VN

VN

EN

EN

09/07/2026, 11:15

Investment

Market valuations leave more room for selective investment strategies

The VN-Index has approached the 1,900-point threshold, but the prolonged “green outside, red inside” condition — where the index rises while many stocks decline — has led to increasingly polarized market valuations.

Current market valuations still leave room for growth under selective investment strategies, particularly for long-term investors positioning ahead of Vietnam’s anticipated market upgrade.

Market Liquidity and Capital Flow Dynamics

In its May stock market strategy report, SSI Securities reviewed April’s strong market rebound, describing it as an impressive “comeback rally” that gave the second quarter of 2026 a favorable start. After falling 11% in March, the VN-Index posted gains in all four weeks of April, rising 10.7% for the month — its strongest monthly increase since August 2025.

.jpg)

Current market valuations still leave room for selective investment strategies. (Illustrative image)

According to SSI Research, the market’s recovery was supported by a broader rebound in global equity markets, with many indices surpassing previous peaks as tensions in the Middle East temporarily eased. Additional support came from FTSE Russell’s confirmation that Vietnam would be upgraded to emerging market status effective from September 2026. Positive first-quarter earnings results and new government support measures — including efforts to lower interest rates and raising the tax threshold for household businesses to VND 1 billion — also contributed to sentiment.

