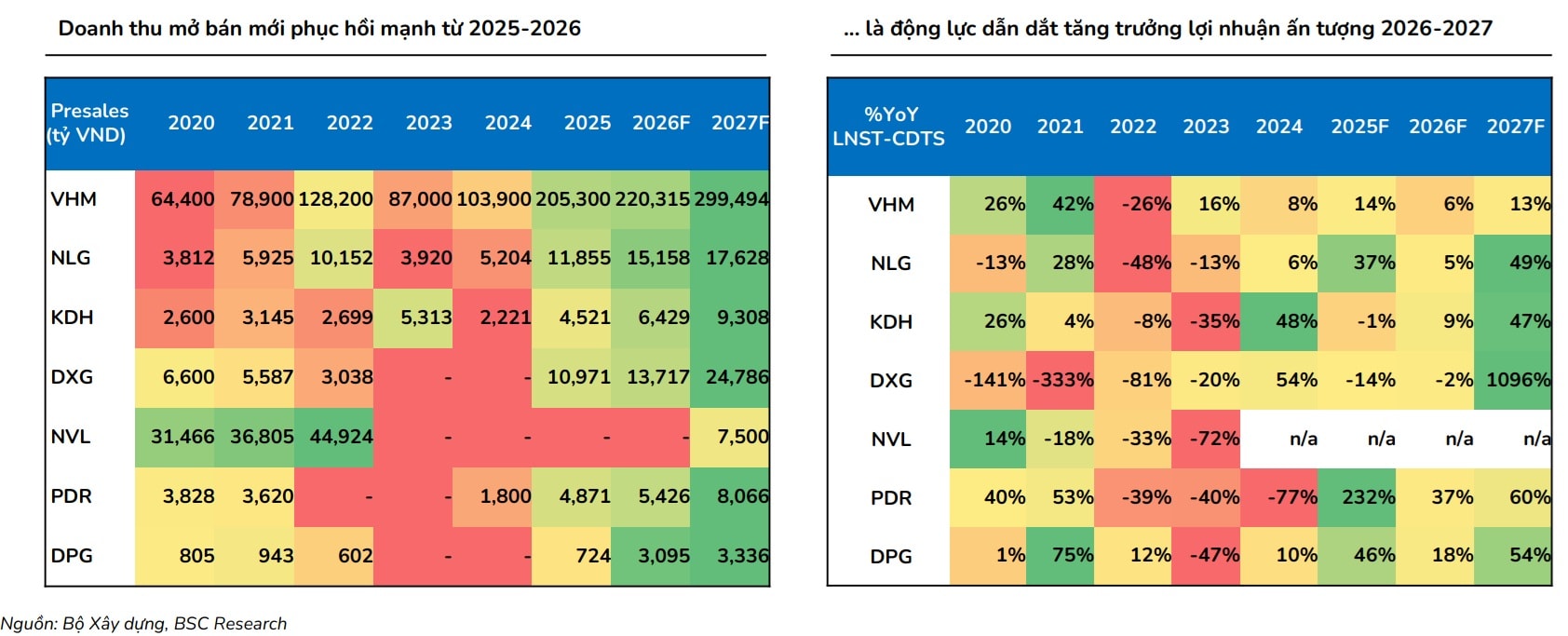

The company expects 2026 pre-sales to reach VND 300–350 trillion, up 46–65% year-on-year. Key contributing projects include Can Gio, Hai Van Bay, Hau Nghia, Duong Kinh, and Ocean Park 2–3, with upcoming projects such as Ha Long Xanh and the Ho Chi Minh City University urban area also expected to contribute.

Regarding profit, around 30–40% is expected to come from sales booked by the end of 2025 but not yet recognized, mainly from strong-selling projects such as Dan Phuong, Duong Kinh, Vu Yen, and Ocean Park 2–3. The company is also negotiating several bulk transactions, including new projects.

Although Q1 2026 results have not been officially released, estimated sales reached VND 70–80 trillion. The Hai Van Bay project, launched in late March 2026, recorded solid results with 1,300–1,400 booking contracts and an absorption rate of 80–90%.

New launches to drive cash flow

Beyond VIC and VHM, which dominate both the economy and the real estate market—VHM alone accounts for around 80% of total revenue among listed residential developers—analysts at BSC expect industry profits to recover strongly this year.

According to BSC, large backlogs and improved financial conditions following restructuring have enabled developers to proactively implement projects and continue market consolidation through M&A.

Strong momentum from new launches in 2025–2026 is expected to drive industry-wide profit growth.

BSC forecasts that total industry net profit attributable to minority shareholders will reach VND 46.3 trillion in 2026 (2.3% YoY) and VND 55.9 trillion in 2027 (20.7% YoY). Excluding VHM, the figures would be VND 2.8 trillion (12.8% YoY) and VND 6.6 trillion (133.9% YoY), respectively.

From an interest rate perspective, low rates tend to stimulate both investment and speculative demand, pushing housing prices up by around 15–25% annually. Current interest rates are broadly in line with previous cycles, highlighting the trade-off between borrowing costs and housing prices.

Based on sensitivity analysis—including assumptions on average housing prices, 25-year loan terms, minimum household income of VND 50 million/month, loan-to-value ratios, and interest rates—analysts estimate that a safe monthly housing cost is around 30–40% of income, with 50% as the upper limit. Under current conditions (mortgage rates of 10–10.5% and average prices of VND 80 million/m²), typical households can still afford housing.

Legal bottlenecks are also gradually being resolved, supporting project supply. Although buyer sentiment weakened in Q4 2025–Q1 2026, transaction volumes still grew strongly (35% YoY, 11% QoQ). Inventory reached record levels, driven by increased approvals and eligible-for-sale products, particularly in Q4 2026.

With profit recovery expected to return to a high baseline, analysts believe real estate stocks are now attractively valued after a sharp correction in late 2025 and early 2026, with discounts of 30–50% from their October 2025 peaks (e.g., DXG -39.3%, PDR -38.6%, NLG -34.6%, TCH -32.2%, KDH -30.5%).

“Currently, the sector is trading at an average P/B of 1.3x, below the previous cycle average of 1.5x (2013–2022), and near the lower bound seen during the strong growth phase of 2017–2019. We believe the market’s structural shift toward a healthier cycle—supported by clearer profit prospects and attractive valuations—will drive a positive re-rating in the near term,” BSC noted.

For VIC and VHM, their strong stock performance during the AGM season, combined with robust business growth prospects and attractive dividend policies, is expected to continue supporting share price momentum.

At the recent AGM, VHM shareholders approved a 160% total dividend payout, including 60% in cash (VND 6,000 per share, equivalent to a 4% yield) and 100% in stock (1:1 ratio). The plan is expected to be executed within six months.

This flexible dividend strategy is considered particularly well-timed as foreign capital inflows are expected to increase. Stock dividends will not involve cash outflows but will help expand charter capital, improve liquidity, and enhance accessibility for investors.

Over the next six months, large-cap, highly liquid stocks meeting foreign investment criteria are expected to attract early inflows from active funds ahead of potential market reclassification, while passive funds will follow once Vietnam is officially included in global indices. These stocks could account for a significant share of the estimated initial inflow of nearly USD 1.7 billion. Alongside HPG, MSN, and VNM, VIC and VHM are among the top candidates for such capital allocation under FTSE index frameworks.

Author: LE MY - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS