VN

VN

EN

EN

26/07/2026, 02:00

Investment

Short-term risks persist: What investment strategy should investors adopt?

The market continues to face several short-term risks, including liquidity pressure and a narrowing gap between equity earnings yields and prevailing interest rates.

Historical data since 2010 shows that the market has often staged strong rebounds after sharp declines, according to analysts at SSI Research, following six consecutive sessions of losses in which the VN-Index dropped about 12% (excluding the most recent recovery).

.jpg)

According to SSI Research, fundamental factors remain supportive.

Looking at historical patterns, the VN-Index recorded gains in about 80% of similar cases within 2–4 weeks, with an average return of 6.6% after one month and roughly 30% after one year.

Notably, March has seen negative performance only twice — in 2015 and 2020. Even in March 2022, the index still advanced despite the Russia–Ukraine conflict and oil prices climbing to $127 per barrel.

According to SSI Research, fundamental factors remain supportive.

First, corporate earnings prospects for Q1 2026 remain positive, with sectors such as consumer goods, construction materials, fertilizers, securities, and oil & gas expected to report strong growth. Profit targets for 2026 also appear optimistic, with many banks, retailers, and real estate firms targeting 20–30% earnings growth.

Second, the market upgrade review scheduled for April 7 could serve as an important catalyst. Vietnam is considered well-positioned to pass the interim review and potentially join the FTSE Emerging Markets index by September.

At the same time, market valuation has corrected to a forward 2026 P/E of around 12.2x, below the 10-year average of approximately 14x.

However, the narrowing spread between earnings yield and interest rates could limit the market’s upside potential.

In this context, analysts believe the market is likely to reward patient investors, as returns may come less from short-term enthusiasm and more from holding fundamentally strong stocks through periods of volatility.

SSI Research expects that a market upgrade scenario could attract significant foreign capital into large-cap stocks such as VIC, HPG, FPT, VHM, and VCB.

Nevertheless, short-term risks remain, including liquidity pressure and a narrowing earnings yield premium over interest rates.

Potential Inflows from a Market Upgrade

The market upgrade story is also increasing expectations for passive capital inflows and improving Vietnam’s position in global portfolio allocations.

According to MBS Research, historical experience from many countries suggests that equity markets often post strong gains 6–12 months before an official market upgrade.

Once a market is included in the MSCI or FTSE Emerging Market indices, tens of billions of dollars from global ETFs and active funds must rebalance portfolios to reflect the new weighting.

These are disciplined passive flows, typically deployed according to index weightings and maintained over the long term.

Following September 2026, when Vietnam could officially be upgraded, ETFs tracking the FTSE Emerging index are expected to begin allocating capital.

MBS Research estimates that Vietnam could attract $0.5–1 billion in passive inflows during the initial phase.