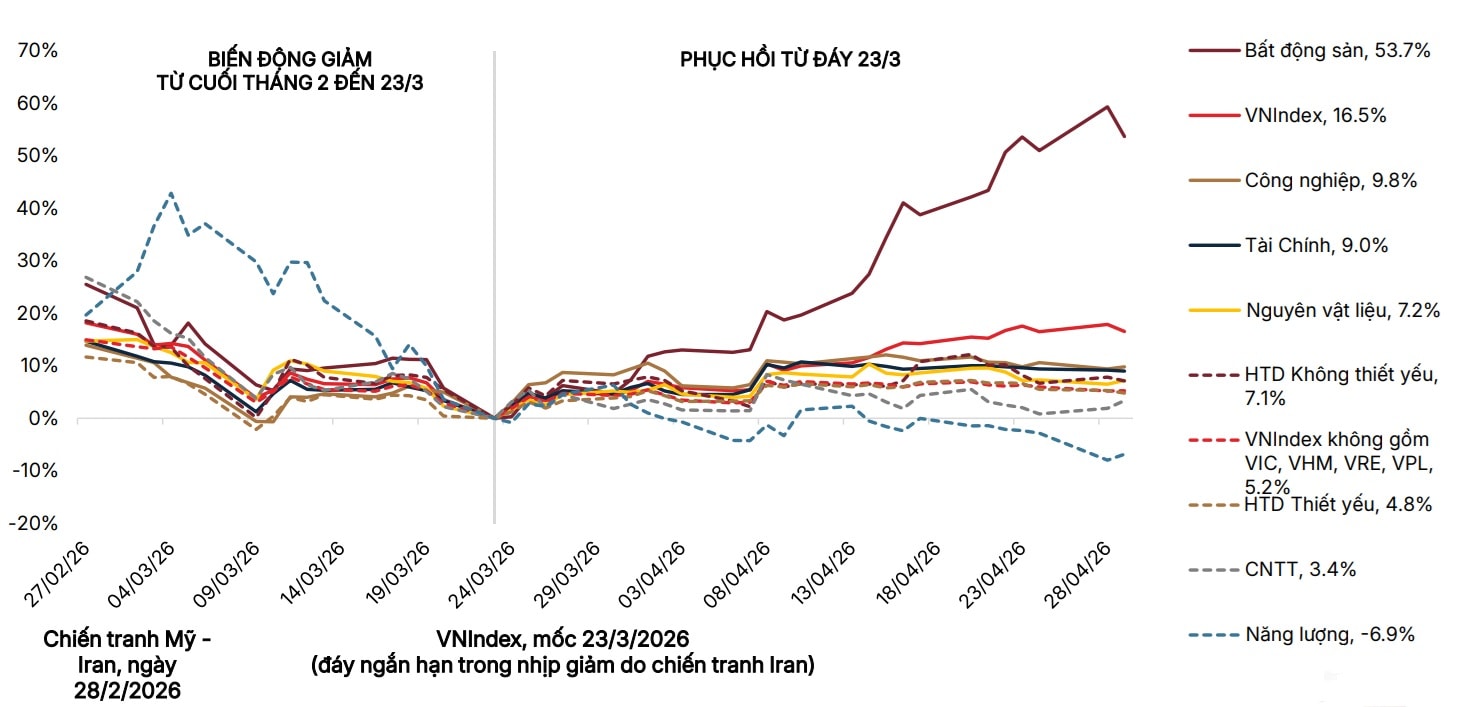

However, much of the market’s rebound was driven by real estate stocks. In April alone, Vingroup subsidiaries VIC (58.5%) and VHM (41.7%) contributed 167 points out of the VN-Index’s total 179-point increase. Excluding Vingroup-related stocks, the VN-Index was essentially flat in April, gaining only 0.6%, according to market data.

This reflects the “green outside, red inside” nature of the market: despite the benchmark index nearing the historic 1,900-point level, many investors remain in negative territory.

Still, the banking sector posted positive performance, with notable gains from TCB (10.3%), LPB (12.9%), STB (8.5%), and MSB (8.2%).

Market liquidity, however, weakened. Average daily trading value in April fell to VND 26.2 trillion per session, down roughly 22% from the previous month and significantly below the first-quarter average of VND 34.7 trillion.

Capital flows also remained highly concentrated in the real estate sector, led by Vingroup-related stocks. Average trading value in the sector rose 75% month-on-month to around VND 3 trillion per session, while liquidity across most other sectors declined sharply.

The drop in market liquidity reflected investor caution amid escalating geopolitical tensions, rising inflation risks, and tightening policies aimed at improving credit quality — particularly in the real estate market. Higher deposit interest rates also continued to weigh on sentiment.

Meanwhile, foreign investors remained net sellers, with net outflows reaching VND 13.3 trillion in April, an improvement from VND 17.5 trillion in March. The easing pressure was mainly due to lower ETF-related selling, as net ETF withdrawals narrowed to VND 442 billion from VND 3.3 trillion in the previous month.

Overall, foreign investors recorded net sales of VND 30 trillion during the first quarter. Cumulative net selling over the first four months exceeded VND 43 trillion, continuing to pressure overall market liquidity.

Market Valuation and Outlook

As of the end of April 2026, the VN-Index was trading at a forward P/E ratio of 13.2x, approaching its 10-year average of 14.0x. Excluding Vingroup stocks (VIC, VHM, and VRE), the market valuation drops to just 10.3x.

“This valuation level still leaves room for selective investment strategies, especially as Vietnam’s market upgrade story remains a medium-term catalyst, including the possibility of being added to MSCI’s watchlist,” SSI noted.

After April’s supportive developments — including the market upgrade outlook, positive first-quarter earnings growth, lower oil prices, and government support policies — May is typically considered a more “information-light” period for the market.

SSI Research estimated that total margin lending across the market reached approximately VND 424 trillion by the end of March 2026, up 3% quarter-on-quarter and roughly 50% year-on-year. This increase was equivalent to around 35% of foreign investors’ net selling value during the same period.

Despite the sharp rise, the margin loan-to-equity ratio of securities firms remained manageable at around 102%, thanks to significant capital increases during 2025 and higher retained earnings. However, margin debt relative to HOSE free-float market capitalization rose to 13.4%, compared with 12.2% at the end of 2025 and 10.8% at the end of 2024.

Profit growth is also expected to slow in coming quarters. Analysts anticipate earnings momentum will weaken due to persistently high fuel and capital costs, combined with a high comparison base from the second and third quarters of 2025, when market-wide NPATMI growth exceeded 30% year-on-year, compared with 21% in the first quarter of 2025.

“The combination of these factors may limit the market’s upside and increase volatility in the coming month. Nevertheless, any sharp corrections could create accumulation opportunities at more attractive valuations for long-term investors,” SSI said.

With market liquidity typically declining in May, capital flows may increasingly favor mid-cap stocks with strong earnings prospects and attractive valuations. SSI’s Investment Analysis and Advisory Center therefore recommends focusing on company fundamentals. Priority themes include businesses capable of sustaining profit growth in the second half of 2026, attractively valued mid-cap firms with distinct growth drivers, companies with healthy balance sheets and stable dividends, as well as re-rating opportunities linked to divestments, IPOs, or corporate restructuring.

Highlighted stocks include HPG, DGW, POW, VCB, FPT, DPR, DCM, TNG, and PVT.

Author: AN DINH - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS