VN

VN

EN

EN

09/07/2026, 11:15

Investment

Geopolitical conflict: A shift in investment thinking is needed

According to Huỳnh Hoàng Phương, investment financial analyst, markets are entering a late-cycle phase where returns moderate and risks rise, forcing investors to prioritize risk management, liquidity and selective allocation.

In the current market environment, the core objective of investing is no longer maximizing returns—it is managing risk. That shift, as financial analyst Huỳnh Hoàng Phương argues, reflects a deeper structural transition: markets are moving into the late phase of the asset cycle, where volatility rises, dispersion increases, and traditional assumptions begin to break down.

This is not a moment defined by a single geopolitical shock. Rather, it is the convergence of multiple forces—tightening liquidity, persistent inflation risks, and geopolitical fragmentation—that is reshaping how capital behaves.

Misreading the Cycle: The Most Costly Investor Mistake

One of the most common errors investors make is reacting to events without situating them within the broader asset cycle.

According to Phương, the current phase of the market is fundamentally different from the early stages of the rally that began in 2023. That earlier phase—particularly from mid-2024 through the end of 2025—was characterized by synchronized asset appreciation, fueled by abundant liquidity.

Across asset classes, the gains were substantial: gold surged approximately 129%, equities rose 77%, and primary real estate in Vietnam’s two largest cities increased by roughly 71%. For many investors, this created the illusion of structural wealth creation.

But the underlying driver of that rally—rapid monetary expansion—is now fading. Global money supply growth, which peaked at around 12% in 2025, is expected to slow. Domestically, Vietnam’s credit growth of over 19% last year is also projected to moderate.

As this tailwind weakens, asset prices are no longer supported uniformly. Expected returns must adjust downward—while risk, critically, does not decline in tandem. In fact, it may increase.

When Risk Becomes the Primary Variable

In early-cycle markets, investing is largely about capturing beta—riding the broad upward trend. In late-cycle conditions, however, success depends on discipline and risk control.

Phương identifies three principles that become essential in this environment.

First, diversification shifts from theory to necessity. When assets no longer move in tandem, concentration risk becomes far more dangerous. Portfolios overly exposed to a single theme or asset class are increasingly vulnerable to sharp drawdowns.

Second, liquidity becomes a strategic option. In volatile markets, the ability to reallocate capital quickly is not just defensive—it is a source of opportunity. Investors with sufficient liquidity can reposition into dislocated assets when others are forced to sell.

Third, alpha begins to dominate beta. As dispersion increases, asset selection becomes more important than market direction. In both equities and real estate, performance gaps between sectors and individual assets are widening. Passive exposure is no longer sufficient.

Taken together, these principles do more than mitigate risk—they enhance resilience. And resilience is the defining advantage in late-cycle markets.

A Test the Market Has Not Fully Passed

The recent escalation involving Iran offers a real-time case study of how markets behave under stress.

In the immediate aftermath, global equity markets reacted in line with historical patterns. Excluding the U.S., global equities declined roughly 8.5%, while emerging markets fell around 9.3% over a two-week period—consistent with what analysts would describe as a “moderate panic” response to geopolitical shocks.

Vietnam’s VN-Index followed a similar trajectory, dropping nearly 9.8%. At one point, the index experienced a drawdown of 13.1% from its 200-day peak, marking a meaningful correction within a broader sideways or mildly upward trend.

Historically, such corrections often serve as a reset mechanism—clearing excess valuations and laying the groundwork for potential recovery, provided that the long-term trend remains intact.