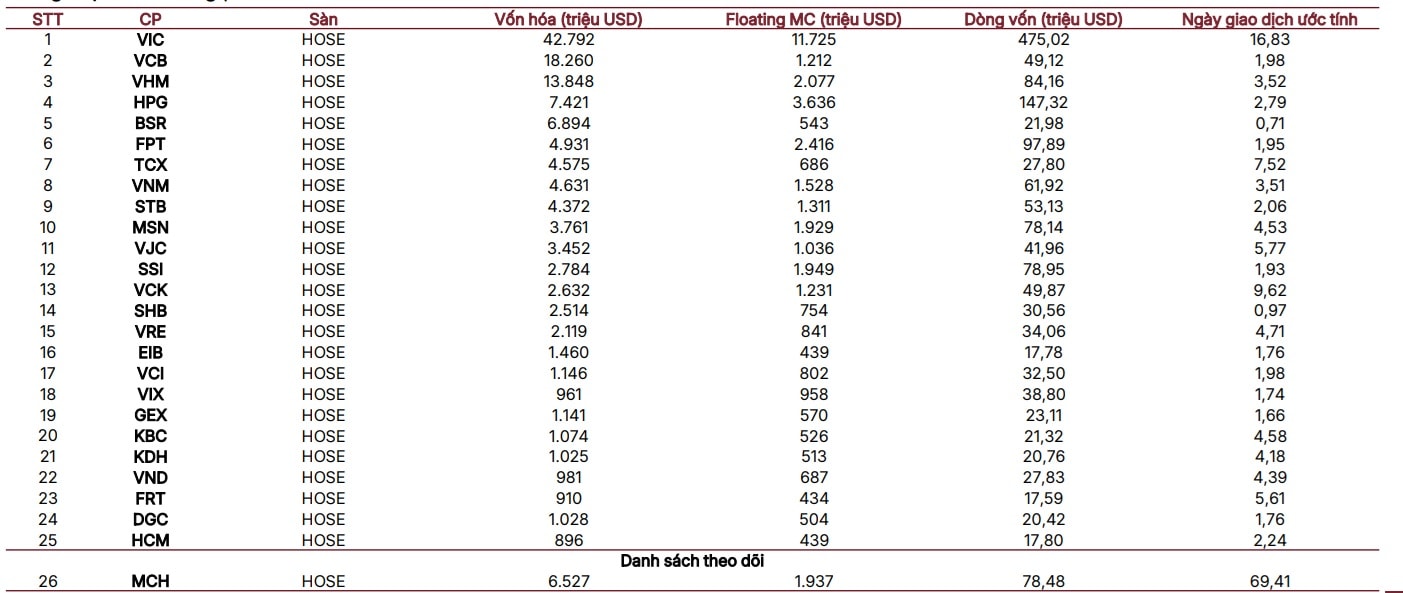

Based on a simulation of potential constituents for the FTSE Global All-Cap Index, around 30 Vietnamese stocks currently meet the preliminary criteria, including:

VIC, VHM, HPG, MCH, FPT, VPL, VNM, TCX, STB, MSN, VJC, SSI, SHB, VRE, GEE, SAB, VPX, EIB, POW, GEX, KBC, KDH, VCI, FRT, VND, DGC, PVS, DXG, HUT, and PDR.

Compared with the FTSE sample portfolio published in November 2025, several stocks show differences such as FPT, TCX, VPL, MCH, and GEE, mainly because FTSE constructed its sample portfolio based on data as of December 31, 2024, according to MBS.

What Investment Strategy Should Investors Follow?

Based on market outlook and strategic positioning in the current environment, the stock recommendations in SSI Research’s portfolio reflect a cautious approach while still offering meaningful upside potential.

Key investment theses for selected stocks include:

- MSN (Masan Group):

Formalization of Vietnam’s informal economy is creating growth opportunities for the WinMart retail chain, while tungsten prices remaining elevated support mining profitability.

Target price: VND 107,000/share

(Current price as of March 11: VND 73,000, upside 46.6%)

- CTG (VietinBank)

Stable profit growth is expected to improve the capital adequacy ratio (CAR) by roughly 40 basis points annually, supporting sustainable credit expansion.

2026 pre-tax profit is projected to reach VND 52.4 trillion (20.6% YoY), driven by stable net interest margins, controlled credit costs, and strong provision reversals.

Target price: VND 46,700/share

(Current price: VND 35,100, upside 33%)

- VCB (Vietcombank)

Profit growth could recover to 15.6% in 2026, compared with a low base of 4.5% in 2025.

The bank maintains one of the best asset quality profiles in the sector, with a non-performing loan ratio of 0.58% and the highest loan-loss coverage ratio in the system (259%).

Target price: VND 84,900/share

(Current price: VND 60,400, upside 39.7%)

- FPT

Earnings growth is expected to remain strong in 2026. A recovery in software and technology stocks could support FPT’s share price following the sharp correction in late February and early March.

Target price: VND 110,400/share

(Current price: VND 80,400, upside 37.6%)

- HPG (Hoa Phat Group)

Strong earnings growth in 2026 is expected to be driven by Dung Quat 2 expansion, anti-dumping measures, and a recovery in construction demand.

Target price: VND 35,000/share

(Current price: VND 27,400, upside 27.7%)

- MBB (MB Bank)

Sustained profit growth is supported by expanding market share and above-industry credit growth, along with strong contributions from non-interest income, including payments and Banking-as-a-Service (BaaS).

Target price: VND 33,200/share

(Current price: VND 26,800, upside 23.9%)

- PHR

Parent company profit before tax is expected to double, primarily due to land transfer income from Thaco, while maintaining a strong net cash position.

Target price: VND 74,000/share

(Current price: VND 60,300, upside 22.7%)

- VNM (Vinamilk)

Strong net cash position, stable dividends, and a solid fundamental base as the company enters a new growth cycle after a period of slower expansion.

Target price: VND 72,000/share

(Current price: VND 63,000, upside 14.3%)

Additionally, SSI Research’s March recommendation list includes strong performers such as CTG, SSI, VCB, HPG, and MSN, with projected 2026 earnings growth ranging from 19% to 63.4%.

Among them, MSN leads in projected profit growth and remains one of the companies expected to benefit most if Vietnam’s equity market is upgraded.

Author: LE MY - TRUONG DANG

RELATED TOPICS

RECOMMENDED TOPICS