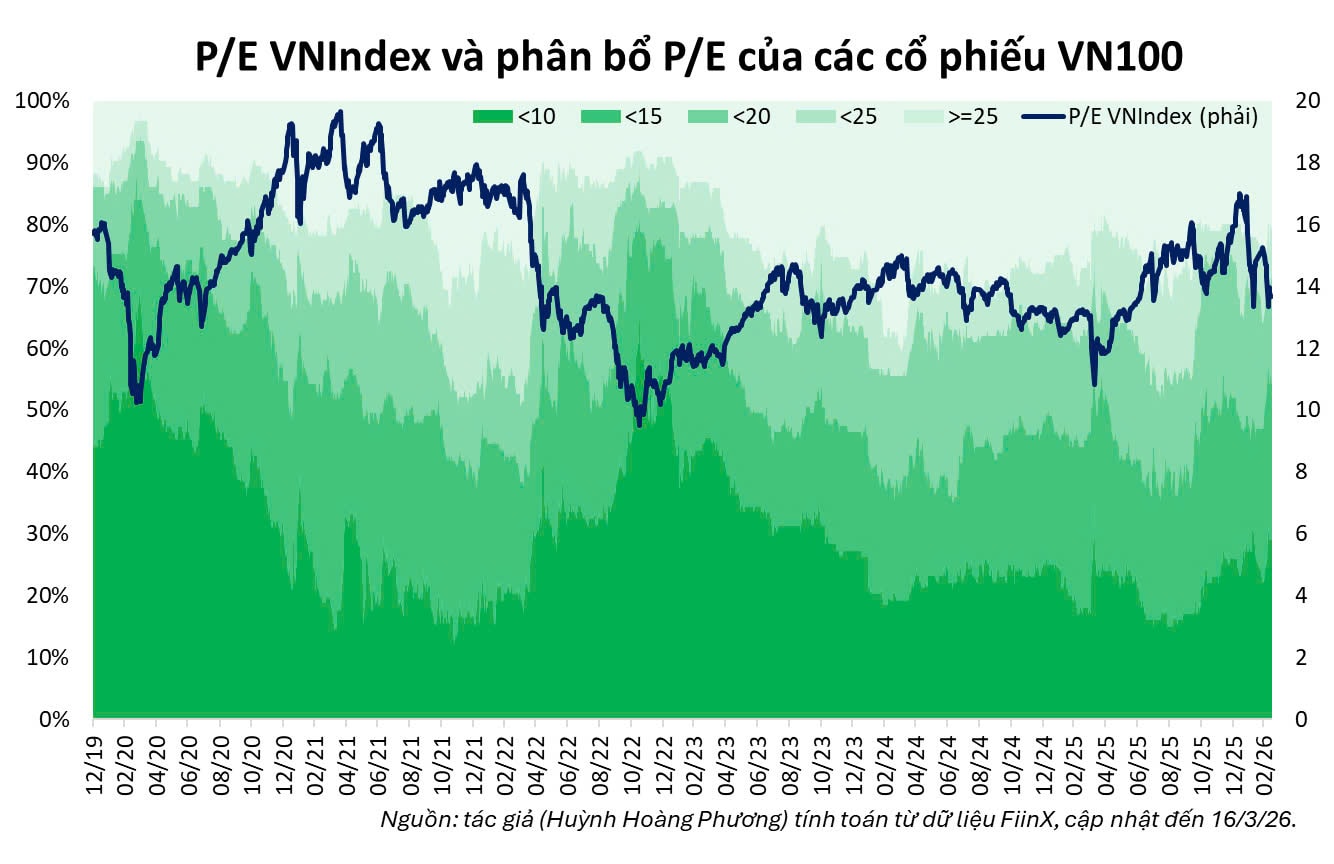

From a valuation perspective, that process is already underway. Prior to the sell-off, more than 80% of VN30 stocks were trading at elevated valuation levels, a hallmark of late-stage bull markets. The recent correction has brought many of these stocks back into more reasonable ranges, potentially supporting short-term technical rebounds.

However, focusing solely on short-term market reactions risks missing the bigger picture.

The more significant risks lie in the medium term. Geopolitical conflicts—especially those affecting energy supply chains—tend to feed into inflation and input costs with a lag. These effects are not immediately reflected in asset prices but can have lasting consequences for earnings and policy.

For investors, this reinforces a critical point: attempting to time market bottoms is less effective than building portfolios capable of adapting to evolving macro conditions.

Gold’s Underwhelming Response: A Data Perspective

One of the more surprising aspects of the current environment is gold’s relatively muted performance, despite heightened geopolitical tensions. Yet historical data suggests this is not unusual.

Looking at more than five decades of gold price behavior, a consistent pattern emerges: after three consecutive years of strong gains, the fourth year—such as 2026—typically sees a significant slowdown in returns. At the same time, volatility increases, often reaching 1.5 to 2 times the average of the preceding period.

This aligns closely with current market dynamics.

Gold, like equities, is exhibiting the defining characteristics of a late-cycle asset: diminishing return potential coupled with rising volatility.

The implication is clear. The traditional narrative of gold as a straightforward safe haven becomes less reliable when macro conditions shift—particularly when interest rates remain elevated.

The current global environment is not defined by a single risk, but by the accumulation of multiple, overlapping uncertainties—geopolitical tensions, energy disruptions, and monetary policy constraints.

This increases both the frequency and magnitude of market shocks.

In such a landscape, the advantage no longer belongs to investors who attempt to predict short-term movements with precision. Instead, it lies with those who construct portfolios that are both resilient and flexible.

History shows that the most significant investment mistakes tend to occur in the late stages of a cycle—when risks are rising but not yet fully recognized.

Yet this does not mean opportunities are absent. Rather, the nature of opportunity has changed.

Success now depends on correctly positioning within the cycle, recalibrating return expectations, and prioritizing risk management through diversification, liquidity, and selective asset allocation.

In a market where returns are no longer easy, survival—and ultimately outperformance—belongs to those who understand that managing risk is not a constraint on returns, but the foundation of them.

Author: TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS